Written by : Knowledge Centre Team

2026-06-23

897 Views

11 minutes read

Share

ULIPs or unit-linked insurance plans are life insurance plans specially crafted to help you meet your long-term financial goals. One of the major differences that ULIP has over other investments is that along with all the investment growth it can ensure the achievement of your goal despite the natural contingencies.

Thus, if you have important financial goals for your family, which you must achieve, such as a child’s higher education, ULIPs could be the best options to use. But there are hundreds of ULIPs in the market. So, how do you choose the best of them?

Here are six simple tips you can follow to buy the best ULIP for your financial goal:

There are major four types of funds namely equity, debt, balanced, and liquid funds available in ULIPs in India. You can choose anyone or two, or a mix of them as per your need for safety and growth of the invested capital. An equity fund can maximise the growth of your investment if allocated for a longer period, but the risk is also high.

Read to find out whether the risk involved in ULIPs the same as equity shares.

Whereas debt fund provides stable growth to the investment albeit at a slower rate. Before allocation in a fund, you can check at least 5 years of performance to have a past view.

A balanced fund is a mix of equity and debt funds to balance the return as well as risks. The experienced fund managers prefer equity fund for 5 to 10 years for maximum growth and thereafter in debt or liquid funds to secure the asset.

However, investors are allowed a maximum number of times to switch from one fund to another during the policy term from the beginning to last. It is given to grow and save the asset/premium invested in the best ULIP in India.

ULIP plans in India serve the objectives of both investment and life cover under one policy. ULIP plan products are designed to meet your long-term financial goals, for example, children’s marriage and higher education, family tour, etc.

But ULIP also provides financial cover to the family and dependents of the policyholder if he/she will be no more during the policy term. This life cover, however, is not just for taking care of the basic financial needs of the family-like, like kitchen expenses and loan repayments.

This life cover ensures that your family can achieve the goal you set out to meet in the first place. For example, Promise4Growth Plus ULIP plan from Canara HSBC Life Insurance continues to invest in the plan until all the due premiums are paid after the death of the policyholder. Thus, while the family receives a sum assured amount upon your death, the investment also continues. They will receive the maturity value you intended and meet their financial goal ultimately.

Therefore, choosing the correct life cover in ULIP plans is important. Also, this life cover amount will decide the maximum amount you can invest in a ULIP every year, without losing your tax benefits.

Your annual ULIP investment should not exceed 10% of the life cover amount to stay tax-exempt. Plus, if you have bought a ULIP plan after 1st Feb 2021, your maximum tax-free ULIP investment can be Rs. 2.5 lakhs in a year.

One of the objectives of investing in ULIP is wealth creation. It helps policyholders in creating wealth to fulfil the goals of family members like higher education and marriage of children, etc. Life cover is to ensure that such important goals do not suffer from a disastrous mishap in your life.

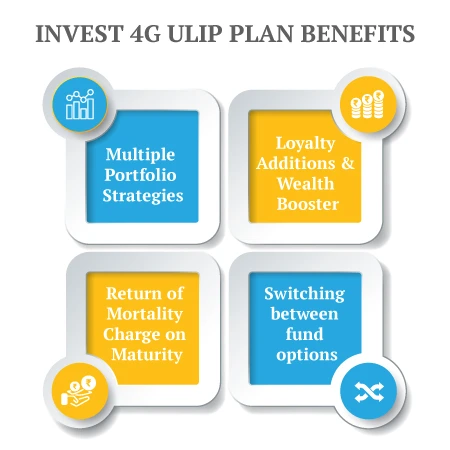

Thus, while equity investment is a tool for long-term wealth, ULIPs offer other perks to long-term investors. If investors stay for the long term then insurance companies also offer Wealth Boosters Bonuses and Loyalty Additions for maximum growth of assets.

Learn how to plan your long-term financial goals with ULIP.

Unit linked insurance plans or ULIPs are allowed to apply the following charges on the investment:

The best ULIP plans in India, including Invest 4G plan, apply minimal charges. For example, Promise4Growth Plus plan only applies the Fund Management Charge and Mortality Charge on your investment.

The Fund Management Charge or FMC is capped at 1.35% of the annual fund value in the case of equity funds. It is even lower for debt funds.

The mortality charge is deducted during the premium paying term and it grows lower as your corpus value grows. It becomes zero once your ULIP corpus grows equal to or more than the Sum Assured.

Policies like Promise4Growth Plus can also return the mortality charge at maturity if you have selected the option.

Click to use : ULIP Calculator

Your investment into ULIP plans is eligible for tax deduction under section 80C and the maturity amount is tax-exempt under section 10(10D). As per the section 80C limit, up to Rs. 1.5 lakhs is deductible in a financial year and is deducted from the investor’s taxable income.

Section 10(10D) allows for the maturity amount to be exempted from Income Tax. You need to take care of the following conditions to ensure a tax-free maturity value from ULIPs.

ULIP plans have a single role to play in your financial life, ‘to help your family achieve their important goal, regardless of your presence.’ In this role, protection is a single and settled aspect. However, when it’s about investment management and growth, you have a lot to gain with the right features:

Thus, the best ULIP plans in India can offer better growth to your investment and protection to your family’s aspirations. If you can select the best ULIP plans with relevant features and benefits, you can invest stress-free for the future of your family.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

Canara HSBC Life Insurance offers online ULIP plans that blend life insurance protection with investment growth, helping you build wealth while securing your family's future.