Written by : Knowledge Centre Team

2026-01-02

1053 Views

8 minutes read

Share

You must have come across the term “Liquidity” in personal finance. So, what is liquidity? And why is liquidity so important in financial planning? In simple terms, if you can give away your asset and get cash in return, that is liquidity. If such an exchange is very difficult, your asset is illiquid, whereas if it is super easy, your asset is highly liquid. Therefore, the degree of ease in exchanging assets for cash determines the degree of liquidity.

If your assets can be exchanged for cash without losing their value, your investments are “liquid”. In most cases all assets are liquid, but what differentiates one asset from another is the degree of liquidity.

“Some investments are more easily turned to cash whereas others will need time and effort.”

Personal financial planning requires you to park some funds in asset classes that are highly liquid so that you have money in hand for emergencies. These financial instruments may not necessarily give better than average returns. At the other end of the spectrum, you must also invest in assets that could be illiquid but gives market-beating returns in the long run.

Investment liquidity has the following characteristics:

Also Read - How to Invest Money?

Highly liquid instruments allow you to withdraw money anytime and anywhere. No restrictions whatsoever. Two examples of how liquidity and investment returns correlate are:

Thus, even though the process is fairly straightforward and simple and the amount is deposited in your account within a few hours or a day. Higher liquidity can affect your return on investment.

This is also why FDs are good to park funds for emergency expenses and unforeseen exigencies. Since you don’t know when you will need to withdraw, your money will enjoy higher growth if you don’t, but will always be available to you on short notice.

Liquid and illiquid investments are at the two opposite ends of the spectrum. Liquid investments are super easy to convert into cash (at short notice) whereas illiquid investments are super difficult to convert into cash (at short notice). The objectives and investment timelines for both types are completely different.

“If you try to convert illiquid assets into cash at short notice, you may have to trade off its value.”

For example, let’s say you own a property in a suburb and have hypothecated the same to a bank. During an organization restructuring, your income is under severe stress and you find it extremely difficult to pay your EMIs. You want to sell off your property and clear the bank loan. Finding a buyer quickly could be difficult. Even if you manage to find one, you will end up selling the property at below-market value to get the money.

So, the transaction ends in a distressed sale. To avoid such scenarios, it is best to set aside some money in liquid funds such as bank savings accounts and fixed deposits. The return on investment will not be as high as in real estate, but you will have money when you need it the most.

Investing in real estate, long-term bonds, and gold should be done with a long-term horizon in mind. One, these assets take time to generate the kind of returns expected from them. Two, selling too quickly is difficult and costly.

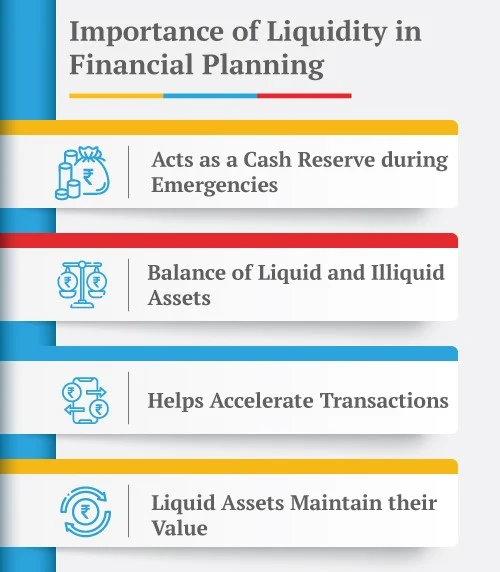

Liquidity has a very important role in financial planning so that you can strike a balance between your short-term, medium-term and long-term goals. Some reasons why liquidity is important in financial planning:

Cash reserves or emergency funds - keep six months equivalent of your income in fixed deposits. This is just a thumb rule and the exact amount can vary for different people depending on individual circumstances. This reserve should be touched only in case of exigencies and emergencies. For routine expenses, you can keep an appropriate amount in your savings account.

Your mid-term goals which are more than a year away but fall within the next five years need investments with lower liquidity. This means that you can invest your money for higher growth. For example, corporate debt funds, etc. Which will offer higher growth in this period, but only if you stay invested.

Long-term financial goals can use long-term investments. These investments like NPS, ULIPs, and PPF, may offer lower liquidity but can offer higher growth with time. These investments are perfect if you want to invest in goals like a child’s education, retirement, home purchase, etc.

When you have a proper financial plan in place, you will know how much money you would require at every important stage in life. Financial planning helps you plan your current and future cash flows such that you have enough every time you need it.

You will never run short of cash when you need it when you have planned and invested. Some typical scenarios:

Your car is 7 years old. You will have to replace it in another 8 years. You can use the following investment options to meet this goal:

Keeping money in ULIP, PPF or MFs will fetch better returns for the available time than letting it be in the savings account.

You may need money to pay your child’s University fees when they finishes high school. If s/he is currently 3 years old and may join University at 18, you can plan your investments for 15 years:

Ideally you should start saving for retirement the moment you start earning. But even if you are 45 you can start with additional investment:

You must invest up to 15% of your annual income until 60. Don’t bank on that fund for the next 15 years.

Be in control of your money. Invest in assets and financial instruments after thoroughly planning your financial requirements for the short-term, medium-term and long-term. Keep aside a kitty to help you tide over emergencies and temporary setbacks. Have a robust plan so that you don’t run short of money despite having assets.

An OTP has been sent to your mobile number

Sorry ! No records Found

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.