Written by : Knowledge Centre Team

2025-11-17

3880 Views

6 minutes read

Share

Akshay, 36 is an advertising professional who lives in Delhi with his wife and 4-year-old daughter. His wife is a homemaker and his daughter has only started school. The fast-paced world of advertising has made Akshay a safe and cautious investor.

While searching for a life cover, he wasn’t satisfied with the conditions of normal term life insurance. He wanted more value out of the money he was paying. Ultimately, he zeroed in on whole life insurance.

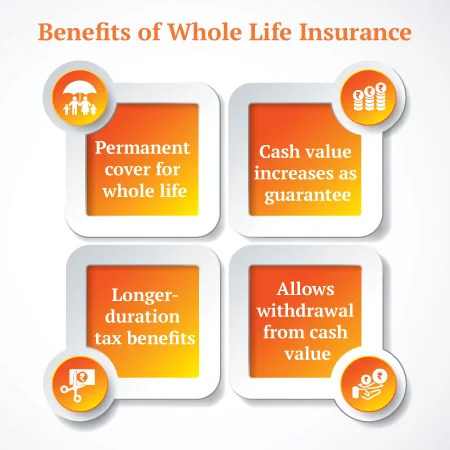

There were three compelling reasons Akshay based his choice:

If you are one of the late boomers; i.e. those who see financial success later in life, whole life insurance could be the best life insurance plan for you. Usually, when your success starts late in life, chances are your expenses, work-life and even liabilities will extend well beyond the official retirement age.

Therefore, it makes sense to extend your life insurance too accordingly. But, extending life cover beyond 60 certainly doesn’t come cheap. Thus, it will be better to look for additional benefits, such as maturity benefit or estate.

While plans with a maturity value will cost a lot, whole life term plans are a better choice for multiple reasons:

With any other investment plan which has a maturity value, you will either compromise on the life cover or premiums. Whereas, the whole life term plan offers the best combination of both.

Whether you are starting late or for any other reason want the life cover to continue after your retirement, whole life insurance offers a better solution. Whole life insurance from Canara HSBC Life, iSelect Smart360 Term Plan, offers features which will be quite handy for you.

For example, the plan necessarily offers premium payment term only till retirement. So that your entire premium is invested while you are employed. At the same time, the plan offers adequate life cover for the family being a term insurance plan.

Additionally, you can choose to get all the premiums you paid for the cover back at retirement. However, your life cover will continue until the age of 99. Although the plan does not have any maturity value, long tenure ensures that your family gets the funds even after natural death.

According to guidelines issued by the IRDAI (Insurance Regulatory and Development Authority of India), all the claims related to Covid-19 treatment (including quarantine period) will be eligible to gain coverage under a standard health plan. It will be there to help the insured with the normal cover on hospitalization for all viral infections, including Corona. All the features you enjoy under your chosen health insurance plan will also apply to Covid-19 treatment. But to avail treatment through your medical insurance, you must be hospitalized at least for 24 hours. In the event of hospitalization, all your expenses will be covered for treatment of disease, including pre and post hospitalization expenses.

If you want to leave a legacy for your grandchildren, you should invest in whole life insurance. It is a plan that will provide your grandkids with the sum assured amount after your death.

Gone are the days when parents built houses and real estate for the next generation. As the future increasingly becomes unpredictable fixed assets are more of a liability than assets. However, as unpredictable the future could be, cash is one thing which will always open more possibilities.

Thus, the whole life plan lets you pass on a lucrative and useful estate to your children or grandchildren. Also, since it will be coming as a life insurance payout, it will be tax-exempt in their hands. It will be a beautiful memory and gift that your grandkids will cherish for life.

Canara HSBC Life’s online iSelect Smart360 Term Plan has the option to work as a whole life plan. In fact, if you start investing early enough, you can have better value for your money.

Premium payment term is that time within which you need to pay all premiums of the policy. For example, if you choose a premium payment term for your life insurance plan as 10 years your total premium will be distributed equally between 10 years. Premium payment term is always less than or equal to the policy term.

A life insurance contract is a long-term commitment, and that is why limited premium payment is so useful. You can limit your liability of premium payment and still enjoy full benefits and cover.

Considered as one of the best life insurance plans, whole life plan has multiple premium payment options. It also offers the option of return of premium benefit where the premium will be returned once you outlive the policy tenure. You can easily align the plan as per your needs. The plan also has an option to cover for a limited tenure or an entire lifetime.

For high sum assured and for females, there is a special discount on the premium. You can also get an enhanced cover by adding riders like accidental death benefits or permanent disability benefits. Choose from the multiple premium payment options including a single payment for the term or payment only during working years.

Whole life insurance is an ideal investment for those who want financial security during retirement and want to leave a legacy for their children. It is a simple and affordable plan that will provide a cover for you as long as you live.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.