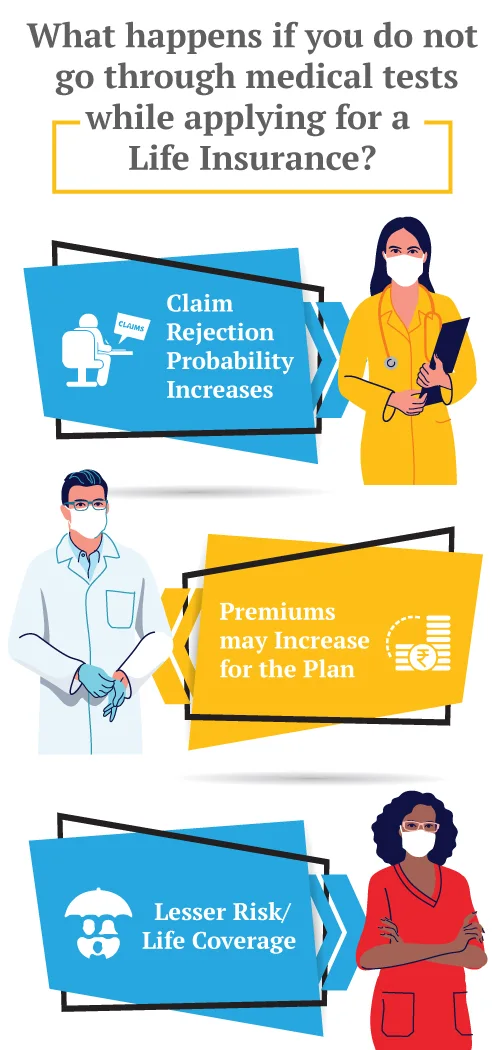

Risk is the basis of any insurance. In the case of life insurance, the risk is the likelihood that you are going to die within the policy term. The risk involved will decide the coverage you can be eligible for. The more the risk involved, the more will be the chances of you paying higher premiums.

Insurers assess your risk profile before providing you with life insurance. The basis of insurance is probability. Insurance is generally provided for those events whose probability of happening will not be very high. If there are high chances that something might happen to you, then you possess a higher risk for the insurer.

How much risk you possess for the company is based on a host of factors determined by the insurance company itself. One such factor is health. The risk that is external to you is already included while calculating the premium as it’s the same for all. But what plays a major part in differentiating premium rates is your health condition.

Your health plays a significant part in deciding your risk and ultimately the premium you will pay. The higher the risk, the higher will be the premium. Your general health parameters such as height and weight are checked along with specifics such as blood samples, etc.

For example, if you are overweight, you may be charged extra premiums as obesity brings with it certain health conditions.

Click here to Use - BMI Calculator

The process through which all these things are checked is called underwriting in insurance.