Written by : Knowledge Center Team

2025-10-02

5130 Views

10 minutes read

Share

Unit linked insurance plans or ULIPs are amazing investment products from life insurance companies. These plans not only enable you to save tax every year but also provide you with highly customisable investment plans.

One such customisation feature is premium redirection, which allows you to control how your future premiums are invested. It’s a simple yet powerful tool that helps you adapt your investment strategy as your goals or market conditions evolve. Understanding how premium redirection works is key to making the most of your ULIP’s flexibility and long-term potential.

Key Takeaways

|

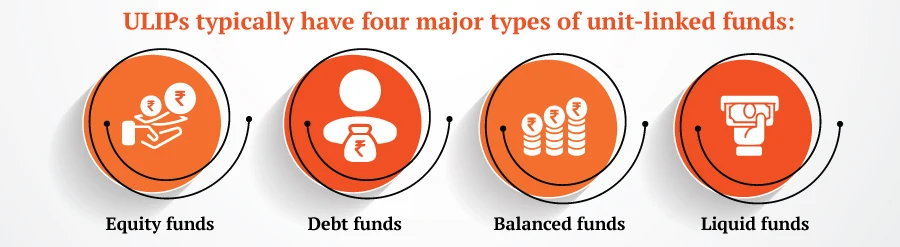

A ULIP plan has multiple ‘unit-linked funds’ where you can allocate your invested premium, each designed to match specific investment goals and risk appetites. You can choose to invest your money in the following fund strategies:

ULIPs are managed by professional fund managers and allow you to align your investments with your financial goals, whether it's aggressive growth, stable returns, or capital preservation. Understand the various types of unit-linked funds available to make the best decision to create a pathway towards a promising long-term value of your ULIP investment.

These funds are best when you want to preserve the value of your investment in the short run. For example, as you approach the goal or in the final years right before maturity.

Premium redirection is when you want to change how your upcoming premium should be allocated to different funds. This feature gives you the flexibility to realign your future investments without affecting the existing fund value already accumulated in your ULIP.

It’s especially useful when your financial goals, risk appetite, or market outlook change over time. For example, you chose to direct 100% of your investment premium to an equity fund in the ULIP plan. This approach might have suited your initial goal of aggressive capital growth.

After a few years, you want the premium to be split between an equity and a debt fund in a 50:50 ratio.This transaction is counted as a premium redirection in ULIP.

Premium redirection can impact your portfolio’s future allocation and risk profile. However, depending on the features you have been using, there could be different impacts.

In most ULIP plans, premium redirection applies only to future premiums. It doesn’t affect the money already invested, but it can change your portfolio’s direction going forward, especially if you've been following a specific allocation or investment strategy.

ULIP plans by Canara HSBC Life Insurance offer automated portfolio management strategies to help you maintain a disciplined investment approach without frequent manual intervention. These may include:

These strategies aim to optimise returns while managing risk. However, in most cases, if you opt for premium redirection, it will override and deactivate any automated portfolio strategy that is currently active

You are investing ₹1 lakh a year in a 15-year ULIP plan. You chose the auto fund rebalancing option to manage your portfolio at the time of starting the policy.

In the fifth policy year (after paying the fifth-year premium), you submit a request to redirect your future premiums in the fourth month.

The policy will implement your request upon the receipt of the next annual premium, i.e. the sixth premium on the policy. So, from the sixth premium payment, the auto fund rebalancing strategy, which rebalanced your portfolio every three months, will stop.

In case you had opted for a monthly premium payment, the change would be effective from the fifth month in the fifth policy year itself.

In the normal course of life, you may not need to redirect premiums, especially if you are using one of the portfolio management strategies. However, insurance is a long-term commitment, and situations may change over time.

The only legitimate scenarios when you may have to intervene and change your usual allocation are when you:

Whichever scenario applies to you, always remember the reason for starting this investment. If it were to meet a particular goal, that is what your primary focus should be. If it were to gather wealth, perhaps one or two interventions wouldn’t harm.

But do keep in mind that proven strategies work better in the long run than occasional interventions.

ULIPs give you the power to grow wealth, manage market risks, and stay tax-efficient, all within a single product. Whether you're aiming for long-term capital growth, planning for a life goal, or seeking stability as you near maturity, understanding the nuances of fund selection and premium redirection can put you in control of your financial journey. Automated strategies can bring discipline, while timely redirection can add flexibility, but both must serve the original purpose.

ULIPs reward those who stay invested and make informed adjustments. Stay focused on your goals, revisit your strategy when needed, and use the tools ULIPs offer, not reactively, but purposefully. That’s the key to making your ULIP work smarter for you.

An OTP has been sent to your mobile number

Sorry ! No records Found

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

Canara HSBC Life Insurance offers online ULIP plans that blend life insurance protection with investment growth, helping you build wealth while securing your family's future.