Written by : Knowledge Centre Team

2025-08-22

3876 Views

6 minutes read

Share

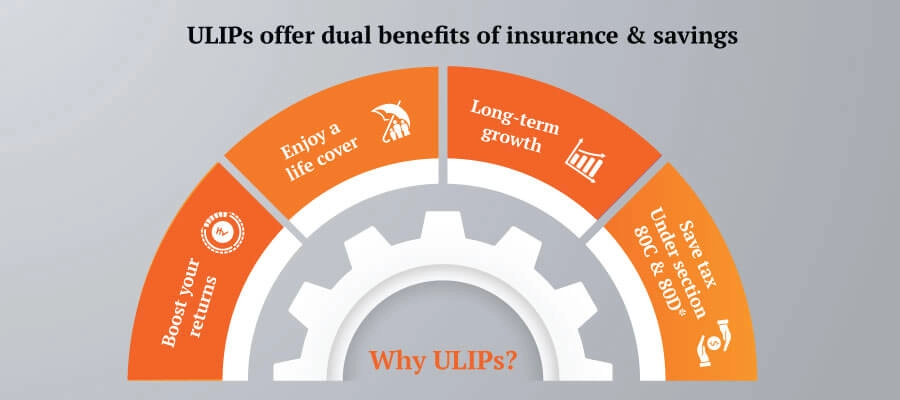

ULIPS (Unit Linked Insurance Plans) is a product offered by life insurance companies which provide a combination of investment and insurance. This makes the product a goal protector on two counts- both by investing for a life goal when you survive the policy period or when you are no longer alive, benefitting your nominee.

Previously, Unit linked insurance plans had been subject to much bad press because they are expensive. However, the dedicated push by the Indian insurance regulatory authority, IRDA has helped in lowering charges substantially. For making ULIPs competitive in the market, particularly in comparison to ELSS (Equity Linked Savings Scheme), many insurance companies have launched fourth-generation ULIPS’s which have no policy administration or policy allocation charges. The charge for fund management is the same as that for ELSS.

Because a ULIP plan has an investment component along with insurance coverage, part of the premium is used for life cover and expenses like fund management charges, while remaining is invested in debt, equity or hybrid (mix of both) based on the type of ULIP.

You can switch among funds in case you think that the fund has not been doing well. However, if you close your policy within 5 years, you will have to cough up Rs 6000 to the insurer as ULIPs come with a 5-year lock-in period.

After 5 years, you can withdraw funds partially or totally to foreclose your policy. But expert’s advice to stay invested for at least 10 to 15 years for earning attractive yields on your investment. Hence it is good to go for a ULIP if you have a long-term horizon to invest and are confident of paying premiums for the complete policy tenure.

Death benefit: The minimum death benefit guaranteed by a ULIP is called as the sum assured. The insurer will provide value to the fund if it grows bigger than the sum assured. Some policies provide fund value along with sum assured. But such policies charge more premium.

The standard charges and fees of ULIPS include:

With the clause of waiver of premium on the demise of the policyholder, he can ensure that the policy is used only for its long-term purpose. The future premiums are waived off and are paid by the insurer itself along with a lump sum payment at the time of death. Also, the total corpus built over the years is paid to the nominee when the policy period is over. This feature is valuable for persons who wish to keep their family financially secure in the event of their demise.

The rider for waiving of the premium is also applicable in the event of accident, critical illness or permanent disability. It ensures that all future premiums towards your ULIP policy will get waived and your life cover and investment will continue without hindrance.

These are all some of the reasons why it is attractive to invest in ULIP insurance.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

Canara HSBC Life Insurance offers online ULIP plans that blend life insurance protection with investment growth, helping you build wealth while securing your family's future.