2025-06-02

963 Views

7 minutes read

Share

When it comes to securing your family’s financial future, life insurance is often the first step. However, even in a market filled with options, many buyers remain confused between two popular plans: Unit Linked Insurance Plans (ULIPs) and Term Insurance Plans.

Both products serve very different purposes and suit different financial goals. While term insurance is ideal for financial protection in your absence, ULIPs combine life cover with investment opportunities. But how do you decide which is the better choice?

In this blog, we’ll help you understand the key differences between ULIP and term insurance plans, what each one offers, and how to pick the right option for your financial goals.

Key Takeaways

|

A ULIP or Unit Linked Insurance Plan is a mix of both investment and insurance. In ULIPs, one premium segment is paid towards the insurance and is known as a mortality charge. In contrast, the other segment is invested in various investment options like market reserves, securities, debts, values, or hybrids.

But ULIPs aren’t just about flexibility; they also offer dual benefits:

Let’s break these down:

Maturity Benefit: If you survive the policy term, you receive a maturity amount, which is the fund value on the policy’s end date. This is calculated as:

Fund Value = NAV (Net Asset Value) × Number of units you own

Once the maturity amount is paid out, the policy terminates.

Death Benefit: If the policyholder passes away during the policy term, the nominee receives a death benefit, which could be:

For Example, Kailash, 30, bought a ULIP in 2023 to save for his son’s higher education.

An OTP has been sent to your mobile number

Sorry! No records Found

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

Scenario 1: Kailash survives the policy term (25 years)

Additional units accrued: 1800

Total units = 232 + 1800 = 2032 units

NAV in 2047 = ₹700

Maturity Benefit = 2032 × ₹700 = ₹14,22,400

Policy ends after payout.

Scenario 2: Kailash passes away mid-term

Total units till date = 232 + 1000 = 1232 units

NAV at death = ₹700

Fund Value = 1232 × ₹700 = ₹8,62,400

Sum Assured = 10 × ₹1,20,000 = ₹12,00,000

Death Benefit = Higher of fund value or sum assured = ₹12,00,000 to the nominee (his wife)

This example highlights how a ULIP serves both as an investment tool and a financial safety net. It’s ideal for those with long-term goals like retirement planning, child education, or wealth creation, while ensuring life cover for your family.

ULIPs offer numerous features that make them the best. Listed below are some of them to explore:

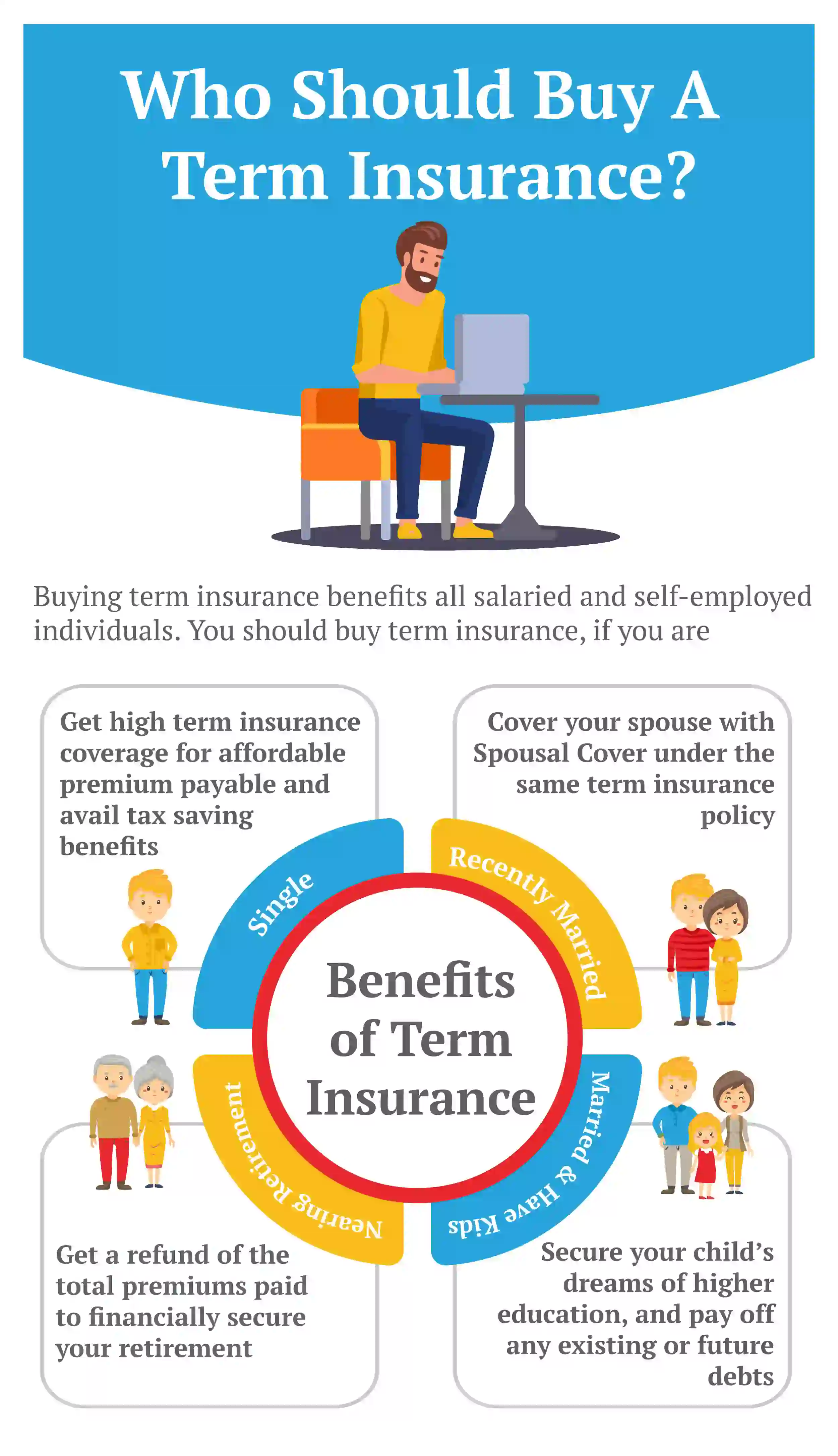

A term insurance plan is the purest form of life insurance policy that offers financial protection to your family in your absence. If the policyholder passes away when the term plan is in force, the death benefit is paid out to the beneficiaries. A term life insurance plan is affordable and has lower premiums as compared to other types of life insurance plans.

There are various types of term insurance plans, and you can choose one as per your financial goals and requirements.

Term insurance plans are straightforward, affordable, and focused solely on life cover without the complexities of investments. Here are some of its standout features:

Choosing between a ULIP and a term insurance plan requires understanding how each works and what they offer. Here's a quick breakdown of the key differences to help you make an informed decision:

| Features | Ulip | Term Insurance |

|---|---|---|

Purpose | Insurance + Investment | Pure life insurance |

Returns | Market-linked | No returns |

Premiums | Higher | Lower |

Risk Factor | Subject to market risk | No investment risk |

Maturity Benefit | Yes | No (Unless ROP opted) |

Tax Benefits | Section 80C and 10(10D) | Section 80C and 10(10D) |

Lock-in Period | 5 years | No lock-in |

Riders available | Limited | Extensive |

ULIPs are ideal for individuals who want to:

ULIPs encourage disciplined investing over the long term and are especially useful if you’re looking to grow your money while staying protected.

Term insurance is perfect for:

Young professionals with dependent family members

Individuals seeking high life cover at a low cost

Families where the loss of income could lead to financial hardship

People with limited budgets but high coverage needs

If your primary goal is to protect your family financially in case of your untimely demise, then term insurance is the most efficient and cost-effective tool.

Choosing between a ULIP and a term insurance plan depends on your financial objectives, risk profile, and long-term priorities.

Whether you choose a ULIP or a term insurance plan, selecting a reliable insurer is critical to your financial planning journey. Canara HSBC Life Insurance offers a range of innovative and customer-centric plans like the iSelect Smart360 Term Plan and various ULIPs that cater to diverse financial goals. With flexible features, transparency in charges, and trusted claim settlement, Canara HSBC ensures peace of mind for you and your loved ones.

Our commitment to financial protection and wealth creation makes us a trustworthy partner for both risk coverage and investment needs.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

Canara HSBC Life Insurance offers online ULIP plans that blend life insurance protection with investment growth, helping you build wealth while securing your family's future.

Canara HSBC Life Insurance offers online ULIP plans that blend life insurance protection with investment growth, helping you build wealth while securing your family's future.