Written by : Knowledge Centre Team

2025-10-16

892 Views

8 minutes read

Share

Becoming a parent gives you overwhelming happiness. Along with it, it also brings in huge responsibility. You dream of a beautiful future for your child, and to fulfil them, you need money. To get the money, you need financial planning. As a parent, you must know how much to invest for your child's future and where. One such option you can explore is child plans.

Child plans are of various types and help you to create a corpus for your child's future. They ensure the increasing cost of education does not hamper their dreams. These are long-term saving plans, and most of them come with a mix of investment and insurance options.

Most people have a completely different understanding of the child plan. Below are the five popular myths about child plans and the reality corresponding to them:

Most parents think child plans are life cover for a child and consider it inauspicious to buy an insurance plan for a child. Child insurance plans do not provide cover for your child.

When you buy a child plan, your life is covered and not your child's. Life cover ensures, if you die, the benefits associated can take care of a child's dream. P4G comes with a life cover that is paid to your nominee in case of your death. The sum assured will depend on your annual premium and the plan option you choose. As per your need, you can decide the plan and premium you want to pay.

When we talk of the child plan, you may think it is only for education and may only be available when your child turns 18. Most child plans give you the flexibility to choose your policy tenure. Since child plans are not just about educational goals, you have an option to withdraw funds earlier also depending on the goals you have created for them.

For example, P4G plans give your Systematic Withdraw Option. Under this option, you can withdraw a pre-decided percentage of the fund at a chosen frequency. Depending on your child's current age, you can decide when you would need the funds for her life goals.

Many people think if a parent dies, the child plan expires, and no one receives any benefit. Contrary to popular belief, child plans are the opposite. The purpose of a child plan is to ensure the dreams you have seen for your child get fulfilled under all circumstances. Hence, a child plan comes with death benefits - the benefits remain even after your death.

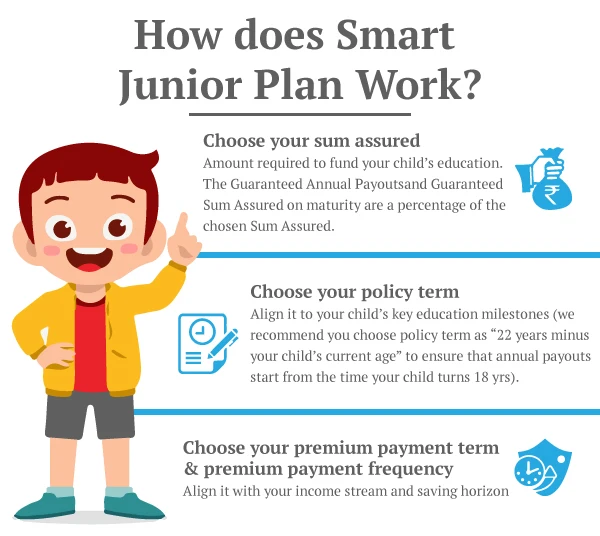

For example, in the Canara HSBC Life Insurance Smart Junior child plan, the family receives a sum assured as a death benefit if the insured dies during the policy tenure. Also, all the future premiums (if any) need not be paid by the family members.

The Smart Junior child plan provides you with guaranteed annual payouts in the last four years of your policy tenure. Even if you die, the beneficiary will receive the guaranteed annual payouts as per the policy.

The general belief is that child plans are expensive. They come with a high investment amount and a number of hidden charges. When you invest for a child's future, in most cases, you have time to grow capital. So even if you invest a small amount, you can create a corpus for your child's future. Keeping this in mind, most child plans let you invest a small amount as well.

For example, in Promise4Growth Plus Life Option, the minimum amount to buy the plan is Rs 2000 per month, or you can pay Rs 24,000 yearly. Even the other charges are minimal. The maximum fund management charge (FMC) for ULIP plans is 1.35%, much lower than other financial instruments. With all the features and options Invest4G provides you, the charges are very minimal.

People want to stay away from child plans because they think the child plans invest in equity funds and equity investment is risky. First, the equity investment is not risky if you invest for the long term and the fund is managed by professionals. Second, depending on your needs (time horizon and risk appetite), you can choose the financial instrument you want to invest in under child plans.

For example, with the Promise4Growth Plus plan, you have the option to invest in equity funds (multiple equity options), debt funds, liquid funds, or a combination of all. If you are not sure which investment option is best suited for you, the plan offers you Auto Portfolio Management.

Below are some reasons why you should save for a child's future goals:

Thus, investing in your child’s future goals is an important decision and requires you to select your investment options carefully.

When you buy a child plan, you should not go by hearsay. You must make an informed decision. Child plans are very crucial, and you should study them carefully before buying a plan. A good investment decision today can help your child in a number of ways in the future.

An OTP has been sent to your mobile number

Sorry! No records Found

Thank You for submitting the response, will get back with you.

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.