Written by : Knowledge Centre Team

2026-02-11

1165 Views

10 minutes read

Share

When you plan for your future, one thing that does not come top-of-mind is the possibility of untimely death. What will happen to your family and loved ones if you die? It can be uncomfortable to plan for it in advance, but if you do so, you will do a lot of good to your family. To protect your family from every kind of situation, you need to take a Permanent Life Insurance Policy.

A permanent life insurance policy is a popular name given to whole life insurance plans in the USA. A whole life insurance plan is a type of insurance plan that provides you with death benefits as well as survival benefits. When you opt for a whole life insurance plan like iSelect Smart360 Term Plan, the policy gives you cover for as long as you live.

You pay the premium for 10 or 15 years, depending on the option you chose. You get insurance cover for your entire life. For example, you are 25 years of age, and you buy a whole life insurance plan for 15 years and a sum assured of Rs 50 lakh. You will stop paying the premium when reaching 40 years of age. The death benefit will last for life.

An OTP has been sent to your mobile number

Sorry ! No records Found

Thank You for submitting the response, will get back with you.

When you decide to go for a whole life term plan like iSelect Smart360 Term Plan from Canara HSBC Life Insurance, below are the steps you follow:

For example, you buy a term plan in your 20s with a sum assured of Rs 1 crore. You get married at the age of 30, within one year of your marriage, you have an option to increase your Sum Assured by 50 per cent. So after your request is processed, you will have a Sum Assured of Rs !.5 crores, under the same policy.

At the time of birth of a child or, purchase of a house, you have an option to increase Sum Assured by an additional 25 per cent, i.e. new sum assured will be Rs. 1.75 crores.

The premium, of course, will also increase as per the new sum assured. However, the increase will be nominal compared to buying a new life insurance plan.

Increasing In this option, the sum assured will increase by 5 per cent (of the initial sum assured) every year. The maximum increase in the sum assured will be 100 per cent of the original Sum Assured.

Learn how an increasing sum assured in a term plan?.

For example, you buy a Whole Life Term Plan with a Sum Assured of Rs 50 lakh. The Sum assured will be Rs 62,50,000 at the end of 5 years, Rs 87,50,000 after 15 years, and Rs 1 crore after 20 years. Post this, it will continue to remain the same.

The plan will expire under the following circumstances:

This term plan has a very high chance of paying the benefit amount to your nominees. Since you can change the nomination anytime during the policy term, the policy works both as a protection plan and a legacy plan for you.

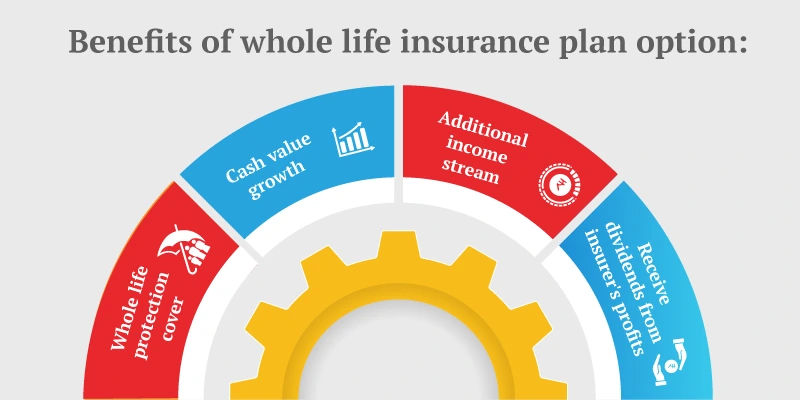

If you choose the Life Plus option under the iSelect Smart360 Term Plan, you get the features offered by a whole life insurance plan. Under this iSelect Star’s whole life cover you get the following benefits:

Now that you know the types of permanent life insurance and how they work, you can easily pick the right plan without any confusion. Buying a permanent insurance plan helps you not only protect your family while you are building their future but also leave a legacy when you are done.

Additionally, you may choose a limited premium payment term for your policy. Ideally, you should be able to pay off all the premiums for the entire policy tenure within your employment period. That way you will not have to worry about premiums during retired life, and the policy can work as a legacy plan after you.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.