Written by : Knowledge Centre Team

2025-09-29

2880 Views

6 minutes read

Share

Life is synonymous with change and growth. It is normal to expect growth in your age, family, income and wealth while you are alive. With this normal growth, an increasing number of other factors like expenses, financial needs and goals also take shape.

Now term insurance cover is to ensure that your family can maintain their lifestyle as you have left it in the case of your early demise. So, the question, ‘Shouldn’t your term life insurance keep up with your life?’ The simple reason would be to ensure that your life cover keeps up with the growing demands of life. But, does it really work like that? Or, is there anything else you should be looking for?

Key Takeaways

|

Your financial needs are defined by the following:

Monthly survival expenses

Lifestyle habits and spending

Medical conditions

Number of family members

Children

Annual Income

Long-term liabilities

Changes to the above define the change in your financial status, especially income. A long-term income ultimately defines your lifestyle and financial status.

If you consider your life starting with your first paycheque, you only expect the income to grow. At the same time, other factors like family and lifestyle will also grow with time. Another factor that should prompt you to increase your life cover is a long-term loan, such as a home loan or an education loan.

Thus, to keep up with your growing family and income, your term insurance cover should also grow. Ultimately, you should have a life cover large enough to take care of the following for your family:

Pay off the long-term loans

Meet their important financial goals, i.e., the child’s higher education and marriage

Look after their survival and important lifestyle expenses

Usually, a life cover that is 10 to 15 times your annual income is enough to cover all three financial needs for your family.

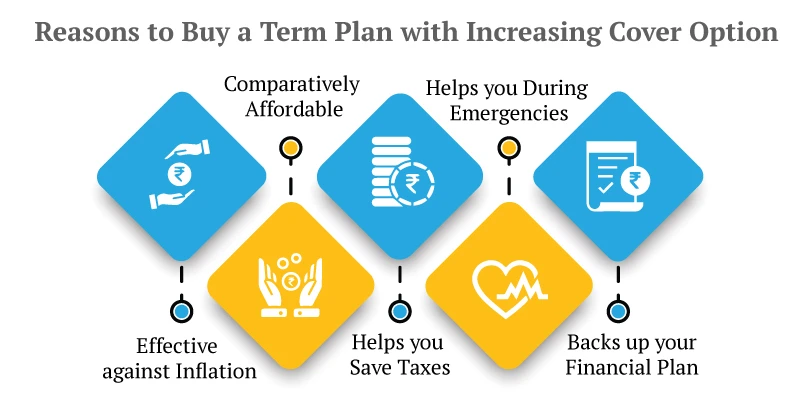

Since you need a life cover of at least 10 times your annual income, the easiest solution is term life insurance. You have more than one option to increase your term life cover:

Let’s understand this with a scenario.

Raj, 30, buys a ₹1 crore term plan.

At 35, he takes a ₹60 lakh home loan.

At 36, he becomes a father.

At 40, his child's education cost is estimated to be ₹25 lakhs.

If Raj sticks to the initial ₹1 crore cover, it won’t suffice to meet all his family’s future needs. But if he opts for an increasing cover plan, his sum assured will gradually become ₹2 crore, offering adequate protection at a nominal additional cost.

iSelect Smart360 Term Plan by Canara HSBC Life Insurance is one of the most versatile life insurance plans with increasing cover benefits. The plan offers two types of incremental life cover options:

Life stage increment

Increasing cover at a fixed rate

You would want to choose the second option if you want to continue increasing your life cover without increasing your premiums. Apart from the increasing cover, iSelect Smart360 Term Plan by Canara HSBC Life Insurance offers multiple additional benefits such as regular income payout and terminal illness cover. Regular income payout is especially useful in keeping the headache of income-generating investments after the claim. The critical illness options come inbuilt into the base plan, ensuring protection against diseases like cancer, heart ailments, and more.

Term life cover is an important part of your financial safety needs, especially when you have dependents. Selecting features such as growing life cover and regular income features helps increase the benefits of your term insurance plan. Increasing cover is a great way to ensure your single-term insurance plan remains relevant for your family for a long time.

Plans like iSelect Smart360 Term Plan by Canara HSBC Life Insurance offer flexibility, affordability, and peace of mind, making it easier than ever to increase your life cover at a nominal rate. So, don’t wait until life changes catch you off guard. Choose a term plan that grows with you and secure your family’s tomorrow.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

Canara HSBC Life Insurance offers online term insurance plans to secure your family financially in your absence.