Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

A waiver of premium ensures you will still have life insurance coverage even if your earnings are reduced due to injury, disability, or critical illness. The rider is used mainly to cover life insurance costs in the event of critical illness or long-term disability. If you are affected, this rider will waive your insurance premiums for the duration of the rider period. Riders are offered at an additional cost, which is paid as part of the premium.

Key Takeaways

A Waiver of Premium Rider keeps your life insurance active during critical illness or disability.

It eliminates the need to pay premiums during the waiver period.

Not all policies offer this rider; it’s optional and comes at an extra cost.

Claiming the benefit requires documentation and may involve a waiting period.

Exclusions apply, so it’s crucial to read the terms thoroughly.

A waiver of premium rider is an insurance rider that allows you to stop making premium payments under certain circumstances, such as critical illness, injury, or disability. The insurer will continue to provide coverage, and the policy will not lapse.

How Does Waiver of Premium Benefit Work?

When you buy a life insurance policy, you are usually required to pay premiums regularly to keep the coverage in force. A waiver of premium benefits allows you to stop making premium payments under certain circumstances and still keep your coverage active. Some of the prominent features of a premium waiver are listed below:

Most waiver of premium benefits are triggered by a disability that prevents you from working.

The benefit is designed to help keep your life insurance coverage in force if you become disabled and cannot work to earn income to pay the premiums.

Waiver of premium benefits is not available on all life insurance policies, and the terms of the benefit can vary from insurer to insurer.

Some policies may have limitations on when the benefit can be used or how long it will last.

Some policies may define a waiting period that must pass before the waiver of premiums gets activated.

Secure Your Family’s Future with the Right Life Insurance Plan

Enter OTP

An OTP has been sent to your mobile number

Didn’t receive OTP?

Application Status

Name

Date of Birth

Plan Name

Status

Unclaimed Amount of the Policyholder as on

Name of the policy holder

Policy No.

Address of the Policyholder as per records

Unclaimed Amount

Sorry ! No records Found

. Please use this ID for all future communications regarding this concern.

Request Registered

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

Benefits of Waiver of Premium in Term Insurance

The waiver of the premium rider has several benefits.

Helps You Keep Your Life Insurance Policy Active: It ensures that the policyholder has life insurance coverage even if they can no longer work and are unable to pay premiums. If you are the sole breadwinner of your family, your family will be financially dependent on your life insurance policy proceeds in case of your unfortunate demise.

However, if you are unable to pay the premiums due to an accident or illness, your life insurance policy will lapse, and your family will not receive the death benefit. With a waiver of premium rider, your life insurance policy will remain active even if you are unable to pay the premiums. This will ensure that your family receives the death benefit in case of your untimely demise.

Gives you peace of mind: Knowing that your life insurance policy will remain active even if you are unable to pay the premiums due to an accident or illness gives you peace of mind. You can rest assured that your family will be taken care of financially in case of your untimely demise.

Save money on premiums: The waiver of premium rider can help you save money on premiums. If your income has been reduced due to illness, the money saved on premiums can be used to manage your expenses.

Exclusions in Waiver of Premium Rider

The most common exclusions under the waiver of premium rider are:

Disability resulting from participation in any hazardous occupation, except where the policyholder has the permission of the insurer and has paid an additional premium if required

Disability resulting from participation in any hazardous sports or activities

Did You Know?

The origins of modern insurance can be found in the London Fire of 1666. Due to the severity of the fires, insurance became essential rather than optional.

Source: Investopedia

How to Claim Waiver of Premium Benefit?

The policyholder must inform the insurer within the first 30 days of diagnosis of any critical illness or disability. The documents mentioned below should be submitted along with the application in the requisite format:

Original Policy Document

Completed Claim Form

Photo IDs such as Aadhaar or PAN Card

Proof of address, such as a Passport or an Aadhar

Hospital reports

Bank statement and cancelled cheque

In case of disability, a certificate from the local government body may be required

Once your claim is approved, your insurance company will start waiving your premium payments. You will continue to be covered under your policy and will not have to make any premium payments during the waiver period.

Who Should Opt for a Waiver of Premium Rider?

A Waiver of Premium Rider is especially beneficial for:

Sole Breadwinners: If your family depends solely on your income, this rider ensures uninterrupted coverage.

High-Risk Professionals: Those in physically demanding or hazardous jobs.

People with a Family History of Illness: Increased chances of critical illness make this a worthwhile addition.

Parents with Young Dependents: Ensures the financial plan remains intact despite unexpected health setbacks.

Policyholders Without Emergency Funds: Acts as a financial safeguard during crises.

Though it adds to your premium, the long-term protection it offers can far outweigh the cost.

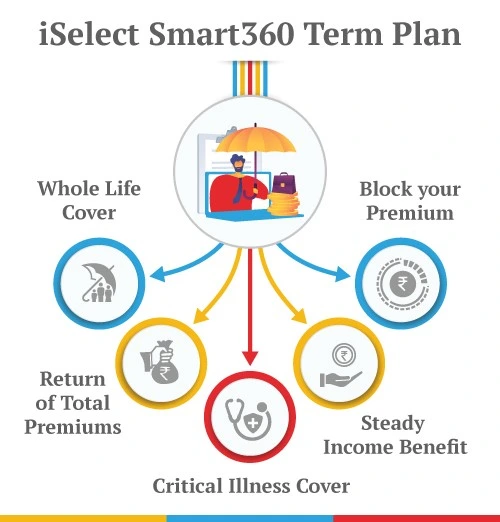

Waiver of Premium in iSelect Smart360 Term Plan

iSelect Smart360 Term Plan by Canara HSBC Life Insurance is a comprehensive term insurance solution that combines flexibility with robust protection. Apart from the versatile benefits and flexibility of premium and death benefit payments, the term plan offers premium waiver benefits for the following claims:

Critical Illness Claim

Accidental Total & Permanent Disability Claim

If you happen to suffer either of the two problems, your family will continue to have the safety umbrella while you recover, that too, without the need for extra premiums.

If you have a life insurance policy with a waiver of premium benefit rider, this means that your life insurance premiums will be waived if you become disabled or are affected by a critical illness and are unable to work. This rider can provide peace of mind in knowing that your life insurance coverage will not lapse if you are unable to work due to a disability.

Conclusion

A Waiver of Premium Rider adds an essential layer of financial protection to your life insurance policy. In times of critical illness or disability, it ensures that your policy remains active without the burden of paying premiums. While it may come at an additional cost, the security and peace of mind it offers, especially for families relying on your income, make it a smart investment. Be sure to understand the terms, exclusions, and claim process before opting for this rider.

If you have a life insurance policy with a waiver of premium benefit rider, this means that your life insurance premiums will be waived if you become disabled or get affected by a critical illness and are unable to work. This rider can provide peace of mind in knowing that your life insurance coverage will not lapse if you are unable to work due to a disability.

Glossary

Sum Insured: Sum insured is the maximum cap on the costs you are covered for in a year against any unfortunate event. It is applicable to non-life insurance policies like home and health insurance.

Sum Assured: Sum assured is the amount the life insurance company pays to the nominee if the insured event happens (death of insured). This term is used in life insurance policies.

Maturity Value: The amount of money paid out when a life insurance policy matures is known as its maturity value.

Risk Transfer: Risk transfer is a strategic method where a pure risk can be contractually shifted from one party to another as part of risk management and control.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.