Written by : Knowledge Centre Team

2026-02-28

939 Views

10 minutes read

Share

Term insurance is a life insurance product whose purpose is to provide life coverage to you for a specific period of time or ‘term’. If you have bought a term plan and you die within the term of the policy, then the sum assured is provided to your family. This helps in maintaining the financial security of your family even if you are not there.

Now we know how the term life insurance plan takes care of your family in case of your death. But death is not the only thing that you would fear. There are other risks as well. Your earnings can stop even if you have not died. How? Suppose you suffered a massive accident. Though you managed to survive, now you have a permanent disability.

What if you are earning well and are financially secure, but suddenly you are diagnosed with cancer? All your savings will go towards the expensive medical care you have to undergo. This will shatter all your plans in a matter of seconds.

Key Takeaways

|

Both the above examples highlight to you the risks of critical illnesses and disability. Before going further, let’s take a look at what will constitute a disability.

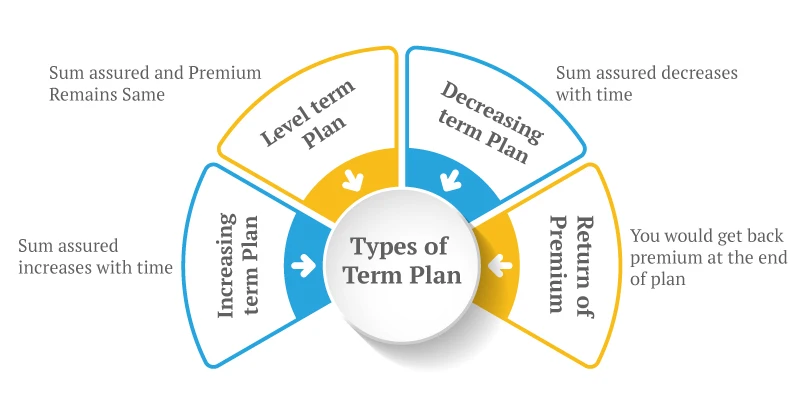

Also Read: Various Types of Term Insurance

An OTP has been sent to your mobile number

Sorry ! No records Found

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

A disability happens when the worker is unable to perform their job due to some limit of the functioning of a body part. The parameter of what can be called a disability varies with different insurance providers. But more or less, the following things are counted as a disability:

Also Read - Short term vs Long term Disability Insurance

What these disabilities do is they can limit you from doing your job and earning a living. This is a bigger concern when you are the only breadwinner for your family. This sudden loss of your income can hinder the financial stability of your family.

“Loss of income + Additional cost of living”

Not only can a disability cause a loss of income, but it also increases expenses. To take care of disability, many modifications in your home need to be done, and many medical treatments are also needed. These costs were huge. So, disability hits you as a ‘double whammy.

Also Read - How to Choose the Right Disability Insurance?

Keeping in mind the seriousness of disabilities and how it affect you and your family, term life insurance policies provide you with the option to cover disabilities.

Term plans have a feature that involves adding riders to your basic cover. There is a rider that covers you for disabilities. This is known as the Accidental Death and permanent disability rider. These riders are available with:

While buying your term plan, make sure to check the rider options and understand the terms before adding it to your policy.

Riders are add-on covers that can be added to your existing cover. They enhance the scope of your life or health insurance plan. You may avail the following types of riders with your life and health insurance plans:

By selecting the Accidental Total and Permanent Disability rider at the time of purchasing your term plan, you can get disability cover.

Term insurance cover is a pure protection plan. Thus, this is one plan which offers adequate financial protection at a pocket-friendly cost. Adding disability cover to a term insurance plan means you can add a large enough benefit amount without affecting the premium too much.

For example, you can add up to ₹25 lakhs in disability benefits to your ₹1 crore term insurance plan. However, this benefit cannot exceed the base life or health cover of the primary policy.

Thus, adding more than ₹10 lakh cover to a ₹10 lakh ULIP would not only be impossible, but you may have to opt for an even lower amount.

So, add disability cover to your term plan so that you get:

Choosing this rider entitles you to get an additional sum in case you suffer from a permanent disability due to an accident. The sum is separate from the life cover; it acts as an add-on to your existing sum assured.

The amount can be used to meet the expenses associated with your disability. This will reduce the burden on your family members. This will ensure that you do not become a liability and can take care of the sum you received.

To avail of this rider, you need to pay an amount that is over and above the extra premium. This varies from policy to policy.

Note that you will receive the sum assured in the case of ATPD only when your disability is included in the insurance provider’s policy. Also, the insurance rider has some criteria involved. If your disability falls outside of the following criteria, then you will not be entitled to receive the sum assured.

Criteria:

ATPD has some exclusions; if your disability arises out of these exclusions, no benefit will be payable. These are as follows

Now that we know what exactly a disability cover is and how it can help you, let us take a look at the features of a disability cover.

iSelect Smart360 Term Plan by Canara HSBC Life Insurance offers premium protection plus variant, which will not only provide you with the ATPD sum assured, but also make sure that the policy continues and the death benefit is also intact.

This reduces the financial stress that you or your family members can go through while paying premiums despite no income.

Click to use: Term Insurance Calculator

A term insurance calculator is a useful online tool that helps you determine how much coverage you need based on your income, lifestyle, and family’s needs.

The above calculation and illustration of figures are indicative only and not on actual basis.

While term life insurance is essential for protecting your family in the event of your demise, don’t overlook the financial risks that come with surviving a severe accident or illness. A permanent disability can stop your income and increase expenses, creating a double financial burden.

By adding a disability rider to your term insurance plan, you ensure that you and your family have a cushion to fall back on, no matter what life throws your way. Opt for comprehensive plans like the iSelect Smart360 Term Plan by Canara HSBC Life Insurance to enjoy the benefits of premium waivers and dedicated disability protection, all in one smart plan.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

Canara HSBC Life Insurance offers online term insurance plans to secure your family financially in your absence.