Written by : Knowledge Centre Team

2026-06-22

4955 Views

6 minutes read

Share

Wealth creation is something humans yearn for from a very early age. Even before taking up a career or discerning their passion in life, most people are confident about making enormous amounts of money.

There is no easy road to wealth creation. It takes a lot of smart work and a lot of your most precious possession – and no, not money. It’s time. Time is one of the most treasured things in the world.

Key Takeaways

|

Setting clear income goals can help you feel more confident and satisfied with your money, something that's not always easy to achieve with other assets. Equity goals are also useful because they can support your other financial plans more effectively. Many successful businesspeople have reached financial success by setting wealth goals before fully entering the business world

However, like much good stuff, capital objectives are not easy to achieve. But with the proper strategy to save and invest, even ordinary people like us can achieve incredible feats.

Wealth creation is the process of increasing assets and reducing debts over time. It is eventually the process of establishing and building a reliable source of sustenance so that you would not have to strive to make ends meet.

A person’s wise and rational financial judgments determine the value of the wealth they can generate.

Two important points to ponder are:-

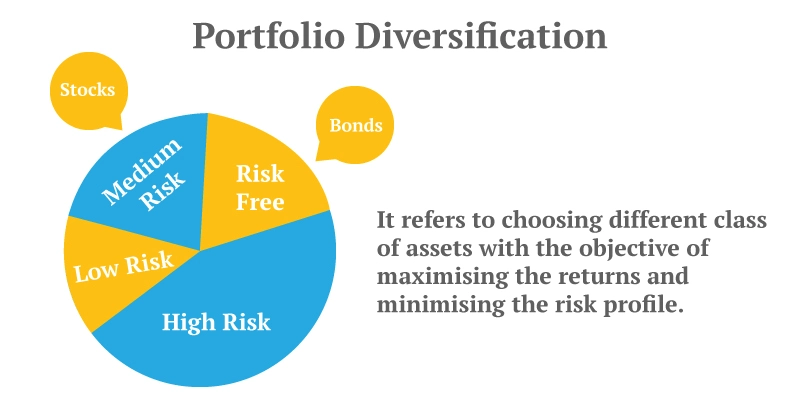

Wealth creation encompasses various aspects, including assets, property, retirement plans, inherited property, gold, and valuable metals. Putting your money in these instruments enables you to grow your economic worth over the years. The appreciation in the value of assets or the returns made from capitalising in stocks, bonds, mutual funds, etc., are all means to earn revenue.

An OTP has been sent to your mobile number

Sorry ! No records Found

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

Here are some tried and tested ways to build your wealth efficiently

Before you invest, you must know that an investment that is best for someone may not be a promising option for you because your financial objectives, investment horizon and risk appetite are not identical. It is advisable to discuss with a trusted financial planner or advisor before making any decision.

A professional planner can look at your risk appetite and objectives to formulate the best wealth creation scheme to suit your requirements and goals. Investing is a long-term policy for creating wealth. The most prosperous investors invest timely, then allow their money to ripen for years or decades before utilising it as revenue.

Pursuing these easy tips can be incredible for your net worth in the long run.

Wealth creation is all about discovering the right equilibrium between traditional insurance plans and taking planned investment risks. The notion is to be consistent and careful and to put together the perfect wealth creation strategies.

Including life insurance in your wealth creation strategy ensures your family’s financial goals stay on track, even in your absence. It offers not just peace of mind, but a foundation on which long-term prosperity can thrive. After all, true wealth isn’t just about how much you earn, it's also about how well you protect what you build.

At Canara HSBC Life Insurance, we understand that wealth creation is not just about growing your money; it’s about protecting it, preserving it, and planning for the future with confidence. With the various term plans offered by Canara HSBC Life Insurance, you can take every step toward your goals with peace of mind and purpose.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

Canara HSBC Life Insurance offers online ULIP plans that blend life insurance protection with investment growth, helping you build wealth while securing your family's future.