Written by : Knowledge Centre Team

2025-09-27

1620 Views

10 minutes read

Share

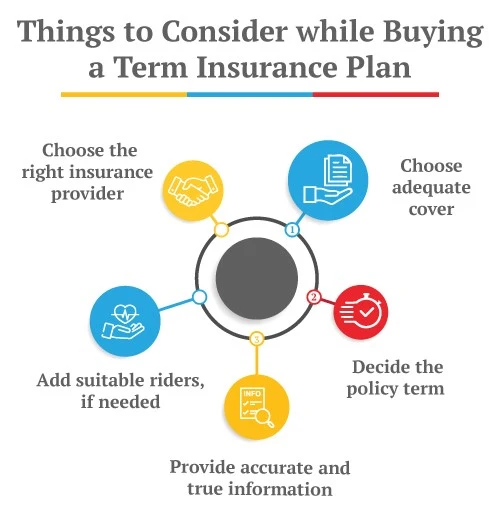

Life is unpredictable, and thus having a term insurance plan is not an option; it is a must to secure the future of your loved ones. It offers financial protection to your loved ones in the event of your untimely demise.

You can choose a term plan or return of premium with a term plan, depending on your needs. A term insurance plan with return of premium promises to return all the premiums you have paid till the policy matures if you survive the term without a claim. That makes a term plan with a return of premium almost a free-of-cost safety net for the family. While both provide life cover, the way they handle premiums, maturity benefits, and flexibility differs.

Let’s explore both options in detail to help you make the right choice for your financial future.

Also Read - What is Term Insurance?

Key Takeaways

|

You can opt for either of the two plans. The underlying reason for buying a protection plan is the same: to secure the future of loved ones under all circumstances. However, both plans are different in a few aspects that are listed below:

An OTP has been sent to your mobile number

Sorry ! No records Found

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

Under the iSelect Smart360 Term Plan by Canara HSBC Life Insurance, you can choose to have the death benefit paid as a growing income as well.

Assume you buy a term insurance with the return of premium option. Since you want to get a cover of ₹1 crore, you have to pay a premium of ₹7,500 every year. Your policy tenure and premium payment tenure are 10 years, which means you have to pay ₹7500 every year for the next ten years to keep your policy active. Two cases can arise after you buy the plan:

Untimely Demise: In case of your untimely demise, the insurance company will pay your nominee a sum assured of ₹1 crore.

You survive the Policy Tenure: If you survive the policy tenure, you will receive all the premiums you paid during the 10 years. Hence, you will receive ₹75,000 at the end of 10 years.

In either case, you get something back if you buy a term insurance with a return of payment plan.

A TROP plan is ideal for you if:

You are uncomfortable with the idea of “no returns” on survival

You have a steady income and can afford slightly higher premiums

You want a disciplined savings option with guaranteed returns

You’re looking for financial backup at policy maturity, possibly during retirement

A regular term plan is suitable if:

You’re seeking high-life coverage at the lowest cost

You’re younger and want long-term protection up to age 99

You’re investing elsewhere and don’t mind the absence of survival benefits

When it comes to term insurance, the ideal plan isn’t just about low premiums or high returns; it’s about securing your family’s future with flexibility and confidence.

So, if you prefer the affordability of a regular term plan or the value-added benefits of a return of premium plan (TROP), this plan adapts to your evolving needs. Features like sum assured upgrades for life events, customisable payout options, and critical illness riders ensure that you’re not just buying a policy; you’re investing in a lifelong safety net.

Ultimately, the right plan is the one that complements your life stage, aligns with your goals, and leaves no room for financial uncertainty. With iSelect Smart360 Term Plan by Canara HSBC Life Insurance, you don’t have to choose between practicality and peace of mind, as you get both.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

Canara HSBC Life Insurance offers online term insurance plans to secure your family financially in your absence.