Written by : Knowledge Centre Team

2026-01-10

1267 Views

7 minutes read

Share

Unit Linked Insurance Plans (ULIPs) are among the most preferred plans because of its dual benefits: not only do they provide favourable market-linked returns, but also provide financial security to your family by providing life insurance. To put it simply, ULIP is both an investment and a life insurance plan. But did you know that ULIPs can also help you secure the future of your child? A ULIP based child plan can help you to provide for the cost of your child’s education, and in the case of any unfortunate eventuality your child will receive either a lump sum or regular payments, as per the terms of the policy. What’s more, some ULIP based child plans also come with the option of waiver of premium, in the case of a policyholder's sudden demise. This means that children can receive regular payments to fund their education.

Also Read - What is ULIP Plan?

ULIP can help you meet the cost of your child’s education: Every parent wants their child to receive the best education, be it at national educational institutions of repute, or prestigious foreign universities. But, funding for these reputed educational institutes cannot be just met by savings. You require a huge corpus of funds to meet the cost of education. For instance, if you want your child to go to the USA for higher education, you have to factor in a wide slew of costs. Apart from the tuition fees and cost of living expenses, you have to consider the education inflation and foreign exchange rate movement. Come to think of it, the costs might seem demotivating. But if you start an early investment in a Child based ULIP, it will help you to have sufficient funds for your child’s education.

ULIP can help you meet the child’s immediate and future financial requirements: A ULIP will also act as a life insurance plan, thereby ensuring that in the case of any unfortunate eventuality, your child’s financial requirements are met. If your child is in the midst of an educational course, there will be no shortage of funds. Even the child’s life stage goals, like marriage can be funded by the death/ disability benefit - in the form of sum assured - provided by the ULIP. Some ULIPs also provide for waiver of premium, in the case of your unfortunate demise/disability. This means that the policy continues with all benefits, and all future premiums are funded by the insurance company. In this case, the fund value will be paid on maturity.

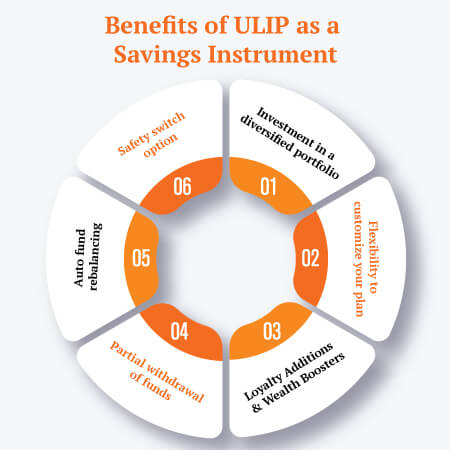

Now you can start planning long-term for the future of your child by investing in a ULIP. This investment plan is equipped with the following features and benefits:

Thus, you can invest in a ULIP to secure your child's financial future. You must always select the best ULIP to get maximum benefits. You can zero in on the Canara HSBC Life Insurance plan, a protection and savings oriented ULIP. Along with favourable returns on your investment and life insurance, this plan allows you to save for your dreams and life goals. The loyalty additions and wealth boosters in this plan further multiply your savings.

An OTP has been sent to your mobile number

Sorry ! No records Found

Thank You for submitting the response, will get back with you.

Thank You for submitting the response, will get back with you.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

Canara HSBC Life Insurance offers online ULIP plans that blend life insurance protection with investment growth, helping you build wealth while securing your family's future.