Written by : Knowledge Centre Team

2026-07-28

900 Views

5 minutes read

Share

Investing is a regular activity. You can invest your surplus and withdraw money when you need it. However, without investment management, you may find your investments slacking. Adequate and timely investment management can help you optimise your investment needs with the market growth.

While financial planning gives you an idea of your financial needs and resources, investment management starts with the execution of the plan. The moment you want your money to work harder for you, you will face the challenges and questions of investment management.

If you buy and sell stocks, that does not amount to investment. Such actions are merely transactional.

Handling financial assets and devising prudential strategies for acquiring and disposing of assets from your portfolio is a better definition of investment management.

Some of the commonly used terms to refer to investment management:

Scope of investment management:

Must Read - What is Net Present Value?

Investment management must account for the following important factors to provide effective guidance to your money. These factors are usually a part of your financial planning exercise:

Investment managers are key people in managing your money, growing it and returning it to you as safely as possible. They work under tremendous risk and invest your money keeping in view your financial objectives and your risk appetite. However, all investments have one objective in common-to grow your money. The aspired quantum of growth may vary depending on the risk appetite.

Some of the common avatars of investment managers:

Investment styles vary across investment experts and also depend on your objectives and timelines. Different investment styles can also carry different investment risks and your choices will depend on your risk appetite:

Know More - Passive Investing

Safe income funds will focus on generating income through fixed income securities like bonds and debentures. Aggressive income funds invest in blue chip equity stocks to generate income through dividends.

Also Read - Income from Salary

You can rely on different performance measures to assess the results of your investments over time. Each method offers a unique perspective and should be used in appropriate scenarios. For example, CAGR is the most common method for representing mutual fund growth, while IRR would be more appropriate for regular investors.

You can consider any of the following measures to assess your investment choices:

The majority of the portfolio investment options in India provide a CAGR for their historical performance.

Here are three popular investment options and their CAGR over a period:

Must Read - NPS Withdrawal Rules

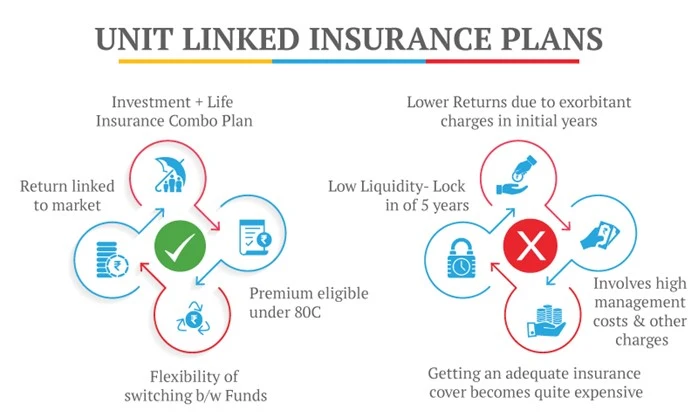

The CAGR of NPS and ULIP can vary a lot due to the range of fund choices within these investments. You can invest in a safe portfolio consisting of mostly government securities or invest in an aggressive portfolio of majorly equity stocks. The higher the risk, the higher your long-term returns can be.

Another factor you should consider is the bonus additions available to long-term investors in ULIPs. ULIPs like Promise4Growth Plus from Canara HSBC Life Insurance add wealth boosters and loyalty bonuses if you continue to invest for more than 5 and 10 years. Thus, your IRR from the ULIP plan will be very different from the CAGR reflected by the funds.

Investment management ensures your money is diversified across asset classes and financial instrument. The investment is made basis a clear growth plan, factoring in your risk appetite, and short/medium/long-term financial goals. Strategizing investment will help reduce transaction costs, save on taxes and fetch a better return on investment.

An OTP has been sent to your mobile number

Sorry ! No records Found

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.