Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

As investment tools, ULIPs have come a long way in the past decade. They have become more and more popular as tax-saving tools. With the introduction of the LTCG in 2019, they came to the forefront. Budget 2025 has made ULIP investors wary about this popular tax-free investing option. The large tax benefit of section 10(10D) of the Income Tax Act, along with the chance to earn a better return through equity investment, has been the most convincing reason for investors to choose ULIPs. What is it that makes ULIPs work and what can you expect from them? Let’s find out.

What is a ULIP?

ULIPs are tax-saving tools which help you invest as well as secure your family, all with one single plan. A part of the premium paid regularly is invested in funds selected as per your risk appetite, and the other part is utilized for a life cover. This makes them neither pure insurance plans nor pure investments, but hybrid products.

Get a Personalised ULIP Plan for Wealth Creation & Protection

Enter OTP

An OTP has been sent to your mobile number

Didn’t receive OTP?

Application Status

Name

Date of Birth

Plan Name

Status

Unclaimed Amount of the Policyholder as on

Name of the policy holder

Policy No.

Address of the Policyholder as per records

Unclaimed Amount

Sorry ! No records Found

. Please use this ID for all future communications regarding this concern.

Request Registered

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

How Taxation of ULIPs has changed in 2026?

The ULIPs with annual premiums over ₹2.5 lakhs are taxable from February 1, 2021. They incur a 12.5% LTCG tax when redeemed after one year. Previously, the high premium ULIPs were taxed under Capital Gains, while lower premium ULIPs were taxed as income from other sources, if they were more than 10% of the death sum assured. The budget 2025 requires all non-exempt ULIPs to be taxed under Capital Gains, reducing the tax burden on minor policies.

Moreover, as per the budget 2025, the ULIPs with premiums less than Rupees 2.5 lakhs will incur a tax of 12.5% LTCG after a year. The LTCG exemption of up to Rupees 1.25 lakh annually will also apply, thus affecting individuals using ULIPs for tax savings.

What to Expect in 2026 from ULIPs?

As per the Budget 2025, the ULIP redemptions that are not exempted from tax are taxable under ‘Capital Gains’. The information brings clarity to the investors. It also equates the plan with equity-oriented mutual funds. Hence, 2025 will witness informed decision-making with respect to ULIPs as per the individual financial goals.

Why are ULIPs Good for a Slowdown?

We have all read about the global economic slowdown arising due to the pandemic. India will also be affected sooner or later. Markets will change and investors will be worried. At such a time, a ULIP can be a saving grace as it allows great flexibility in terms of switching between equity or debt oriented and balanced funds. You can easily bring your investments back on track if either of the categories isn’t performing well.

Further, the combination of insurance and market investment with ULIP makes them a considerable option. It offers protection from a volatile market while also building long-term wealth. The tax benefits and clarity, as mentioned above, also contribute to achieving financial goals.

ULIP maturity benefits are taxed at 10% as LTCG if the annual premium is above ₹2.5 lakh, but death proceeds remain tax-free.

Source: India Today

Why are ULIPs Gaining Popularity?

The reasons for growing popularity of ULIPs are as follows:

EEE tax status of ULIPs: EEE refers to Exempt-Exempt-Exempt. As per this principle, ULIPs are exempt on three fronts.

The first exemption is on the investment amount

The second exemption is on the interest earned from the investment.

The third exemption is on the maturity amount.

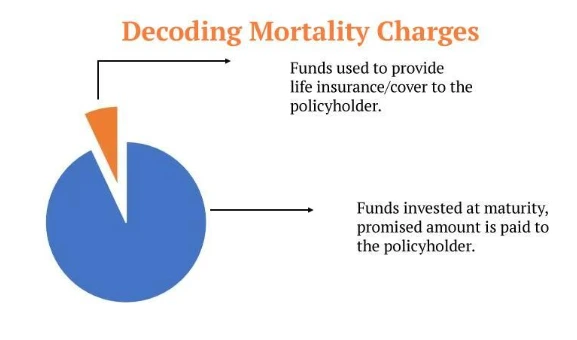

Return of mortality charges: Mortality charges are generally levied on insurance products, which is why they are applicable to ULIPs as well. It is the actual cost of insuring a life, and is deducted on a monthly basis. Mortality charges depend on the policyholder’s age, sum assured, gender, smoking habits, health factors, etc. It is usually less for healthier, younger persons.

Learn what are mortality charges in ULIPs?

Nowadays, some insurers have started offering return of mortality charges. This saves the cost of a ULIP investment significantly, and converts into better ULIP returns.

Investment Flexibility: ULIPs allow investment in equity or debt funds, or both. The decision is based on the investor’s requirements and financial goals. The flexibility to balance the funds and benefits makes it a well-optimised choice.

Switching Option: Adding to the flexibility is the freedom of portfolio management based on the market dynamics. It helps individuals safeguard their money as per their goals and risk appetite. Further, the switching is possible without the need to exit the plan, making it an easily accessible option.

Maturity and Death Benefits: Maturity benefits are the total fund attained within the policy term, which is provided to the policyholder. Death benefits allow the nominee to receive a higher of the sum assured and fund value as per the date of death.

Withdrawal and Top-Up Facility: Investors can opt to withdraw the funds as per their needs or add more funds. Both aspects are possible without the need for policy modification.

Premium Redirection: Premiums can be chosen to be submitted for funds different from the current ones, as per the policyholder’s wish and requirements. It adds to the flexibility of meeting one’s financial goals with the help of long-term investment with ULIP.

Glossary

Premium Funding: A benefit offered by insurance companies to continue premiums if the policyholder passes away

Lock-in Period: The minimum time before ULIP funds can be withdrawn

LTCG: Profit earned from selling an asset like stocks or property after holding it for a long period

Risk Appetite: The level of risk an investor is willing to take

Fund Switch: It is an option to move money between ULIP funds

iSelect Guaranteed Future Plus by Canara HSBC Life Insurance

If you’re looking for a plan that balances stability with smart long-term growth, the iSelect Guaranteed Future Plus by Canara HSBC Life Insurance is worth considering. It offers guaranteed benefits along with flexible options to customise your savings plan based on life goals. So, be it about building a corpus for retirement, your child’s education, or legacy planning, this plan can be your pick.

Key features include:

Return of mortality charges, adding back to your overall returns

Loyalty additions and wealth boosters to grow your corpus

Guaranteed benefits tailored to your chosen premium term and payment mode

Flexibility in choosing the policy term, premium payment frequency, and benefit payout mode

Conclusion

As we move through 2025, ULIPs continue to evolve as a smart and flexible investment option. They come with market-linked returns and also tax advantages.

The iSelect Guaranteed Future Plus by Canara HSBC Life Insurance is a strong contender for investors who want predictability, long-term savings, and life cover all bundled into one robust plan.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

Canara HSBC Life Insurance offers online ULIP plans that blend life insurance protection with investment growth, helping you build wealth while securing your family's future.