Written by : Knowledge Centre Team

2025-10-03

914 Views

7 minutes read

Share

A daughter’s wedding is one of the most beautiful celebrations in a family. You dream of giving her a grand wedding filled with love, joy, and unforgettable memories. Many parents start saving gold or money with this dream in mind, but it is not enough. The real question is how to plan smartly and early so that you can give your daughter the best wedding memories. In this blog, we will discuss the same. Stay tuned

Key Takeaways

|

A sufficient life insurance can be of great help in achieving your future goal. Read on to find out how.

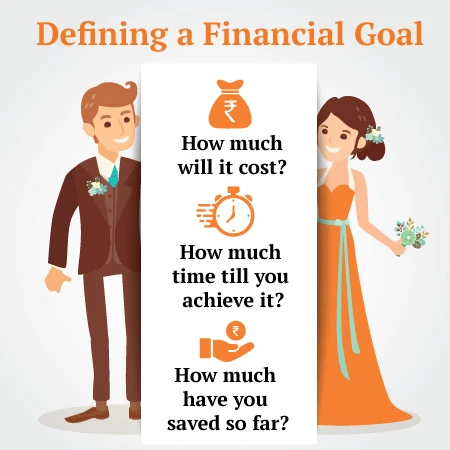

Planning your daughter’s wedding begins with setting a clear financial goal. A lavish wedding includes multiple expenses, including venue, décor, outfits, jewellery, catering, and more. To prepare well, you need to estimate how much you are based on your lifestyle and expectations.

In cities like India, families often plan wedding budgets that start around ₹15 lakh and can go much higher, depending on the scale of the celebration. Once you assign a number to your goal, you can start planning how to reach it with the right investments.

This planning can begin by assessing the number of years you have before your daughter is ready for the next chapter of her life. This can be found out by deducting your daughter’s present age from the probable marriage age. For example, if your daughter is five years old right now, you may have approximately 20 years before she begins to think about marriage. This is the time to set aside money for your savings to accumulate the funds you need for this goal.

Based on this timeframe, if your current budget is ₹15 lakh, 20 years from now, you will need approximately ₹54 lakh to maintain the same standards. Considering your current savings for the goal, you can either leave it as is or consider transferring it to the new investment plan.

An OTP has been sent to your mobile number

Sorry ! No records Found

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

When you have 15 to 20 years to save for your financial goal, you have multiple investment opportunities open for you. However, you want only the safest way to reach the goal, even if you have a high-risk appetite for investments. You would want the investment to:

Work without your regular involvement: You should be able to set it up once and let it grow on its own, without needing frequent reviews or adjustments.

Safeguard the growth of your investment: It should protect your returns from sudden market dips and ensure consistent growth through a balanced investment strategy.

Safeguard your daughter's goal: During critical times, the investment should continue and provide the full amount at the right time.

Provide maximum tax efficiency: It should help you save on taxes under applicable sections while keeping the maturity amount tax-free.

There is only one investment option that can meet all four conditions simultaneously, the ULIP investment plan.

A Unit-Linked Insurance Plan for investment is a plan that offers diverse investment options and tax savings under Sections 80C and 10(10D). ULIPs offer multiple fund options to allocate your invested money according to your risk appetite and comfort level.

Being a life insurance plan, ULIPs also offer death benefit to the family, ensuring your goals are met even in your absence. These features enable ULIPs to help protect your family’s goals in the event of mishaps and provide financial support to your family

If you want to accumulate around ₹54 lakhs in 20 years for your daughter’s wedding, ULIPs can be a smart and tax-efficient option. Assuming an average return of 8% per year, you would need to invest about ₹9,000 each month, or around ₹1.1 lakh annually.

When investing in a ULIP, you should keep two important things in mind:

ULIPs offer tax-free maturity under Section 10(10D), but only if certain conditions are met, especially for plans purchased after February 1, 2021:

Your total annual premium across all ULIPs should not exceed ₹2.5 lakh in any financial year.

For each policy, the premium must not exceed 10% of the sum assured.

If either of these limits is crossed, the maturity amount becomes taxable as capital gains.

Example: If you invest ₹1.1 lakh per year and your sum assured exceeds ₹11 lakh, your plan remains fully tax-exempt. Also, ensure your sum assured is always at least 10 times your highest expected annual premium.

ULIPs enable you to invest additional funds through top-ups. But to keep the tax benefits:

Your total premium (base + top-ups) should stay under ₹2.5 lakh in any financial year.

The total annual premium should always be within 10% of your sum assured.

This way, you can boost your savings without losing tax advantages.

Condition | Is Maturity Value Tax-Free? |

Annual premium ≤ ₹2.5 lakh AND ≤ 10% of sum assured | Yes |

Annual premium > ₹2.5 lakh in any financial year | No (Taxed as capital gains) |

Annual premium ≤ ₹2.5 lakh BUT > 10% of sum assured | No |

As the wedding date approaches, protecting your savings becomes just as important as growing them. ULIP plans offer smart strategies to safeguard your goalskeep your goal safe from market risks.

You can select one of the four investment strategies this plan offers. These strategies can benefit your investment from equity market performance while safeguarding your gains:

You can use this option with any of the other three investment options.

For example, consider that while investing ₹ 1.1 lakh a year, you will have a life cover of ₹ 15 lakhs for the 20-year plan. If a death claim is filed in the 10th policy year, your family will receive:

Your daughter’s wedding is one of the most cherished events in your life. With early and smart financial planning, you can turn this dream into reality. A ULIP investment plan by Canara HSBC Life Insurance helps you build the right savings, secure your goal, and enjoy tax benefits while staying protected from market ups and downs. Now is the right time to begin planning for the future you envision.

Talk to our advisor today or get a personalised quote to start your journey towards a grand and joyful celebration.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.