Written by : Knowledge Centre Team

2021-11-03

1288 Views

11 minutes read

Share

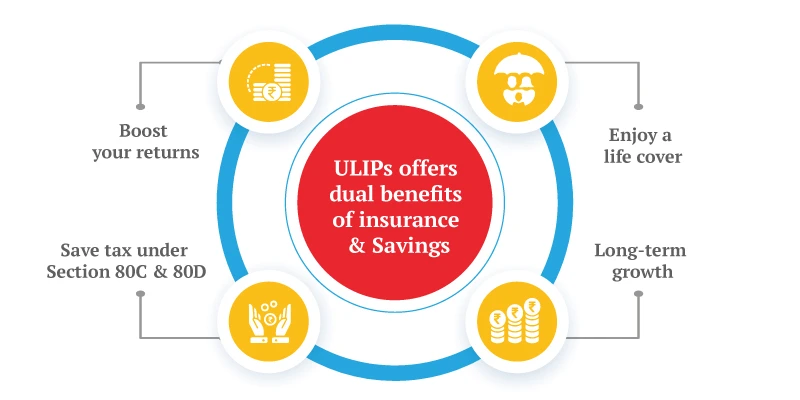

ULIP is a financial product that provides your life insurance cover and also acts as an investment. It combines the benefits of both insurance and investment in a single plan. Thus, this plan helps you to protect your family’s future and gives you a chance to build your wealth so you can achieve your goals. Buying the best ULIP online is one of the wisest financial decisions as it is completely hassle-free and convenient. Also, as ULIPs are known to offer the best of both the worlds - insurance and investment - you should always understand how it works so that you can gain benefits from it.

For ULIPs, as is the case with other life insurance plans, you have to pay a premium to get the policy. The premium depends on the amount of life coverage you want. The fixed premium you have to pay is used for providing life insurance as well as an investment instrument. Where the money will be invested is totally up to you. You can choose to invest either in debt or in equity or even both, known as hybrid investment.

As said above the premium you pay will offer you two benefits. It will invest your amount in funds to give you return while simultaneously making sure of the fact that policyholders family stays protected. This part is done by providing live coverage.

| FUNDS IN ULIP | SELECTED PREMIUM ALLOCATION RATIO | ALLOCATION OF RS 1 LAKH P.A. | ALLOCATION OF RS 20,000 P.M. |

|---|---|---|---|

| EQUITY AGGRESSIVE GROWTH FUND | 15% | 15,000 | 3,000 |

| EQUITY INDEX FUND | 15% | 15,000 | 3,000 |

| DEBT FUND GILT PLUS | 25% | 25,000 | 5,000 |

| DIVERSIFIED DEBT FUND | 20% | 20,000 | 4,000 |

| HYBRID FUND | 20% | 20,000 | 4,000 |

| LIQUID FUND | 5% | 5,000 | 1,000 |

| TOTAL | 100% | 1,00,000 | 20,000 |

Table 1: Premium Allocation to various funds in ULIPs

The premium which you pay is allocated to investment. As the policies name suggests, the amount you invest is broken down into specific ‘units’.

Learn how does risk involved on ULIP investment as equity shares.

Now, the whole fund is divided into these units. You will be allocated units from these funds in proportion to the amount actually invested by you. The units value will change with a change in its underlying assets.

| FUNDS IN ULIP | ONGOING NAV AT THE TIME OF UNIT ALLOCATION | UNIT ALLOCATION IN THE 1ST YEAR | ||

|---|---|---|---|---|

| for the Annual Investor | for the Monthly Investor | |||

| EQUITY GROWTH AGGRESSIVE FUND | 25.5 | 588.24 | 118 | |

| EQUITY INDEX FUND | 150.4 | 99.73 | 20 | |

| DEBT FUND GILT PLUS | 31.1 | 803.86 | 161 | |

| DIVERSIFIED DEBT FUND | 43.6 | 458.72 | 92 | |

| HYBRID FUND | 51.9 | 385.36 | 77 | |

| LIQUID FUND | 13.6 | 367.65 | 74 | |

| TOTAL | 2,703.55 | 540.71 | ||

Table 2: Unit allocation in the selected funds for the invested amount

If you wish to withdraw a part of your investment then the proportion of units will be sold for the payment of the withdrawal proceeds.

If due to unforeseen circumstances you die in the middle of the policy, then the death benefit will be provided to the nominee. The death benefit is higher than the guaranteed sum assured and 105% of the total premiums paid.

On the other hand, you do not die during the course of the policy, then you will be entitled to receive the total value of all the units invested by you in all the funds combined as a maturity benefit.

Every investment has associated expenses. The investment component of ULIP also has some charges associated with it as well. These costs are divided into several heads. The costs are deducted out of the invested premium or the fund value of the ULIP folio.

ULIPs charge the expenses under the following heads:

| Premium Allocation Charge |

|

| Policy Administration Charges |

|

| Fund Management Charges |

|

| Switching Costs |

|

| Discontinuation Charges |

|

| Mortality Charges |

|

Premium paid by you for ULIP is automatically utilized for all of these charges, and these remain somewhat the same for all the policies.

The investment component present in ULIP is what makes ULIP stand out from the other plans on offer. The existing traditional plans include the likes of Term Insurance, Endowment plan, Money-back plan and even whole life insurance. What these plans do is provide you with a hefty life cover as well as a guaranteed maturity benefit but they do not provide investment options.

Thus, ULIP provides you with ample flexibility. Policies like Canara HSBC Life Insurance P4G Plus also come with a safety switch option that allows you to switch between funds during the duration you pay your premium. The sum is invested in instruments whose returns are linked to the markets.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

Canara HSBC Life Insurance offers online ULIP plans that blend life insurance protection with investment growth, helping you build wealth while securing your family's future.