Written by : Knowledge Centre Team

2026-07-30

906 Views

6 minutes read

Share

For decades, people had limited options when it came to insurance plans. But with the growth of the insurance market and the diversification of the target demographic, the need arose for new kinds of insurance plans with all sorts of new features that customers can pick and choose from. The limited pay term plan is one such plan.

There are several disadvantages to a regular term insurance plan. For starters, there is a chance that the premiums may extend beyond your retirement. If you are no longer earning the same amount of income you used to when you signed up for regular premium plans, you may not be able to pay off the premium dues. Instead of helping your family in the long run, you may drive yourselves into more debt and financial hardship. Regular plans aren't, therefore, useful for people nearing retirement.

In such a situation where you are in a financial crisis, there is also a higher chance that you may miss one or two payments. Once laps occur and there is an unpaid premium, the policy will lapse, after which the bank and its plan will pay you no benefits. You will lose coverage.

A limited-term insurance plan allows the user to customize the number of years to finish paying their premiums. This autonomy allows for great flexibility and planning for the user. Once they finish paying their dues within the promised time limit, they need not pay any more money to the insurance company and can enjoy the plan's benefits for the rest of the policy duration.

People who have an unsteady or flexible income or people who work in unpredictable fields should go for a limited pay plan. Once you are confident that the next few years are at your productive peak, you can retire with a full insurance period and peace of mind. If you are close to your retirement and have the highest income for someone your age in your field, limited-term insurance is for you.

For instance, if you buy a term cover for thirty years and are comfortable paying all the insurance money within the next ten years, perhaps because your family is at its peak levels of income, you can go for limited-term insurance. By the time you retire, you will have twenty insured years left, during which you will not have to pay a single penny.

Limited-term insurance plans are popular mainly because of their flexibility and customizability in terms of time duration and the monthly payable amount (individual banks). Here are some additional benefits:

Depending on the scenario of your untimely death, banks will provide you with a certain assured amount. If you die a natural death during the policy plan period, the person you nominate will be provided with more than 100% of the sum, along with a bonus. The same goes for a case of accidental death during the policy. This is a great advantage that can secure the life of your family.

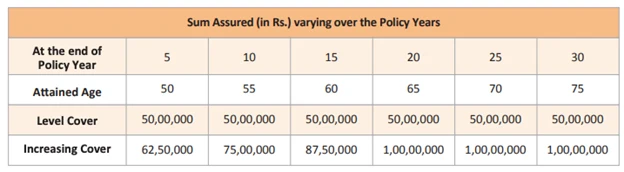

Additionally, most banks offer a final additional bonus if you outlive the plan and live to see it mature. This sum will be equal to the assured sum promised in the beginning, in which case you will be able to enjoy your savings with your family. For instance, take a look at the beneficial sum assured scale offered by Canara HSBC life Insurance limited pay plan called iSelect Smart360 Term Plan.

Some banks also provide the option to take loans to pay the premium, provided that you have been regular with the payments for two or more years. This is great if you face a tough month, but it is not advised to rely on loans to pay off premium dues for apparent reasons of counterproductivity.

While this sounds like an excellent option, it does have its disadvantages. For starters, To make sure that limited pay insurance plans are the best idea for you, you should evaluate your situation and pick the right one.

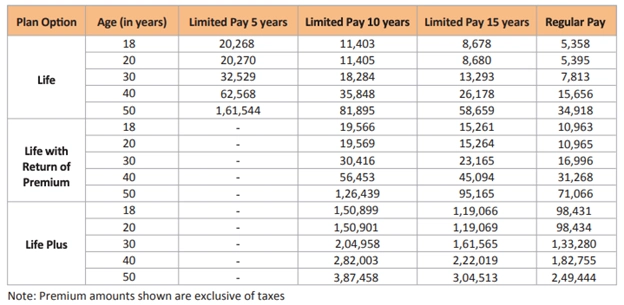

While it may seem like the limited payment plan is better in terms of savings, it is in no way cheaper than a regular payment plan. Understandably, the premium amount you pay will be higher, since you have to cover more amounts of money in half the time you will use for a regular plan. Suppose, by any chance you lose your job or end up physically unable to work. In that case, you will not only miss out on payment and lose coverage but lose more money in one go than you would in the case of a Regular Payment plan – you would have already paid more at that point if you are a limited premium plan holder. The iSelect Smart360 Term PlanTerm Plan has the following premium payment scales:

What attracts customers is the overall reduction of the premium to be paid, but the buyer may be paying a higher amount. The internal rate of return would be the same regardless of whichever policy you choose, so keep that in mind while you pick out a plan.

All of these disadvantages may lead you to conclude that you may benefit from a regular payment plan.

A regular payment plan would benefit someone who is very regular and planned with their finances. Disciplined policyholders who have saved over the years will stand to gain from a regular payment plan.

If you are young and have plenty of time before you reach the age of retirement, you may want to settle for a regular payment plan. If you just started working, you are in a position where you can afford to pay regularly and for a more extended period. The standard plans can also prove more affordable since it is spread over a longer-term with smaller premiums to be paid periodically.

Work in a sector where you have assured an individual income regularly or work in a very stable field where there is no risk of unemployment, demotion, or loss of pay. The regular pay plans may benefit you more than the limited pay plans.

In the case of a limited pay plan, the maximum age of eligibility may also be higher. For instance, nine-year premium payment plan requires you to be at least sixty-two years old.

In conclusion, while Limited Pay Plans have their advantages, you should ideally contextualize your choice based on your current situation and your predictions for the future. Limited pay plans are a great idea for a few and can be disastrous for others, so choose wisely.

An OTP has been sent to your mobile number

Sorry ! No records Found

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

Canara HSBC Life Insurance offers online term insurance plans to secure your family financially in your absence.