Written by : Knowledge Centre Team

2025-12-25

1030 Views

8 minutes read

Share

The simple “housewife” is actually the powerhouse of any family and her absence creates a vacuum that can rarely be filled by anyone else. Although the emotional scars can never be erased, a term insurance plan, for the housewife, now helps the family to at least ward off any possible financial challenges caused by the homemaker’s absence.

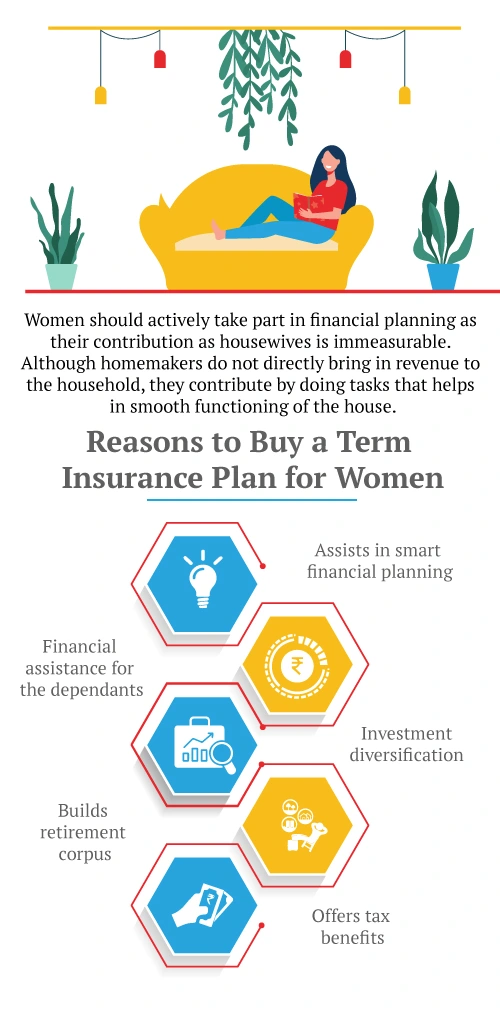

Although homemakers do not directly bring in revenue to the household, they contribute by doing tasks that are important for the smooth functioning of the house. Ergo, homemakers can be equated to the operations managers of the corporate world who run the kernel of the organization. In fact, more recently, there have been serious debates to assign an economic value to the work done by homemakers and add the same to the country’s Gross Domestic Product (GDP). Would you not pay a cook, a nanny or an estate manager to manage the household in the absence of the “housewife”?

The above points clearly advocate the necessity of providing term plans for housewives. But can a housewife buy a term insurance plan?

Traditional thinkers went by thinking of life insurance as a mechanism to provide financial protection to the dependants in case of the demise of the sole breadwinner of the family. In return for this financial protection, called “Sum Assured”, the insurance company would receive “Premiums” for the defined policy term.

The amount under “Sum Assured” depended on the age and annual income of the insured and was pegged at approximately 10-15 times the annual income. The underlying logic of this thumb rule was simple: If the income-earner dies, his income*15 times should be sufficient for the children to become financially independent or for the wife to find alternative sources of income.

Also, in the interim, the corpus of Sum Assured will earn interest thus adding to the kitty and giving more time to sustain life.

In the case of homemakers, there was no clear human life value because they did not “earn” a specific income. Their death did not cause any loss of income. This logic kept housewives outside the purview of term life insurance.

Although, you could still buy life insurance policies in the name of your homemaker spouse.

One of the conditions that you will face often while insuring your homemaker spouse is that you need to have term insurance from the same insurer. Other term policies, like iSelect Smart360 Term Plan from Canara HSBC Life Insurance, allow you to include your spouse in the same plan.

Here are the salient features of the iSelect Smart360 Term Plan, and how joint life cover helps:

The disability benefits help cover incidental expenses incurred that may not be covered by the regular Mediclaim policies whereas the Accidental Death rider gives an add-on Sum Assured to provide more financial cushion to the family. Child Care Benefits help the child pursue their aspirations even after the untimely demise of the parents.

Modern schools of thought have redefined the way new-age insurers look at the contributions of homemakers. As mentioned at the beginning of this article, would you not pay a cook, a nanny or house help to manage the household in the absence of the “housewife”? This is exactly the annual expense that you would incur in case of the untimely and unfortunate demise of the backbone of the family.

| Expense Type | Amount |

|---|---|

| Cook* | Rs. 15,000 |

| Nanny* | Rs. 14,000 |

| Driver** | Rs. 20,000 |

| House help*** | Rs. 15,000 |

The table gives an estimate of your spouse’s economic contribution to the household although the actual contribution is priceless because no-cook or nanny can ever replace the emotional strength that a homemaker provides to the family. However, this quantification is necessary for calculating the Human Life Value (HLV) which forms the basis of extending term insurance covers to the homemakers.

The total monthly expense will range from Rs 30,000 to Rs 60,000 depending on the services and this works out to an annual expense of Rs 3.6 lakhs to Rs 7.2 lakhs. If your spouse is about 35 years of age, you must extrapolate the annual expense, using the same thumb rule that was used for income earners, factoring in the inflation as well. Some components of the expenses, such as Nanny, Driver may not exist in future though.

Even with a modest Rs 3.6 lakh expense per year, the thumb rule of 10 times when applied, the projected corpus works out to Rs 36 Lakhs. This is the minimum insurance cover that the housewife should have basis the financial calculations. The exact amount will vary basis age and other personal circumstances of the family.

The term “housewife” has now evolved to be called “homemaker” to make it more gender-inclusive as more and people of the other genders also opt to stay at home to manage the household chores and run errands for the family when needed. Of course, this trend is very recent and the sheer magnitude of stay-at-home women is still staggeringly high. Adding them under the umbrella of term insurance will surely add to the family’s financial stability.

An OTP has been sent to your mobile number

Sorry ! No records Found

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

Canara HSBC Life Insurance offers online term insurance plans to secure your family financially in your absence.