Written by : Knowledge Centre Team

2026-03-10

1198 Views

10 minutes read

Share

To build a beautiful home, couples come together with shared dreams, love, and responsibilities. However the life is unpredictable, and the sudden loss of a partner can create emotional distress and financial uncertainty. A joint life insurance policy offers protection for both partners, ensuring that the family’s future remains secure. It provides financial support to the surviving partner and helps protect long-term goals like children’s education or daily living needs. In this blog, we dive deep into joint life policy in detail.

Key Takeaways

|

A joint life Insurance policy treats both partners as policyholders and provides financial security to both of them. Life is uncertain, so keeping your partner’s financial life secure is the key requirement.

It is a single plan that covers both the wife and the husband, whether both of them are earning or only one. This way, even the homemaker’s human life value is covered by the family.

For example, if a couple have a joint life insurance and the husband is the first one to die, the homemaker wife will receive a support amount from the joint life policy.

While a single life policy would have expired on the death of the policyholder, the joint life insurance will continue to cover the other spouse until the expiry of the policy. This policy provides financial support to the remaining partner regardless of their working status.

Thus, if the surviving partner also suffers an untimely mishap, the children will still have adequate financial support. They can continue their lives and meet their future goals with the same financial support as they would have with both parents in their lives.

An OTP has been sent to your mobile number

Sorry ! No records Found

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

Once a couple buy a joint life cover policy, the other partner is covered under the same plan. Single-life policies will cover only one person, but joint life insurance is a great way to look out for your partner after your demise.

A joint life cover plan works on a first-death basis. If a partner dies an untimely death, the life cover for the other person continues after the payment of the death benefit of the deceased spouse. This is regardless of the working or non-working status of the surviving spouse.

In a very unfortunate case, where both partners are unable to survive the unfortunate situation, the insurance amount is credited to the policy’s beneficiaries or the listed legal heir.

Only the insured amount is paid to the living partner, and no additional benefits can be claimed by the other partner.

Joint life insurance helps the homemaker spouse with a life cover. The homemaker spouse is eligible for a life cover equal to 50% of the sum assured for the breadwinner spouse.

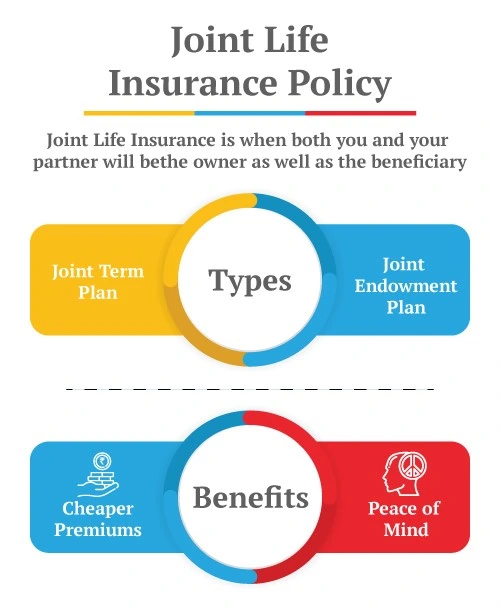

There are two options in the joint life policy. An individual can choose as per their preference.

It also works as an asset during the retirement period, as it acquires a cash value

Joint life policies offer unique benefits to policyholders and their families. Some of the most important reasons to buy joint life insurance are listed below:

A married couple can buy a joint life cover. These policies waive off further premiums if one of the policyholders dies an untimely death. The other is entitled to complete the policy term with their share of the life cover.

However, this insurance policy is also very suitable for business partners. They can buy the joint life cover with another business partner to protect the company’s interests. In case of the untimely demise of either of the business partners, the other will receive a fund which can be useful to settle the succession of the deceased partner.

If couples are worried about the financial security of their child after their demise, they can buy joint whole-life insurance to make sure their child remains financially protected. This money will surely help the child’s future expenses like educational fees, house maintenance, healthcare, and so much more.

iSelect Smart360 Term Plan by Canara HSBC Life Insurance can be easily purchased online, and it offers the following features for joint holders:

Cover for the homemaker spouse.

Critical illness and accidental disability benefit riders for the primary holder/working spouse.

Option to increase the cover for the primary holder/working spouse in the policy after purchase.

Death benefit payment as a regular income option.

Joint life insurance is a practical and thoughtful way to secure your family’s financial well-being. It protects both partners under one plan and ensures continuity of financial support in uncertain times. Couples and business partners alike can benefit from this shared protection. With plans like iSelect Smart360 Term Plan by Canara HSBC Life Insurance, they can enjoy low premiums, flexible benefits, and lasting peace of mind for their loved ones.

If your primary goal in buying the policy is to offer adequate financial protection to your family joint-term life insurance is a better option. However, if you plan to fulfil a future goal joint life endowment plan is a better choice as it has a maturity value.

Yes, joint life insurance policies can offer similar benefits to both spouses if both are employed while reducing the paperwork and premium cost. In the case of the demise of one partner, the life cover will continue to cover the surviving spouse. You can select the premium waiver option to ensure continued coverage without premium payments.

Premium paid up to Rs 1.5 lakhs for joint life insurance provides tax benefits under section 80C of the Income Tax Act. Also, if you receive the insurance amount after the death of your partner, this amount will be tax-free under section 10 (10D).

The policy continues if you don’t take any action. In case of your death, your ex-spouse will claim the insurance amount and benefits. You can also surrender the joint life policy or ask the insurer to divide the policy into two individual policies. However, the availability of such an option will depend on the insurer’s discretion.

Yes. You should add a beneficiary to your joint life policy. In case both the policyholders die within the policy term, the beneficiaries will receive the policy amount and benefits easily if they have been a nominee in the policy.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.