2025-08-10

892 Views

8 minutes read

Share

A child’s aspiration keeps evolving throughout their childhood and is shaped by their experiences, learnings, and the environment that they are brought up in. At the age of five, your child may think of becoming a pilot that may subsequently change to becoming a scientist when they turn ten. By the age of fifteen, the animation may sound exciting to this teenager.

Whatever be the aspirations and however fickle they may sound, you will still want to plan well ahead of time. Some may want to buy the best child plan, while some may want to open an FD for their child. In the last two decades, several private universities have also come up across India and offer quality infrastructure, academic delivery, and a good learning experience. But these coveted degrees come at a cost. Even government-backed institutions are no longer as affordable as they were in the last century. If your eyes are set west, the costs would swell into crores.

In another unfortunate scenario, if you are not even around in the future to support your child’s career, who will help them realize those dreams that were nurtured all these years. In a hypercompetitive world where there is fierce competition for opportunities, a lack of quality education would be a major and permanent setback.

The best way forward would be to start investing early and do it systematically over the planned period. Investing in the right instruments that give you the required amount, at the right time along with the peace of mind is quintessential. The 5 steps listed below can help you navigate this path with ease.

By trying different ideas, their margin of error, in decision making while pursuing a career, would considerably taper down. Closely observing their inclination, passion and aptitude will give you a direction to work on a specific financial goal. For example, if they are an aspiring filmmaker you may evaluate options of admission to Vancouver.

Should you depend on education loan to fund your child’s dreams?

For example, on an education loan of Rs. 30 lakhs, repayable at a 10% interest rate over 10 years, you will have to pay Rs. 18 lakhs as interest. If you avail of an interest-free loan scholarship of Rs. 30 Lakhs, you save a neat Rs. 18 Lakhs

| Education Loan | |

| Amount Spent on Education | Rs. 30 Lakhs |

| Amount Spent on Interest | Rs. 18 Lakhs |

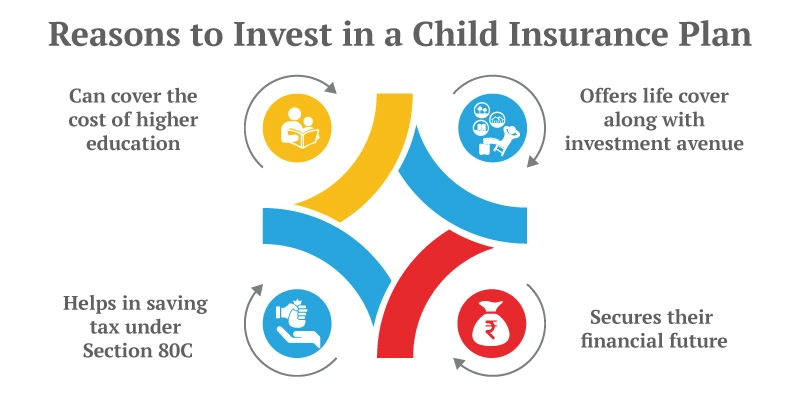

Investing about Rs. 1 lakh each year for 15 years can fetch you a cumulative return of approximately Rs. 25 lakhs. The 1 lakh that you invest each year is deductible from your taxable income, under section 80C of the Indian Income Tax Act.

The maturity value received from the child plans is also exempt from tax. Canara HSBC Life Insurance provides the following child education plans you can meet your child’s goals with:

Periodic rotation helps you take advantage of market movements and keep your portfolio working in all conditions. In case you are looking for guaranteed maturity value, Guaranteed Savings Plan is a perfect choice.

The key, however, would be to continue increasing your investment as your income grows to maintain the ratio of income to savings. This will help you not only build a better corpus but also meet any unexpected demands in the future. The 5 steps mentioned above will enable a clear thought process and let your money grow while you focus on the apple of your eye!

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.