Written by : Knowledge Centre Team

2026-02-11

2192 Views

7 minutes read

Share

The importance of saving and investing money is well known. Everyone knows investing is one of the cornerstones of responsible financial practices. Investing money helps grow your wealth instead of letting it sit stagnant in a bank account, earning minimal interest. It is essential for building long-term financial security and staying ahead of any curveballs life may throw your way.

Another key aspect of responsible financial practices is buying insurance to protect yourself and your loved ones against financial emergencies and unforeseen expenses. Insurance has the potential to help you and your family.

Key Takeaways

|

There is a way to provide a safety net to your family while also generating wealth through investing. It's called ULIP or Unit Linked Insurance Plan. A ULIP is a combined insurance plan where a part of the monthly premium paid by the insurance policyholder goes towards the payment for the insurance, and the rest is directed into investment funds chosen by the insurer.

These plans offer flexibility, allowing you to choose from different fund options based on your financial goals and comfort with risk. You can also make changes to your investment choices during the policy term, depending on how your needs evolve over time.

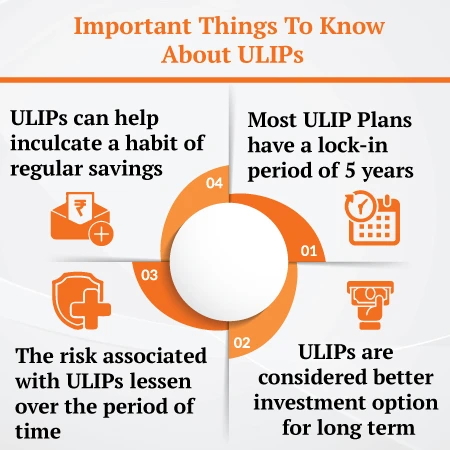

The idea of "short term" can vary from person to person. However, Most unit-linked insurance plans come with five-year lock-in periods. This means you cannot get the money back before completing five years.

Here are certain things you should know about ULIP to make a more informed decision:

Also Read - Short Term Investments

Keeping this in mind, if your definition of short term is five years, then sure, ULIP can help you achieve your short-term goals. It allows your money to grow gradually while keeping it protected for five years.

Also Read - Investment Options for 5 Years?

An OTP has been sent to your mobile number

Sorry ! No records Found

Thank You for submitting the response, will get back with you.

Thank You for submitting the response, will get back with you.

ULIPs are designed to support long-term financial planning. Unlike traditional insurance policies, ULIPs offer the added benefit of growing your savings over time through professionally managed investment funds. Here’s why it makes a great choice for long-term investment.

Choosing the right financial plan depends on your goals, time horizon, and how much flexibility you need. ULIPs are structured to offer both life insurance and long-term savings in a single plan, which can be useful if you're looking for a disciplined way to build wealth over time. However, they come with features that may or may not suit everyone.

Here are a few things to consider before deciding if a ULIP aligns with your needs:

Unit-linked insurance plans cut down the number of things you may have to juggle. Instead of having to keep an eye on and be mindful of a separate life insurance plan and an investment plan, this acts as a monthly investment added to your insurance premium.

If all of these seem like the right reasons to you, you should consider investing in term plans from Canara HSBC Life Insurance. Our unit linked insurance plans allow you to:

ULIPs can be a suitable option for those looking to combine long-term financial planning with life insurance. While they may not be ideal for short-term goals due to the five-year lock-in period and limited liquidity, they offer potential benefits for disciplined savers with a long-term outlook. With features like flexible fund options, tax benefits, and the ability to adjust investments over time, ULIPs can support structured wealth-building, provided you understand how they work and align them with your financial goals.

As with any financial decision, it's important to assess your needs, compare alternatives, and choose what fits your situation best.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

Canara HSBC Life Insurance offers online ULIP plans that blend life insurance protection with investment growth, helping you build wealth while securing your family's future.