Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

When it comes to secure and low-risk investment avenues in India, Kisan Vikas Patra (KVP) stands out as a trusted option for individuals who prioritise capital protection and guaranteed returns. Launched by the Government of India and offered through India Post, KVP was originally created to encourage long-term savings habits, especially among rural investors. Over time, it has become a reliable investment tool for anyone looking to double their investment over a fixed period without worrying about market fluctuations. Let’s explore everything you need to know about Kisan Vikas Patra.

Key Takeaways

Kisan Vikas Patra offers assured, fixed returns regardless of market volatility, making it a reliable choice for conservative investors.

At the current interest rate of 7.5% (FY 2025–26), your investment doubles in approximately 115 months, ideal for long-term financial goals.

KVP certificates can be held individually, jointly, or even on behalf of a minor, allowing flexibility for families and senior citizens.

Although KVP doesn't qualify for deductions under Section 80C, the predictable and compounding returns compensate for the lack of tax incentives.

With a 30-month lock-in period and premature withdrawal allowed only under specific conditions, KVP balances capital discipline with partial liquidity.

Build Guaranteed Savings for Your Future Goals

Enter OTP

An OTP has been sent to your mobile number

Didn’t receive OTP?

Application Status

Name

Date of Birth

Plan Name

Status

Unclaimed Amount of the Policyholder as on

Name of the policy holder

Policy No.

Address of the Policyholder as per records

Unclaimed Amount

Sorry ! No records Found

. Please use this ID for all future communications regarding this concern.

Request Registered

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

Categories of Kisan Vikas Patra (KVP)

Kisan Vikas Patra (KVP) is divided into 3 categories, which are:

Category 1 - Joint A- This is allotted to two adult members jointly. The payment of this category is made to either the account holders or the one who lives on till the plan's maturity.

Category 2 - Joint B- This is allotted to two adult members jointly; however, the payment is made to only one holder or who lives until the plan's maturity.

Category 3 - Certificate of Single Holder- This is allotted to a single adult member or on behalf of a minor holder.

What is Kisan Vikas Patra?

Kisan Vikas Patra, also recognised as KVP, is fundamentally a savings scheme available at the Indian Post Offices in the form of certificates. This savings scheme functions as a fixed-rate savings plan aiming to multiply your investment after completing a pre-decided period (115 months).

Initially launched to support farmers, this scheme is now a trusted savings tool for anyone seeking safe, stable returns, especially in rural areas with limited access to banks. Even if you already invest in other financial instruments, KVP can serve as a valuable addition to your portfolio by boosting your long-term financial plan. Even if there is any other savings plan already added to your investment portfolio, you must not stop exploring other available options.

Let us understand in detail what is Kisan Vikas Patra, how it works, its features and benefits, and eligibility criteria so that you can make an informed decision.

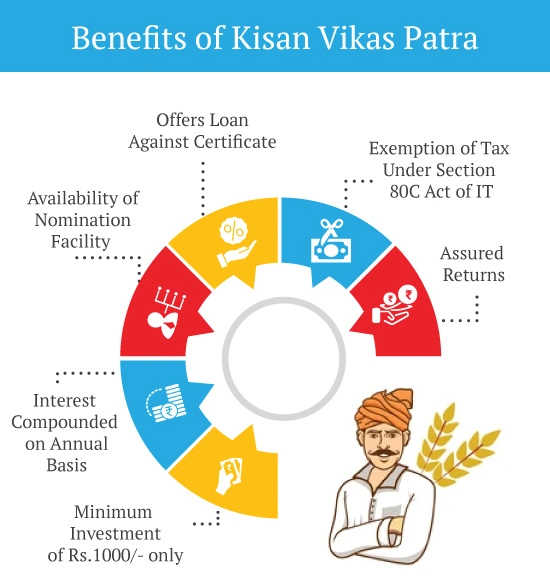

7 Features of Kisan Vikas Patra

Some of the Kisan Vikas Patra scheme's significant features are:

Guaranteed returns: The saving scheme was originally made to provide financial relief to the farmers owing to the loss incurred from unexpected weather conditions. This allows the scheme holder to receive the guaranteed sum of returns despite any market fluctuations.

Maturity period: KVP scheme holds a maturity period of 124 months; you can claim your amount after completing this period. However, if you decide not to withdraw your investment, it will continue to receive interest till you withdraw it.

Fund protection: The fund you have invested in this scheme is free from any market uncertainties. The scheme owner will be entitled to get the whole investment amount and profit when the policy tenure ends.

Interest rate: The interest rate of Kisan Vikas Patra varies according to the number of years you've remain invested in the scheme from the time of purchasing it. KVP scheme currently holds an interest rate of 6.9% for the quarter from January 2021 to March 2021. As the interest gets compound, you will gain more returns on your deposit.

Tax deductions: The scheme attracts no tax deductions under Section 80C of the Income Tax Act, and the returns received are fully taxable. Nevertheless, Tax Deducted at Source (TDS) is exempted from withdrawals after the maturity period.

Rules on premature withdrawal: Even though the maturity period of the scheme is 124 months, its lock-in period is merely 30 months; before that, you are not permitted to encash the policy, except in the scenario of the account holder's unforeseen death or a court mandate.

KVP certification: If you make the scheme's payment in cash mode, you will receive the issued certificate on the spot. However, in the case of a money order, cheque, or demand draft, you will have to wait until the post office receives the amount.

Kisan Vikas Patra - Interest rates

The interest rate of the KVP scheme is subject to frequent fluctuations as per the declarations made by the Finance Ministry. Currently, the interest rate of the scheme is 6.9% per annum, which doubles your investment within the tenure of 124 months.

Unfortunately, no tax deductions are attracted under the Kisan Vikas Patra scheme. The interest you receive under the scheme is liable for taxation under the category 'Income from other sources, paid every year. Also, a 10% TDS is deducted from the interest.

Nevertheless, the ultimate value on maturity is exempted from tax deductions.

*Disclaimer: Tax benefits are subject to change in tax laws. Please consult your tax advisor.

Did You Know?

The discount rate for calculating SSV can be up to 50 basis points higher than the 10-year G-Sec yield.

Source - Business Standards

Who should Invest in the KVP Scheme?

Any individual of 18 years of age or older is eligible to purchase Kisan Vikas Patra.

They can get it from their nearest post office. This saving scheme is majorly preferred by people of the rural sector in India as they don't have a bank account.

A KVP can be purchased for a minor or purchased in the form of a joint account.

If purchasing a KVP for a minor, it is essential to mention the name of the guardians and the minor's date of birth.

A trust foundation is also eligible to purchase a KVP. However, a member of the Hindu Undivided Family (HUF) and a Non-Resident Indian is not eligible to buy a Kisan Vikas Patra.

Eligibility Criteria for Kisan Vikas Patra

To meet the eligibility criteria to invest in the Kisan Vikas Patra, you must fulfil the following requirements:

The person applying for the scheme should be an adult residing in India.

The person investing on behalf of a minor should be their guardian or parent.

NRIs and a Hindu Undivided Family (HUF) are not eligible to apply for Kisan Vikas Patra.

Documents Required for KVP Saving Scheme Certificate

To acquire the KVP certificate, an applicant of the KVP scheme needs to provide self-attested copies of the following documents:

For KYC verification, identity proof can be your Aadhar card, PAN card, Voter ID Card, Driving License, or Passport.

A duly filled KVP application form

Address Proof

DOB(Date of Birth) certificate

Glossary

Surrender Value: Amount a policyholder receives after terminating an insurance before maturity, lower than the total premiums paid.

Lapsed Policy: A policy that becomes inactive due to non-payment of premiums, leading to loss of benefits and coverage.

Dividends: A part of companies profit that is shared with shareholders.

Wealth Accumulation: Process of growing financial assets over time through disciplined savings and investment strategies.

Maturity Benefit: Guaranteed sum or accumulated returns paid to the policyholder at the end of policy term, provided active policy.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

Savings and Investment Plans from Canara HSBC Life Insurance

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.