Written by : Knowledge Centre Team

2026-07-24

1289 Views

8 minutes read

Share

Investment planning is a crucial if you want to safeguard your financial prospects. Everyone has a desire to experience the life of his dreams. If we compare the financial knowledge in the past decades with the prevailing time, the stone has completely turned.

Nowadays, people are aware of the various saving and investment avenues like life insurance plans where their funds can form a healthy corpus for the times ahead. Everyone wants to put their hard-earned cash in a rewarding as well as a secure pool. Putting money in the best pool is of utmost importance because gaining money alone can't make one live a life of dreams. With a rise in inflation each year, it is necessary to consider this factor while analyzing the increase in revenue. If the addition in earnings each year exceeds inflation, your money is doing good.

Otherwise, the alarms have been raised to consider some serious financial planning.

To summarize, it is essential to increase your wealth at a rate exceeding inflation. Keeping your cash locked in banks alone would not make your wealth grow.

Money is a must requirement at any stage of life. One has to build a corpus to sustain well in life. Be it education and marriage of loved ones or buying luxury, or retirement funds, money is the driver in every walk of life.

While exploring different channels to build a corpus, people tend to look for a savings plan that would create a significant corpus at a greater rate. Due to multiple savings plans on offer, it becomes a tricky situation to consider one over another.

Saving plans are financial instruments that create resources for the times ahead and meet the financial goals by periodical contribution into various funds and saving schemes. Moreover, it also plays a remedial role by motivating investors to exercise disciplined investing.

There are respective advantages of opting for a savings plan for your financial holdings. Here are a few advantages of buying the best savings plan:

Putting the money in a clean portfolio and at the right moment makes your idle funds to multiply in the best way. A savings plan allows the investor to make money in the long run by offering well-organized and regular contributions. By earning adequate returns, one can be sure of securing the loved ones for unpredictable times ahead.

Savings with dual nature are beneficial for the family in the event of the ill-fated death of the supporter of the family. With the double plan, the family gets secured by receiving the insured amount and the fund value in a lump sum or annuity.

Putting the money in Government plans and the notified schemes provide the investor with a chance to increase his wealth but also gifts with certain tax benefits under section 80C and 10(10D) of the Income Tax Act, in the form of deductions from total income computed for tax.

Opting for plans with a long-term lock-in period helps investors reach their monetary goals. The lock-in feature of such investments plays a remedial measure in making the investor commit his funds in the investment for longer. Whether it is for buying a house, or the car you always wanted, or meeting the education costs of children, or for your post-retirement plans. Goal-centric planning is the best way one can hit an enormous corpus in the future.

The first action towards picking a plan is to undergo a risk-return evaluation of the scheme. If one has a high risk-taking capability, he may opt for a High-Risk savings plan. A low-Risk saving plan does well with investors having a lower risk appetite. Some of the best long term saving plan and schemes are:

Low-risk plans are popular amongst people who wish to play on a safer side in their journey to capital appreciation. Such schemes have a significant part of Government securities and plans as a base for investing. Following are the recommended options, which one must consider if low-risk investing is a priority

Public Provident Fund is still a choice for many investors, with goodies like tax-free interest upon maturity, lower risk, and a sovereign guarantee backed principal and interest, creating a safe avenue for the investors willing to pool their funds safely. Moreover, the interest rates are revised every three months by the Government of India.

Senior Citizen Savings Scheme is the most popular financial planning model amongst retirees aged 60 or above. The scheme has a manner that suits the needs of veterans. The savings scheme can be opted from any bank or post office and holds for five years, which may extend for a further period of 3 years subject to maturity.

Furthermore, the upper limit for investment is ₹15,00,000 in aggregate, which stipulates that one can open multiple accounts subject to the maximum limit. The rate of interest remains the same throughout the scheme and the interest earned attracts taxation that can be made exempt up to a maximum limit of ₹50,000, under Section 80TTB of Income Tax Act, 1961.

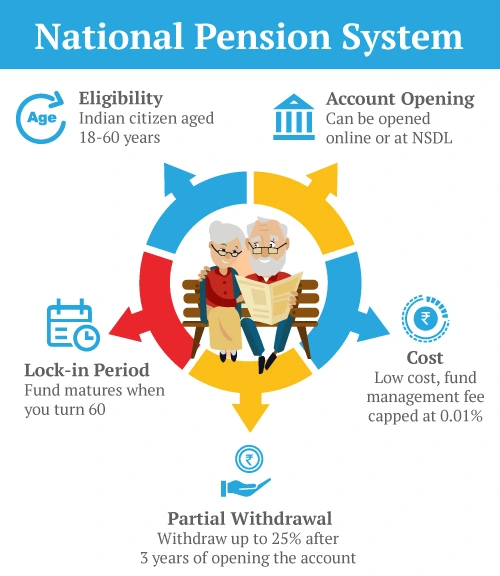

The Pension Fund Regulatory and Development Authority regulates the National Pension Scheme, which implies another safer alternative to park funds. The minimum yearly deposit for a tier-1 account is ₹1000 to render the account active. It is an aggregate of liquid funds, government securities, and fixed deposits.

The scheme is helpful to senior citizens aged 60 years and above as it secures a yearly return of 7.5%. The yojana provides income as a regular annuity as per the terms agreed upon by the investor.

The highest amount of pension reaped out of the scheme is ₹9,250, with the lowest ₹1,000 per month.

The scheme has a tenure of 10 years with a ceiling on investment limited to ₹15,00,000. The sum contribution is paid back to the Senior-Citizen at the point of maturity. In the event of sudden demise, the nominee to the scheme becomes the recipient of the amount.

Fixed deposits are the most popular and safest avenues to create a corpus for the future. The interest earned forms part of the ordinary slab, making taxation go easy for the lower-income group.

In an attempt to safeguard the depositors, the insurable amount has seen an increase to ₹5,00,000, for principal and interest with effect from the 4th Day of February 2020.

Gold has always been a saviour when it comes to financial security. Over time, investing in gold has turned into paper gold. Paper Gold or Gold Bonds are instruments that are made available through Gold Exchange Traded Funds. The buying and selling of gold take place in the stock market, keeping gold as a derivative.

High-Risk investments are an avenue for the risk-takers who aim for capital appreciation in the longer run. Let's get going with the popular plans prevailing in the market.

Debt Oriented Mutual funds are the choice when constant return over time is the priority. The risk involved with the Debt Oriented Fund is relatively lesser as compared to the Equity counterparts. It certainly has some risks, namely interest and credit rate risk, which makes the investor consider thorough research before investing.

The unit-linked insurance plan is an investment plan that is a blend of investment and insurance schemes, fetching the investor a unit of funds in which his money sits.

The returns are dependent upon the fund value of the funds as well as on the amount invested. Such returns are subject to the risks of the capital market.

Equity oriented Mutual Funds keeps the money, primarily in the equity stocks. As we all know the hazards associated with the capital market, the fund manager is of utmost importance for investors by managing the funds and safeguarding their interests. The returns are proportional to the proficiency of the fund manager with the funds.

It is crucial to have a timeline planned for winning future objects before opting in any scheme. It is more rewarding if we give it an early start as it provides the investor with a bit more time to create a premium on a corpus that is the icing on a cake.

An OTP has been sent to your mobile number

Sorry ! No records Found

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.