Written by : Knowledge Centre Team

2026-02-11

1001 Views

6 minutes read

Share

As your life progresses, you will find new responsibilities, new expenses, and financial matters falling on your way. The only way to maintain your efficiency in dealing with these many heads is to get more organised with your monthly financial dealings. Budgeting is the first, simplest, and most important step towards efficiently handling your money.

It can ensure that you always have adequate savings, health and life insurance, and adequate money to look after your monthly household needs. Let’s further understand the importance of budgeting with a handful of tips to ensure smart budgeting.

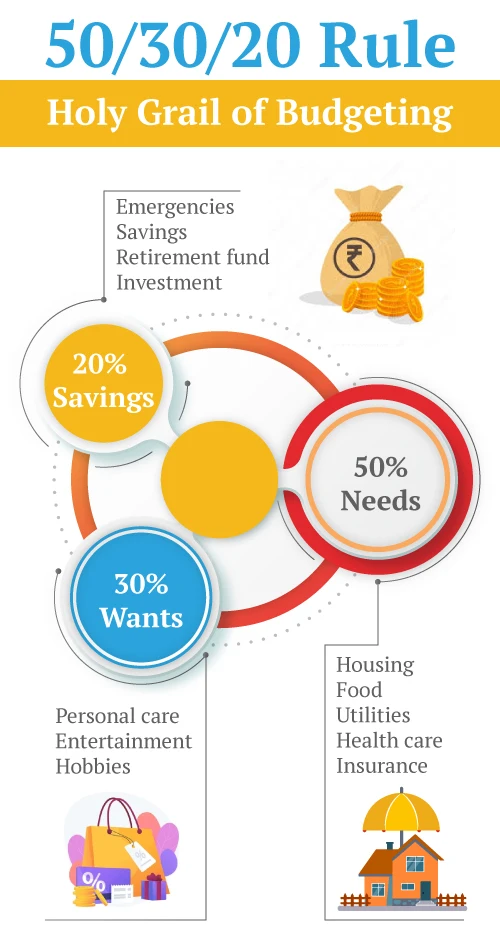

Key Takeaways

|

Maintaining a financial budget is essential because it gives you clear control over your income and expenses. It helps you track where your money goes, avoid unnecessary spending, and save for future goals. A good budget also prepares you for emergencies by encouraging the habit of setting aside funds regularly.

Budgeting keeps your finances aligned with your priorities. It reduces stress, improves decision-making, and helps you live within your means. With a well-planned budget, you gain confidence and stability, making your financial journey more predictable and secure.

An OTP has been sent to your mobile number

Sorry ! No records Found

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

With budgeting, you create a spending plan for the income you are generating. The process will ensure you have enough money for things you need and prioritise your limited resources accordingly. When you budget your expenses, you also learn to prioritise your expenses.

These five budgeting tips (steps) will help you maintain your monthly budget:

You have to make some long-term investments that will ensure you get regular income post-retirement. Canara HSBC Life Insurance offers you two different plans for a reliable lifetime income after retirement.

You can choose from either of these three plans for guaranteed income:

It is a deferred annuity plan you can use to invest your retirement corpus and receive regular income. The plan will ensure you receive guaranteed income post your retirement as per your needs:

The iSelect Guaranteed Future Plus policy by Canara HSBC Life Insurance offers a blend of protection and planned savings to support your life goals. It assures a guaranteed lump sum or income at maturity, depending on the option you choose, which makes it ideal for fulfilling milestones like your child’s education or retirement. The plan provides life cover throughout the policy term and offers flexible premium payment options.

Learn how to check if your retirement corpus will be enough?.

You can choose from multiple benefit options based on your financial needs. Its assurance of maturity benefits, coupled with family protection in case of unforeseen events, makes it a reliable and smart financial planning tool.

Creating and maintaining a monthly budget is not just about tracking your expenses. It is about building a secure future for yourself and your family. When you budget wisely, you make room for life’s priorities, whether it is health coverage, retirement planning, or funding your child’s dreams. Every rupee gets a purpose, and every goal has a path. With simple steps like allocating income, prioritising essentials, and investing smartly, you can create long-term wealth while handling short-term needs.

Plans like iSelect Guaranteed Future Plus by Canara HSBC Life Insurance help make your budgeting more effective by blending protection with savings. With tools like our online calculators at your side, your financial discipline today can become your peace of mind tomorrow.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.