Written by : Knowledge Center Team

2025-11-11

2902 Views

14 minutes read

Share

Planning your finances means being ready for life’s uncertainties. While saving money is important, saving with a purpose makes all the difference. A life insurance cum savings plan gives you a smart way to do both. It gives you peace of mind and helps your money grow simultaneously. Whether you are planning for a child’s education or your own retirement, this plan keeps you on the right track.

Let’s understand why you must invest in a life insurance cum savings plan.

Key Takeaways

|

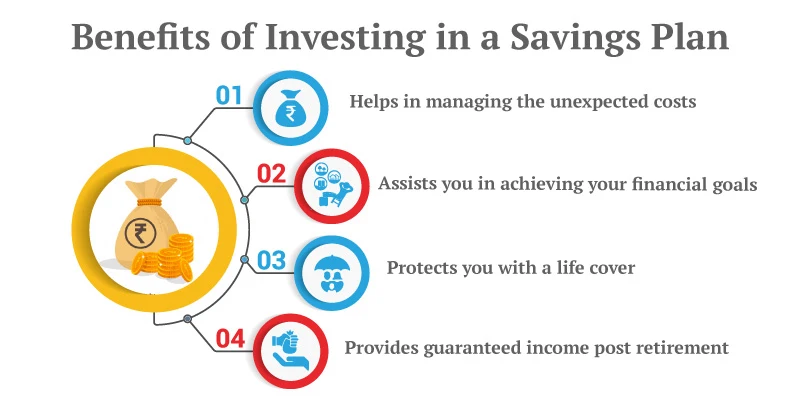

Investing in a savings plan is taking a step ahead in securing your family’s future. It improves your savings habit and also adds value to your saved amount. However, before buying a savings plan, you must know the features it provides to make a better decision.

Similar is the case with life insurance plans. Investing in one gives you an opportunity to stay covered and offer your loved ones financial security. Now, when you get a plan with a combination of features from both plans, it offers the best of both worlds.

Here are the top features of a savings cum insurance plan that you need to know before you look to buy the plan.

Guaranteed maturity benefits are an important feature of savings plans. That is you are assured to receive a certain amount at the policy maturity. Knowing that you will receive a guaranteed maturity benefit gives you a sense of financial security.

Since you know you will be getting a return, you can focus on just completing your part which is paying the premiums on time. The maturity benefit in the savings plan depends upon the following:

ULIP saving plans add bonus units to your portfolio, and the final value will depend on the fund's performance. While offering market investment benefits, they offer life insurance coverage as well.

Similarly, there are other types of life insurance plans that come with market-linked savings components.

Also Read - Best Saving Plan in India

A savings plan gives you full flexibility in terms of

An OTP has been sent to your mobile number

Sorry ! No records Found

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

Choosing a life insurance cum savings plan helps you grow your money while protecting your family’s future. Whether you are planning for education, retirement, or financial stability, this plan fits every stage of life.

At Canara HSBC Life Insurance, our plans come with strong claim settlement support, goal protection benefits, and flexible features that meet your changing needs. You can also use our online calculators to understand returns and plan better. Your journey to secure savings begins with a single step.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.