Written by : Knowledge Centre Team

2026-01-24

891 Views

6 minutes read

Share

Life cover assists one to face the future uncertainties, particularly with regard to the financial safety of the family. Virtually, anyone with normal and frequent income is eligible to receive life insurance cover, and so are you, despite the diabetes.

It is necessary to realise that provided you have a reasonable income and you are not at the critical phase of an illness commonly, you will be able to take out a life cover. Although such conditions as diabetes can bring a somewhat bigger premium than the individual with no underlying health conditions, it is worth it.

Finally, considering the cost-to-benefit ratio, life insurance will guarantee that your family is well off and does not experience the distress of not having you, even when your health condition changes in the future.

Key Takeaways

|

If you are diagnosed with diabetes, you are still eligible for life insurance. However, the plan you can get and the premium you need to pay will depend on the level of your diabetes. It will always be higher compared to a person who does not have any existing medical risks.

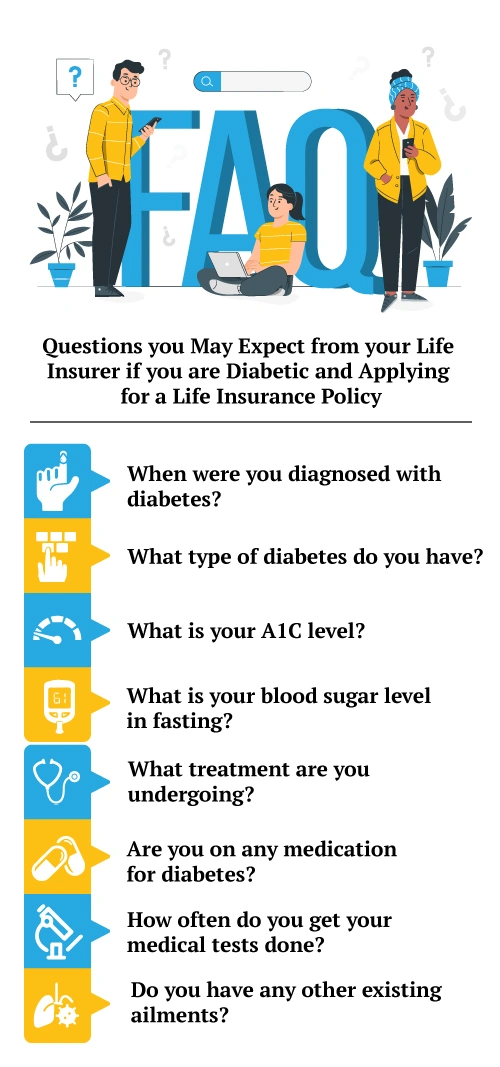

The insurance company evaluates each case based on several factors, like:

Age

Type of ailment (diabetes or other)

Stage of the illness (progressive or manageable)

Family health history

In the case of applying as a diabetic proposer, you are likely to receive a higher premium quote than normal. Only on rare occasions, the insurer may reject your application altogether, such as:

When the risk of early demise is either very high

The financial cover and cost do not resonate well

An OTP has been sent to your mobile number

Sorry ! No records Found

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

Getting life insurance as a diabetic is possible, but several factors influence your eligibility and premiums. Here are five key aspects insurers consider:

Diagnosed after 40 years: Lower risk assessment

Diagnosed before 40 years: Higher risk due to longer exposure

Maintaining these levels through consistent lifestyle habits and medication is crucial for securing life insurance.

The computation of the price of life insurance is against mortality risk. Diabetes:

Raises the likelihood of heart diseases.

Increases the chances of kidney failure, nerve damage or stroke.

Causes less lifetime expectancy when not dealt with.

Therefore, insurers take advantage of these risks by charging higher premiums. Nevertheless, this may have a drastic effect on your premium; however, early diagnosis, effective treatment, and a change in lifestyle can help significantly.

If you are diabetic, life insurance becomes even more crucial because:

It secures your family’s financial future if health complications arise.

Provides funds to cover liabilities like home loans, child education, or spouse’s retirement corpus.

Offers peace of mind knowing your family will not struggle financially in your absence.

Remember, the earlier you buy life insurance, the better your premium rates, even with diabetes.

Here are summarised tips for you to remember when buying life insurance with diabetes.

Maintain a healthy lifestyle: Control sugar levels through diet and exercise.

Keep medical reports updated: Share your latest HbA1c and sugar test reports.

Disclose all health conditions honestly: Concealing health issues can lead to claim rejection.

Apply early: Premiums are lower when you’re younger and healthier.

Compare plans: Understand features, exclusions, and riders before purchasing.

Consult your insurer’s advisor: Seek guidance for the best plans suited to your health profile.

Having diabetes shouldn't stand in the way of securing your family’s financial future. With timely medical care, proper blood sugar control, and consistent health management, getting life insurance is not only possible; it’s essential. While premiums may be slightly higher, the peace of mind and protection it offers far outweigh the cost.

Canara HSBC Life Insurance appreciates all these needs, which is why the company provides solutions that will enable you to plan with confidence regardless of your health condition. Become financially secure tomorrow by beginning today to build financial security for your family.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.