- Sum Assured: Guaranteed minimum payout to beneficiaries in case of the policyholder's death.

- Top-Up Facility: Extra investments over regular premiums to boost wealth creation.

- Fund Switching: Reallocating investments among different funds to align with goals.

- Lock-In Period: Minimum duration before withdrawals are allowed, ensuring long-term discipline.

- Partial Withdrawals: Option to take out a portion of funds post lock-in for urgent needs.

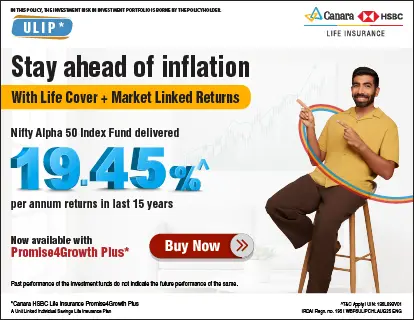

- Tax Efficiency: Premiums and benefits enjoy exemptions under Sections 80C and 10(10D) for savings.

2025-11-13

222 Views

7 minutes read

Share