Written by : Knowledge Centre Team

2025-07-02

881 Views

8 minutes read

Share

Fathers do a lot more for their children than they are acknowledged for, both financially and emotionally. Your father earns and saves to cater to your education and other needs that you usually demand. Thus, he has been the primary reason for your financial security today. There can be no better time than Father's Day to bring a smile to his face. While most of us choose to give materialistic things on such special occasions, providing him financial independence during the post-retirement years to come.

Saving and smartly investing the money might be the best life lesson your father has given you. It's your responsibility to do your part and give him the best gift for Father's Day in form of a life insurance plan.

Medical illness takes away a huge chunk of your savings. It is quite possible or even obvious that the older your father grows; he's more prone to get health issues.

So, it is wise to invest your money in advance to deal with any unforeseen event without worrying about the costs. Medical insurance will be a great gift. Medical insurance policies are two-way policies that help in appropriate money investment and use the same money to pay your medical bills.

A term insurance plan provides cover for any risk of the early death of the policyholder. In addition, it provides financial support to the family after the insured person's demise. But buying term insurance will even offer security to your father after he retires.

You can either buy the policy under your name and make your father the nominee. Then, under unfortunate circumstances, your father will receive the plan's additional benefits.

In addition, the insurance company will pay the assured amount in case of death or any terminal illness. Do check the iSelect Smart360 Term Plan that covers all these benefits along with an option to add a spouse.

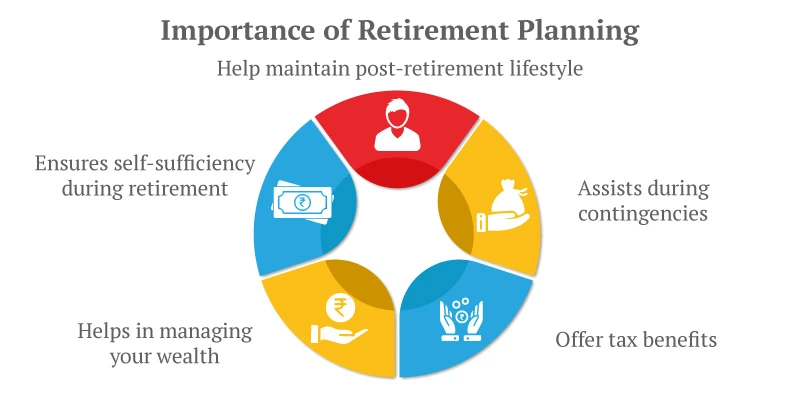

Opting for retirement plans as a Father's Day present is something permanent and valuable. Most retirement plans come with long-term investments and savings (ULIPs). It means that if you start investing in the scheme at the age of 25, you can accumulate a large corpus during your working days.

The earlier, the better. Like the term insurance plans, at the time of the policyholder's death, the entire sum is transferred to the nominee. Some ULIPs also offer partial withdrawal. So, you can surely ensure your father's financial freedom after he retires by investing in such a plan.

Know these 5 Tips to plan for retirement.

These plans are very similar to the retirement plans and have a long-term annuity contract to generate income once someone retires. Such a plan might be the perfect Father's Day insurance plan to go for. You can directly collect and save annuity for your father's retirement years. There are several annuity options in such a plan, like a deferred annuity, immediate annuity, and annuity with or without life cover.

The Pension4Life plan is a suitable option as it provides guaranteed lifetime income to cater to your father's future needs as long as he and your mother are alive.

Add this to your Father's Day insurance schemes gift list and purchase among the wide variety of annuities offered under the plan. Gifting life insurance on Father's Day is a unique and sensible decision keeping your father's age in mind. His future financial security is vital as the non-working years might drain his economic and physical strength to gather resources and work again.

Everyone wants a relaxed post-retirement life, so consider life insurance plans offered by Canara HSBC Life Insurance. Make an informed decision and select the best plan to help your father enjoy his financial freedom.

An OTP has been sent to your mobile number

Sorry ! No records Found

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.