Written by : Knowledge Centre Team

2026-01-10

1009 Views

6 minutes read

Share

There is no dearth of investment options in India. Investors have a variety of options ranging from term plans and unit-linked insurance plans to equity funds. Even though ULIPs are insurance products, most people consider it to be an investment product. However, many people do not take into account the impact of various charges and fees on the return from an investment product. Even a small charge over a long period can have a substantial impact on the overall returns.

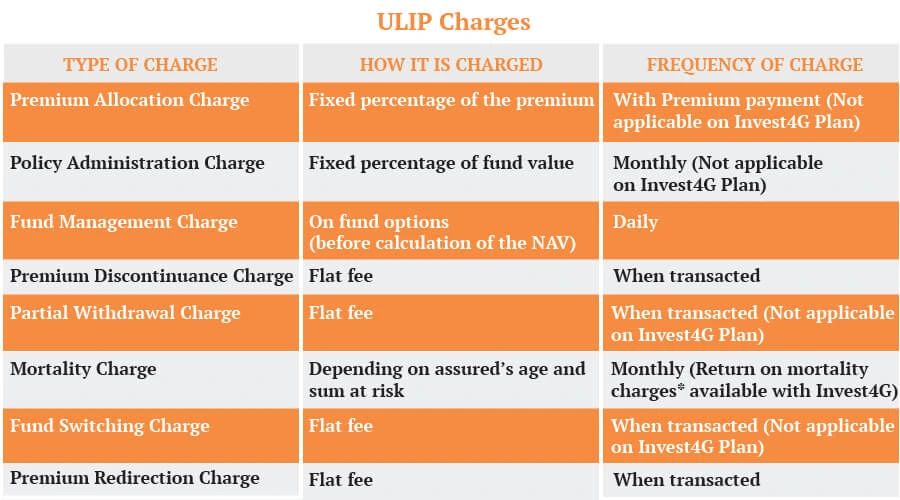

Here are 10 charges every person planning to invest in ULIPs should know about:

Even after multiple charges, ULIPs are one of the best insurance-cum-investment options in the market. Some of the charges are dependent on the action of the policyholder and may not be levied. To maintain transparency, the insurance regulator has capped the annualised charges of ULIPs at 2.25%. The Invest 4G unit-linked plan offered by Canara HSBC Life Insurance can help you fulfill your financial goals with ease and at a nominal price. With the ULIP plan, you can live a stress-free life without worrying about excessive fees and charges. Lower fees automatically boost the overall returns for the investors

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

Canara HSBC Life Insurance offers online ULIP plans that blend life insurance protection with investment growth, helping you build wealth while securing your family's future.