Written by : Knowledge Centre Team

2025-08-02

893 Views

8 minutes read

Share

Any investment journey must start with the basic premise of what one's goal is. Financial planning involves taking stock of one's risk profile, investment horizon, and financial goals. Your financial goals could include everything from buying your dream home to securing the best possible education for your children. After weighing these factors, the next step would be to consider which product to invest in. One such investment option is a Unit Linked Insurance Plan or ULIP.

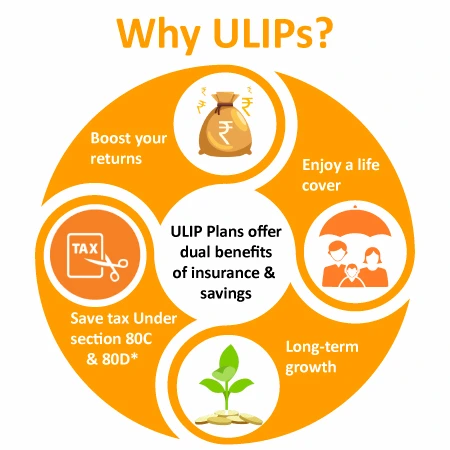

When you opt for a ULIP plan, you get the dual benefits of both insurance and investment, which is why it has turned out to be a feasible option for many investors. You get the benefits of investing in a mutual fund, while also getting insurance cover. When you invest in a ULIP, the insurance firm invests part of the money into shares or bonds, and the remaining is used to provide insurance cover. You can also make changes to your portfolio, switching between debt and equity. This flexibility is another advantage of investing in ULIPs.

ULIPs are a popular option among millennials who may have started thinking seriously about investments. They may be looking at specific goals like higher education for their children or a dream home. Millennials, who are part of the experience economy, value experiences like travel and would prefer to save up for a big international trip. ULIPs offer them that option because of the lock-in period, the sense of discipline and flexibility in terms of switching between funds for greater returns.

An Accident and Accident Disability Benefit (ADDB) rider offers an extra cover in the event of disability because of an accident. Some insurers offer it for a temporary disability as well. Some even offer waiver of premium as the policyholder might not have a proper income due to disability and paying premiums becomes difficult. If this benefit is not available, you can even go for a separate waiver of premium rider.

Like with mutual fund investments, any time is a good time to invest in a unit-linked insurance plan. ULIPs help tide over market volatility, so you can invest in them when the markets are down or when they are on the upswing. The earlier you start, the better it is, as you will be able to make use of the power of compounding. Compounding is all about reinvesting your income constantly so that your wealth grows. The longer the timeframe over which you invest, the better position you will be in to reap the benefits.

A ULIP plan should be used for long-term investment so ideally, you would need to start early and stay invested over the long-term. ULIPs have a lock-in period of five years, so they encourage focus and discipline in your investment journey.

A good time to invest in ULIPs is when you have a steady income and don't have too many commitments, and work towards your goals, whatever they may be. You can even alter your premium allocation annually, and don't have to stick to the same amount each year you are invested in. Based on your risk profile, you could choose from a variety of funds with varying exposures to equity. If you seek higher returns, you may need to choose a fund with higher exposure to equity. Also, if you are a salaried professional, and a mid-level executive at that, you can benefit from the tax-saving options for ULIP premiums and maturity amount under Section 80 C and Section 10D of the IT Act.

Investors planning for their retirement fund may also opt for a ULIP plan. One of the benefits includes sum assured or fund value, whichever is higher in the unfortunate event of the policy holder's death, thereby ensuring financial security for the family. As the goal is reaching completion, you could switch to a safer or low-risk investment in place of the equity-heavy option at the beginning or middle of the policy term.

You can consider Canara HSBC Life Insurance ULIP plan that offers the option of choosing from seven different funds and four portfolio strategies. Besides, it comes with benefits like partial withdrawal in case you need to meet some urgent financial commitments.

To conclude, whether you are a new investor in the early stages of your working life or you are planning a retirement fund apart from insurance cover, ULIP is a good option for you. There is no particularly ‘good’ time to start a ULIP. The time is now and the earlier you start the greater your chances are of fulfilling your financial goals. Just remember that any investment decision you make needs to be aligned with your risk profile and your expectations rather than market conditions. A ULIP helps you tide over weak market conditions as you can rebalance your asset allocation and can also fetch you considerable returns over the long-term.

An OTP has been sent to your mobile number

Sorry ! No records Found

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

Canara HSBC Life Insurance offers online ULIP plans that blend life insurance protection with investment growth, helping you build wealth while securing your family's future.