Written by : Knowledge Centre Team

2025-12-21

1091 Views

8 minutes read

Share

In the current fast-paced and uncertain world, financial security is the top necessity. Health insurance gives you protection against the exorbitant expenses of medical treatment, and life insurance gives you protection against your family's aspirations and standard of living even in your absence. Why then do you need to purchase insurance, and which one do you need to purchase first? Through this blog, you will understand why you need to purchase life and health insurance and how you need to select the proper cover to protect yourself and your near and dear ones from the untimely incidents of life.

Key Takeaways

|

Insurance cannot restore good health. Insurance cannot bring a dead (wo)man back to life. But insurance may save a sick (wo)man from dying. Insurance can replace income. Insurance can ensure that the dreams of those living are fulfilled. In a nutshell, insurance covers the financial risk.

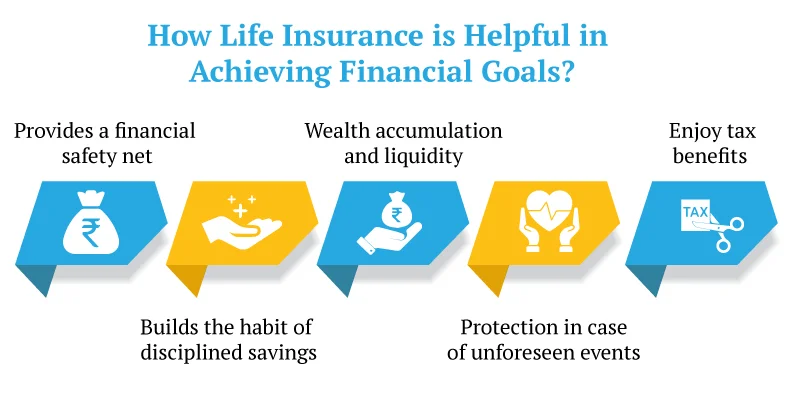

If the insured dies, their nominee/family receives a fixed “Sum Assured” that helps the family financially sustain for years to come. This amount can also help the children pursue education and become independent in life.

Private healthcare costs are already exorbitant and growing by leaps and bounds due to spiralling inflation which is more than average in the case of healthcare. Whereas even minor hospitalisation bills can badly hurt a common (wo)man’s pocket, critical illnesses are a double whammy.

On one hand, medical treatment costs can run into lakhs of rupees and on the other, income may cease to exist due to inability to work. Health insurance is the only known, financially viable solution that can offset the financial risks by bearing costs of hospitalisation as well as allied services.

Additional benefits even give away lump-sum amounts that can replace the lost income or be used to cover incidental costs (such as additional nursing at home, etc.) which may not be covered in a standard Mediclaim plan.

An OTP has been sent to your mobile number

Sorry ! No records Found

Thank You for submitting the response, will get back with you.

Both are definitely and equally important and there is no way to assign more weightage to either of the two. However, many a time, for salaried individuals, it may not be pragmatic to sign up for two important policies in one go. Prioritizing one over the other becomes imperative.

Common sense tells you that buying health insurance first is important because if health is taken care of, the probability of death due to illness will be significantly reduced. Go for a health insurance policy first. But do not procrastinate on life insurance for too long.

Listed below are some of the life and health plans that you must stay informed about:

Do you think life insurance ends with a term plan? Think again. There are several other covers that can help you build wealth, safeguard against health emergencies, and ensure a stable post-retirement life. Here’s what else you should explore.

Life is unpredictable, and although we cannot know what is going to happen next, we can prepare ourselves for it. Life and health insurance are both necessary to safeguard your finances and your family's future when something unexpected occurs. From covering medical expenses to providing financial assistance when you are no longer alive, the proper insurance policies enable you to live with peace of mind.

Canara HSBC Life Insurance offers different life and health insurance policies that are made to suit your requirements and expectations. Take the intelligent decision today to secure your future with a trusted insurance partner by your side.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.