Written by : Knowledge Centre Team

2026-02-17

3493 Views

8 minutes read

Share

India is a land of diversified culture and traditions. However, no matter from which part of the country you are, there is a common thread in our DNA. We all are programmed to save money for the future. Though we are not given financial education in school, every child, at some level, knows the importance of planting a tree today and enjoying the benefits in the future. The saving options may have changed over generations, but at the core, you need a savings option that secures the future of your loved ones.

You save to achieve your short and long-term goals. Savings plans are life insurance plans that give you an option to create a huge corpus over time to meet your future needs. The savings plans are created to help you get into the savings habit.

These plans are designed to reward you for your commitment to saving regularly and for a long time. In addition, they also offer insurance coverage which gives you security in life.

These three savings plans from Canara HSBC Life Insurance, have a range of features you can use. These features allow you the necessary investment flexibility you need to meet your financial goals.

Here are five hidden features of the above three saving plans that you should know:

Your goal is to protect your family financially under all circumstances. The goal of savings plans is the protection of your goals. If you pay your premiums on time, you receive a lump sum value on maturity that helps you complete your goals.

But, in case of your early demise, the investment in the goal may remain incomplete, affecting your family’s chance of meeting the goal. However, these three saving plans can help your family meet these goals even after an incomplete investment.

Here’s how:

Assuming you started investing Rs. 2 lakh a year in your child’s higher education goal. You will invest for the next 15 years and your goal is to build a corpus of Rs. 45 lakhs at the end of this tenure. However, unfortunately, you pass away in the fifth policy year, after investing only Rs. 5 lakhs in the plan.

The investment is far from sufficient to grow to Rs. 45 lakhs in the next 10 years. But, if you opted for a goal protection option within the plan, upon your death, the plan would pay the life cover sum assured to your family, i.e., they will receive Rs. 20 lakhs immediately.

Also, the plan will invest all the remaining premiums on your behalf, until normal maturity. Thus, giving your family the intended maturity value.

One important aspect to evaluate while doing any investing is taxation. If the income you earn from your investment is taxable, the taxes will eat a part of your returns on maturity. The savings plan is a long term plan, and you receive a decent size corpus on maturity.

In these savings plans, you don’t have to pay any tax on the maturity amount. You get to use the whole amount received for your goals.

The payment received from a life insurance plan is exempt from tax under section 10(10D) if the investments follow a simple rule:

“Annual premium investment in any policy year does not exceed 10% of the life cover sum assured in the policy”

So far as your investments into the saving plans follow this rule, your maturity value remains tax-free.

With age, your responsibilities and so your expenses increase. To meet the multiple responsibilities, you would want to continue investing in the new goal every few years. The limited investment period option allows you to free up your investment from one goal and focus on another after a short period of investment.

For example, you can choose to invest for only five years towards your goal of purchasing a house. After that, you will redirect your savings to other goals, while your home buying corpus continues to grow.

The cost of your child's education will increase, and there will be other mandatory expenses that are unavoidable. One of the best features of Promise4Growth Plus, Guaranteed Saving Plan, and Guaranteed Income 4 Life is that these plans let you choose your policy term.

So, you have the flexibility to decide for how many years you want to pay your premiums and will not be tied up until maturity.

You can use any of these plans for lifetime coverage and even plan to leave a legacy for your family after your natural demise.

While the ULIP plan can continue to grow your invested corpus, you can:

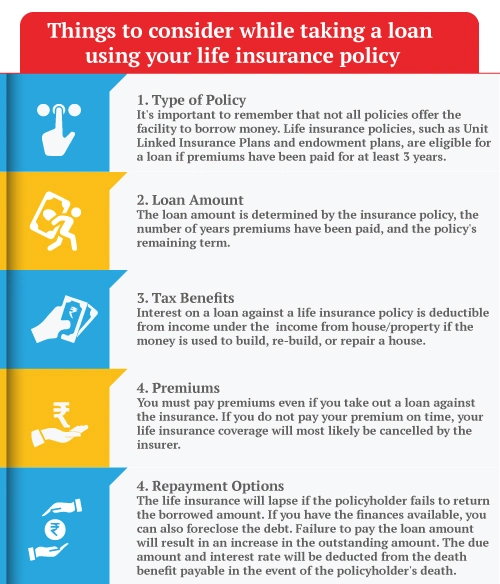

You invest in savings plans for your long-term goals, mostly. However, you may require funds to meet your short-term needs. These saving plans acquire cash value which increases over time. While you will receive the maturity value at the time of maturity, what can you do if you need the money a few years before that?

For such situations, you can borrow money at a low rate of interest against the policy and fulfil your need. The policy will continue in the meanwhile, and you can either repay the entire loan before maturity or the amount is deducted from the maturity value with interest.

Thus, the savings plans from Canara HSBC Life Insurance can help you look after multiple financial needs. All you need to do is to know your savings plan well and use the right features.

An OTP has been sent to your mobile number

Sorry ! No records Found

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.