Written by : Knowledge Centre Team

2025-10-24

2185 Views

11 minutes read

Share

Smart people work in the present and plan for the future. If you look back, you are, what you are, today, because of the actions or incidents of the past. Life Insurance is a long-term investment, a hedge, protection, guarantee and assurance against the unknown.

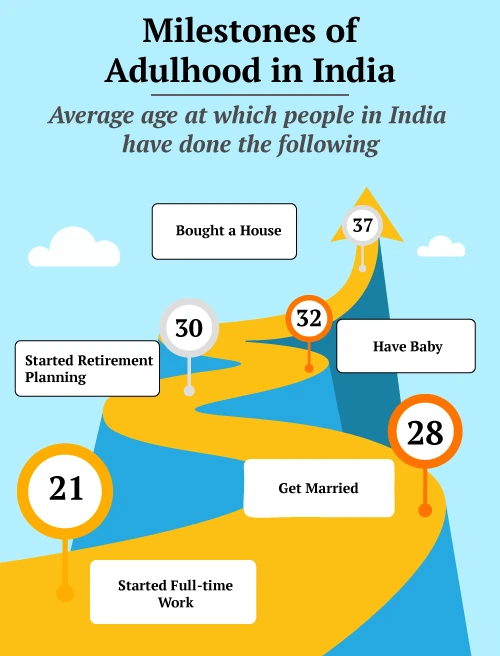

It is natural for 25-year-olds or persons who have recently begun their careers to wonder whether they should buy the best life insurance plan, which is generally associated with old age, ill-health, retirement or even death. But did you know that insurance cannot be purchased when you need it the most? Insurance companies do not extend coverage to ill persons, albeit pre-existing illnesses may be covered after a defined waiting period.

Life insurance may not be available when required and, ergo, insurance should be purchased when it is seemingly least required. Cost is proportionate to age. Start early to avail of a policy with a low premium. The premium remains unchanged throughout the term once you sign up.

From a savings and wealth creation perspective, the earlier the better, to enjoy the power of compounding. If you start saving and investing early on, your money will work hard by itself and grow multi-fold by the time you retire.

Investment cum insurance policies such as ULIPs allocate money in portfolios depending on age. If you are young, a large chunk of your investment will go to equities because over the long run, equities give unmatchable returns.

Portfolio managers move your money to debt instruments, to preserve wealth, as you age and approach retirement. If you start late, you may not be able to take advantage of the bull runs in the equity market and may have to stay content with capital-preserving debt instruments.

Contrary to popular perception, all 25-year-olds are not free from financial commitments. Some have to repay their education loans whereas others take care of their financially dependent parents. Responsible children from underprivileged families support their siblings until they are also financially independent.

At the age of 25, a person may or may not have existing financial commitments depending on their circumstances. However, as s/he traverses through the journey of life, the challenges and uncertainties are bound to increase. With marriage comes an added responsibility of caring for the spouse, and children bring in loads of joy along with dreams for their bright future.

In this game of life, what if you do not get another chance to handhold your loved ones and live through all those plans that you made together?

When you are young, you must lay a solid and sustainable foundation for your future. From a financial planning perspective, you must aspire to create wealth, have a dependable corpus that is not subject to market risks and create financial protection to safeguard your family in case of your unfortunate, untimely demise.

Primise4Growth Plus, offered by Canara HSBC Life Insurance, has four broad investment strategies and seven options of funds to help you multiply your investment. Automatic rebalancing maintains the specific allocation despite market fluctuations and thus your investments are maintained in the original % allocations.

Systematic Transfer Plans (STPs) allow transferring units from one fund to another fund depending on market movements. In the long run, ULIPs are proven to aid in creating wealth.

Guaranteed returns are possible if money is invested in safe instruments such as debts, bonds and G-secs. For example, the Guaranteed Income for Life gives guaranteed pay outs if you invest by paying premiums for a specific Premium Paying Term. The legacy and backing of top-class banking institutions such as Canara Bank, HSBC Life Insurance make it a reliable, dependable and trustworthy source.

All plans can go awry if God has made His plans for you. Hedge all risks with term insurance because your loved ones will still have to lead the rest of their lives with dignity and will need food, clothing, shelter and education.

Term insurance, such as iSelect Smart360 Term Plan, gives a lump sum amount called sum assured (SA) to the nominee, in case of your unfortunate demise. The disability riders get activated in case of total permanent disability. Such benefits act as supplementary protection to help tide over financial challenges. The future premiums are paid by the company and the life cover continues as usual.

Keeping in view the uncertainties of life, the volatilities in employment and rising costs of living, it is important to start financial planning early on. A comprehensive financial plan focuses on savings, wealth creation, risk coverage and post-retirement income. You gain by starting early but put yourself at grave risk if you do not.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.