Written by : Knowledge Centre Team

2025-12-11

4326 Views

11 minutes read

Share

Life insurance and retirement plans are necessary to safeguard your family's future, but very often, the jargon used by the banks and insurance agents is difficult to understand.

These kinds of misunderstandings can lead to many problems in the future. People may overspend or make extravagant plans with the confidence that their savings plans will cover them. Later, they may realise that the actual payout is much lower than expected."

This is a common issue faced by customers across the world, as they are expecting benefits from a policy that was never part of the contract. You may often hear terms like 'guaranteed returns' and 'assured returns' used interchangeably, but they are not the same. While both relate to the financial benefits of savings plans, they work very differently and can impact your payout. Thus, to make better financial decisions and avoid unpleasant surprises, it’s essential to know the difference between guaranteed and assured returns, starting with what each term truly means.

Key Takeaways

|

Guaranteed returns are the amount of money you receive at the end of your investment or insurance plan, regardless of how the markets perform or the financial condition of your insurer or bank. When you choose a plan with guaranteed returns, the amount is fixed at the time of purchase, so you always know exactly what you will receive.

If you are someone who values financial stability, these plans offer you predictable benefits and peace of mind.

An OTP has been sent to your mobile number

Sorry ! No records Found

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

You receive a fixed maturity benefit that is mentioned at the time of buying the plan.

Your returns remain unaffected by market fluctuations or the performance of your insurer. You get the promised amount regardless of external conditions.

These plans are ideal if you prefer low-risk savings options and want to avoid market-linked volatility.

Along with investment benefits, you also get life cover. In case of an unfortunate event, your family will receive the guaranteed sum assured.

You enjoy tax benefits under Section 80C on premiums paid, and the maturity amount may also qualify for tax exemption under Section 10(10D), subject to prevailing tax laws.

Regular premium payments help you build disciplined savings and stay focused on long-term financial goals.

You get complete peace of mind knowing that your returns are protected, even if the financial health of the insurer or bank changes.

Regardless of its financial health, the insurance provider is liable to pay policyholder the pre-determined sum of money upon maturity. Such plans involve fewer risk factors and often better benefits. Some of the key benefits are as follows :

The amount for guaranteed returns is usually less than how much an assured return could be. This is because the bank wants to minimise its risk factor to avoid bankruptcy. Premiums may be higher. Some of the key disadvantages are as follows:

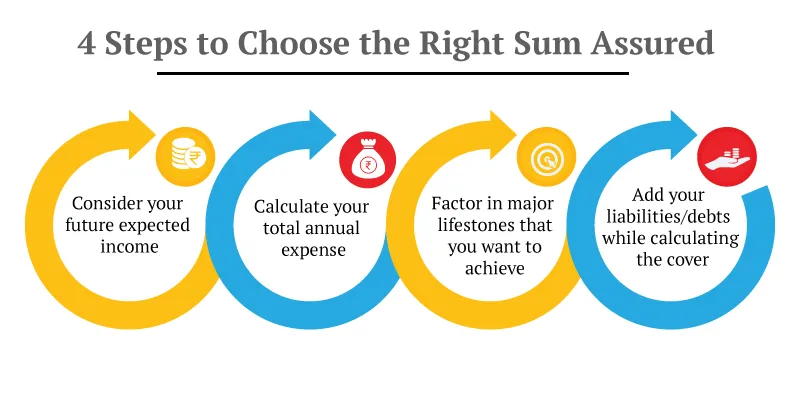

Before you buy a life insurance plan to meet your investment goals based on guaranteed returns, consider the following factors:

Assured returns are similar to guaranteed returns; you receive a fixed benefit regardless of how the market performs. Even if the market underperforms, you still get the payout you were promised.

However, assured returns are not always backed by the insurance company’s financial health. If the bank or issuer goes bankrupt or has insufficient reserves, you may not receive the assured benefit. In such cases, smaller banks often offer assured returns instead of guaranteed ones to avoid overextending their liabilities. Some key Features are as follows:

Assured return plans offer consistent and low-risk earnings. Here are the key features you should know before investing:

You receive a fixed return amount agreed upon at the time of purchase, regardless of market performance.

Your returns stay stable even if equity markets or other financial instruments fluctuate.

The returns are promised by the issuer, but they depend on the financial health and credibility of the institution.

These plans carry minimal risk, making them ideal if you seek stable income rather than high-risk, high-return options.

Most assured return plans have a lock-in period or fixed maturity date, during which the returns remain unchanged.

You may not be able to switch or withdraw funds easily before maturity due to rigid plan structures.

Compared to market-linked products, assured returns usually offer modest growth but higher predictability.

There are different types of investment options available in India that offer an assured return on investment.

The minimum sum payable by the insurer in case of your untimely demise is referred to as the sum assured. This implies that the sum assured is the actual coverage offered by the plan you chose. It also directly determines how much money you have to pay a premium for your instalments.

The sum assured amount is something you have to look out for when picking out your investment plans.

While assured returns offer consistency and security, they also come with certain limitations that you should consider before investing.

Before buying an Assured plan, you should consider the following factors:

Lets quick comparison between guaranteed and assured returns in the form of a table:

Parameter | Guaranteed Returns | Assured Returns |

Definition | A pre-decided sum paid irrespective of market or company performance, contractually mandated. | A promised return that is highly probable based on company policy, but not legally guaranteed. |

Backed By | The insurer’s/legal issuer's contractual obligation to pay as per the policy. | The company’s commitment or promise, not legally enforceable. |

Dependence on Financial Health | Payment is legally required, regardless of the issuer’s financial health (subject to the solvency of the company). | Payout depends on the issuer’s ability to honour commitments; risk increases if the issuer faces issues. |

Risk Level | Very low returns are protected and contractually binding. | Moderate returns are expected, but not legally protected. |

Common Providers | Large insurance companies or highly regulated institutions. | Smaller banks, NBFCs, or lesser-regulated entities. |

Regulatory Oversight | Strictly regulated by IRDAI (for insurance) or respective financial watchdogs. | May not have the same strict regulatory framework as guaranteed products. |

While guaranteed returns, assured sum, and assured returns are all elements of life insurance policies and savings plans, you do not always have to buy two separate plans to avail of these benefits. Most policies offer both a sum assured and a guaranteed return, with the catch being that the you will receive only one of the two. The risk you want to take on when you choose a savings plan may not always be clear at the outset, which is why you should have the necessary knowledge to choose the right plan for you.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.