Written by : Knowledge Center Team

2025-11-12

1092 Views

7 minutes read

Share

The underlying principle of any life insurance policy has traditionally been risk mitigation against loss of life. However, with evolving economic, cultural, and sociological fabrics, the type and magnitude of risks have also changed with time. We are now in a world marred with Volatility, Uncertainty, Complexity, and Ambiguity (VUCA) which makes people’s lives and lifestyles more vulnerable than ever.

Nuclear families, increasing middle-class aspirations, the rising cost of education, lifestyle ailments, and the risk of emerging diseases make insurance a multi-faceted financial cushion. A life insurance policy can be a solid source of corpus for old age, financial support for a child’s education, or even a substitute for income. In all setbacks in life, the child is often the most affected family member as his/her education takes a hit when the family goes through a crisis. Unfortunately, the lost time can never be made up.

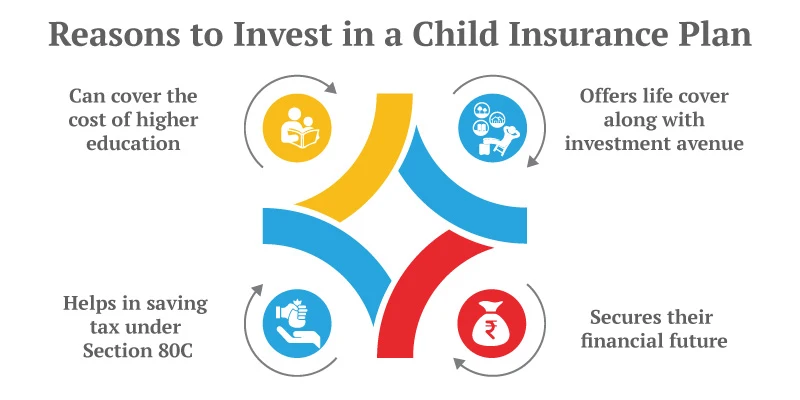

A child education insurance can help mitigate risks so that education can continue without interruptions. Child insurance plans can help you ensure this continuity. This life insurance policy for a child has a single purpose, to help your child achieve the goal even if you cannot be there to ensure the same.

However, that’s not the only reason you should consider investing in a child plan. Here are six more compelling reasons to do so:

You have the option of investing in two types of child insurance plans:

ULIP plans give you the option of systematically investing in an equity fund. Thus, benefit from the market performance. At the same time, it also allows you to invest in debt funds. So, you can not only manage your investment risk from equity funds but also keep the corpus you build safely in the final few years of your investment.

Although you can invest in debt funds in the ULIP plan if you want to stay away from the stock market, you can also invest in endowment plans. These plans offer guaranteed maturity value so that you can be sure about the amount you will receive at the end of the term.

Both policies offer limited premium payment term. So, you don’t have to keep investing throughout the policy tenure. For example, if your child is 5 years old and you buy a child plan for 15 years, you can opt to pay premiums for, say, 10 policy years, i.e., until your child attains 15 years of age.

Understand if limited pay plans are a good idea?

From the age of 18 years, s/he can receive annual pay-outs that can help finance undergraduate education. Moreover, on maturity, you will receive the guaranteed sum assured along with accrued bonuses, if any. This can be utilized for post-graduate studies or marriage.

One of the biggest roadblocks for you as a parent is the uncertainty of life. In case of serious disability, your capacity to earn the same amount of money could be affected. The best child insurance plans in India mitigate this risk and pay all future premiums so that the child’s education is unaffected.

For instance, the policy can continue towards the intended maturity value.

Several child insurance policies have dynamic and balanced equity-debt allocations. Experienced fund managers ensure that your investments fetch the best possible returns on your money. In some plans, there are auto funds rebalancing options that maintain an allocation in a specific proportion irrespective of market movements.

Here are 4 benefits of getting life insurance coverage for your child.

The returns in most child plans are very high due to sizeable investment in equities and almost always beats inflation in the medium and long term. This not just protects the money from getting eroded but also grows it considerably. Of course, policies with traditional endowment plans are also available. The returns may not be as high as in equity-linked policies, but the growth is generally stable and predictable. In endowment plans, your money is invested in bonds and Government Securities.

Emergency and unforeseen expenses can crop up anytime. A flexible policy that allows you to make partial withdrawals for contingencies can help overcome temporary setbacks without compromising on long-term financial goals.

Higher education is costly and more so if your child aspires to study in western Universities. Despite generous scholarships offered to meritorious students, there is bound to be a shortfall in funds that have to be self-financed. Banks and Non-Banking Financial Companies (NBFCs) offer education loans only if there is strong collateral along with a co-signor. Insurance policies are the best form of investments that not only give milestone-based pay-outs but also stand as credible collateral to avail loans.

With a child insurance plan, you can avail of a loan on the policy from the insurer itself. After the lock-in period, the policy starts to acquire a cash value (surrender value). This surrender value keeps rising as you keep on investing in the policy. So, just in case you need money for the child’s education before the policy matures, you can avail of a loan on the policy.

Premiums you pay into the child insurance plans, up to Rs. 1.5 lakhs are eligible for deduction under section 80C of the Indian Income Tax Act. Also, the maturity value and any partial withdrawals you make after the lock-in period is tax-free.

The Lock-in period for ULIP plans is 5 years while for endowment plans it can be two years.

An OTP has been sent to your mobile number

Sorry! No records Found

Thank You for submitting the response, will get back with you.

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.