Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

Work hard, but make your money work harder!

Ask any successful investor and they will most probably respond with this statement. Money does not grow on trees, but your hard-earned money can definitely grow multi-fold, even at night while you sleep soundly. Starting early gives you the advantage of time, which you can use prudently to create wealth. The power of compounding can create a huge savings kitty only if you start early. In Fixed Deposits, the interest earned is reinvested, which in turn creates a bigger principal. Hence, the power of compounding sets in. In the case of wealth creation instruments such as equities, staying invested for the long term will give you the benefit of multiple surges in the stock market.

If you have recently started working, you must have a savings plan and start investing immediately, because you can explore different saving plans before finding your right fit. Presuming your financial commitments are fewer at this stage, you can afford to allocate money to different asset classes and build a base that you can gradually grow over time.

Key Takeaways

Start saving and investing early to benefit from the power of compounding.

Always build an emergency fund covering 3-6 months of essential expenses.

Diversify your investments and avoid trying to time the market.

Review your financial plan regularly and adjust it as your goals evolve.

Five Savings and Investments Priority List

Saving and investing wisely are essential habits for anyone looking to build a secure future. As a beginner, understanding where to focus your money and how to prioritise your goals can set you on the right track from the start.

Here’s a simple guide to the five most important savings and investment priorities you should consider.

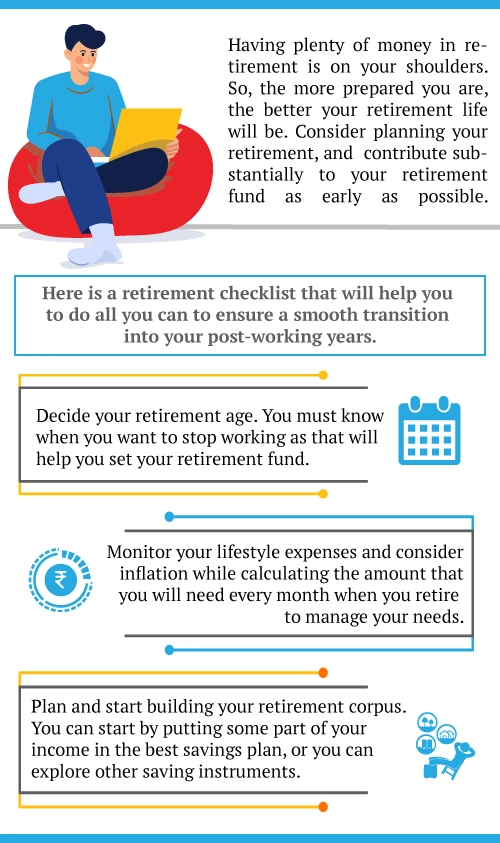

Retirement- It is never too early to start planning for retirement. With spiralling inflation, slowing wage growth and rising life expectancy, accurate planning is now a must. Retirement planning is a two-pronged strategy: wealth creation in the initial phase and wealth conservation later as you inch closer to retirement.

For example, ULIP Plans by Canara HSBC Life Insurance Company help you do exactly that. You can systematically invest a fixed amount of money each year in the form of premiums and enjoy fund growth as well as life cover.

When you are young, you can invest aggressively in equity-oriented funds that will give you extraordinary growth during bull-runs in the stock market. You have the flexibility to decide % allocation to funds of your choice.

The Auto Fund Rebalancing (AFR) maintains the defined proportion at pre-defined intervals. The Systematic Transfer Plan (STP) gives the flexibility of moving your money to different funds and can be used to park money in debt funds during bear markets and invest in equities when there is an anticipation of growth.

Build Guaranteed Savings for Your Future Goals

Enter OTP

An OTP has been sent to your mobile number

Didn’t receive OTP?

Application Status

Name

Date of Birth

Plan Name

Status

Unclaimed Amount of the Policyholder as on

Name of the policy holder

Policy No.

Address of the Policyholder as per records

Unclaimed Amount

Sorry ! No records Found

. Please use this ID for all future communications regarding this concern.

Request Registered

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

Life & Health Insurance- Healthcare costs are already high and are growing faster than the average rate of inflation. With newer diseases on the rise, the need for health insurance is greater than ever. Treatment for even minor ailments can cost lakhs of rupees in high-quality private hospitals. Affording treatment for critical illnesses has now become almost out of reach for the common wo(man).

Health insurance can help cover the costs of hospitalisation. Some policies even offer unconditional lump sum payments to cover incidental expenses caused by specified illnesses. This is important because when an income earner falls sick, they not only spend money on treatment but also lose income by staying away from work.

In an era where people live by the paycheque, what if the family’s breadwinner dies? A life insurance policy is the only reliable solution that financially safeguards the family in the event of an unfortunate demise of the policyholder. The lump sum Sum Assured is paid out to the nominee irrespective of when the insured dies during the term of the policy.

What’s more, in policies such as iSelect Smart360 Term Plan by Canara HSBC Life Insurance, there are additional riders to cover permanent total disability as well. In such cases, a specific amount is paid to the insured, and the policy continues as usual, but the insured will not pay the future premiums. The company does it. This plan also has a return of premium option where all paid premiums are returned to the policyholder if they survive the policy term.

Emergency Fund- Markets are volatile, incomes are uncertain, health is constantly challenged, and expenses and inflation are rising. A fund to manage contingency expenses is recommended so that there is no rude shock. Such a fund is possible only if you save and invest wisely. Ideally, your emergency fund should cover at least three to six months of your essential living expenses and be kept in a liquid, easily accessible account. This ensures that you can handle sudden medical costs, job loss or urgent repairs without disrupting your long-term investments.

Long Term Wealth Goal- You may need a guaranteed amount at the end of a specific period to fund your child’s education or build your dream house. You may want this in a stream of payouts over a couple of years, because university fees are paid each year and house construction costs are also borne in stages based on progress.

Short-term lifestyle goals tend to focus on immediate needs such as fitness, family holidays or a new car. If you start investing early on, your fund balances can witness significant growth that will make some lifestyle aspirations more affordable.

Short-Term Savings Goal- While planning for major long-term goals, it’s equally important to set aside funds for short-term needs like building a festival fund, upgrading gadgets, or paying for a short course. A dedicated short-term savings pot helps you meet these expenses without dipping into your emergency fund or long-term investments. Products such as recurring deposits or liquid funds can help you grow this money while keeping it accessible when needed.

Did You Know?

According to the guidelines of IRDAI, policies like term insurance and unit-linked plans are ineligible for loans.

Source: The Hindu

Mistakes to Avoid as a New Investor

Investing for the first time can feel exciting but also overwhelming. Many beginners rush in without understanding the basics, which often leads to costly mistakes. Here are some common pitfalls you should watch out for and simple ways to avoid them as you build your savings and investment plan.

Not Setting Clear Goals- Jumping into investments without a clear goal is like driving without a map. Always define what you are investing for, whether it is retirement, a house or your child’s education, and choose investment products that match your time frame and risk tolerance.

Ignoring an Emergency Fund- One of the biggest mistakes is investing all your money without keeping enough aside for emergencies. Without a safety net, you may be forced to break your investments at the wrong time. Make sure you build an emergency fund covering at least three to six months of living expenses first.

Putting All Eggs in One Basket- Many new investors put all their money in one stock or scheme, hoping for quick returns. Lack of diversification increases risk. Spread your investments across different asset classes, such as equities, debt instruments and deposits, to balance risk and returns.

Timing the Market- Trying to guess when to buy low and sell high can backfire badly. No one can perfectly time the market, not even experts. A more reliable approach is to invest regularly through Systematic Investment Plans (SIPs) or by setting aside a fixed amount every month.

Overlooking Costs & Charges- Beginners often ignore the impact of hidden charges, brokerage fees or high expense ratios. Always read the fine print and choose cost-effective products so that more of your money stays invested and grows over time.

Not Reviewing Investments- Investing is not a one-time activity. Many beginners forget to track and review their portfolio regularly. Revisit your investments at least once a year to check if they still align with your goals and rebalance if necessary.

Glossary

Endowment plan: A combination plan of life insurance and investment with a death benefit and an assured lump sum if you survive.

Surrender value: The accumulated amount the insurer pays to the policyholder upon termination of the plan mid-tenure before maturity.

Cash Value: The amount that builds up in a life insurance plan over time and is available to withdraw as a loan.

Credit Check: It is the inquiry and search of your credit history to check whether you can repay your debts.

Collateral: A valuable asset you agree to give to somebody if you cannot repay the borrowed money.

Conclusion

Starting your savings and investment journey early can make a world of difference to your financial future. By setting clear goals, building an emergency fund, protecting yourself with insurance and making informed investment choices, you can achieve both peace of mind and long-term financial security.

At Canara HSBC Life Insurance, we understand that every individual’s goals are unique. That is why we offer a range of solutions to help you protect your loved ones, grow your wealth and secure your dreams step by step. Begin today and give your future the head start it deserves.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

Savings and Investment Plans from Canara HSBC Life Insurance

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.