Written by : Knowledge Centre Team

2025-07-02

1107 Views

8 minutes read

Share

With time, the cost of medical treatment has increased rapidly in India. A change in the lifestyle of people living in the country has led to a rapid increase in the number of health insurance customers. Health insurance offers medical expenses to the policyholder in case of any health emergency. Coverage for different expenses depends on the policy.

As of now, in India, there are numerous health insurance companies and policies. So, it is hard to select the best health insurance policy for your loved ones. The below-mentioned tips and tricks can help you choose among the sea of options.

Buying a health insurance at a young age will provide you with the following benefits:

Find out the right time to buy a health insurance plan.

Try selecting a health plan that can cover a wide range of medical, post and pre-hospitalization cover, critical illness cover, cashless treatment, daily hospital cash benefits, maternity benefits, ambulance charges, etc. When you are buying health insurance for your family, make sure that the health insurance plan can meet the needs of each member of the family.

Write down all your requirements, compare them with various plans available and select the best policy that can meet your needs. Do not forget to check out the hidden factors like policy features, limitations, sub-limits, waiting period, daycare procedure coverage, organ donor expenses, newborn baby expenses, etc.

It is mandatory to go through every word of the policy. Hence, ensure that your family does not need to face any difficulty at the time of the claim.

Renewal is a prime factor to be considered while choosing a health insurance plan. With age, health problems and diseases also increase. Hence, health insurance is mandatory for any person at an older age. So, while selecting your health insurance plan, check for the policy that offers lifetime renewability. Selecting a lifetime renewable plan will reduce the hassle of buying another insurance plan once you cross the age limit.

For example, if you choose a policy that has an age limit of 50 years, you will have to buy another insurance after you cross 50 years. Hence, it is better to select a plan with lifetime renewability. This will keep you and your loved ones covered for a lifetime.

Take a look at the co-payment clause before selecting the health insurance plan. The co-payment clause is the percentage of the amount that has to be paid from your pocket.

For example, if your policy has a co-payment clause of 5%. For a claim of Rs. 1 lakh, you have to pay Rs. 10,000 from your pocket while the insurance will be paying the rest of the Rs. 90,000 as a part of the claim. There are also policies without a co-payment clause.

In general, health insurance plans will include pre-existing diseases, maternity expenses, and certain other treatments only after a specific period. This period varies from plan to plan. Hence, look at the time duration after which the pre-existing diseases will be covered in your policy. It is always recommended to select the policy that has the least waiting period.

Individual plans are usually for individuals that don't have a family. But if you have a family, it is better to take a family health insurance plan rather than taking an individual policy. Through a family health plan, you can have maximum benefits at an affordable price.

Check these 5 tips before buying a health insurance plan.

When purchasing a family health plan, it is advisable to choose one where you can easily include any new member of the family. In case any one of the family passes away, then the other family members can continue the same policy without any issues.

Preferring insurance that provides a wide network of hospital ranges is useful. Through this, you can have convenient and cashless settlements irrespective of your location.

The plan you choose will determine the room you will be given, whether it is a private, semi-private or shared room. If you are not able to choose a plan that has a high room rent limit, the rest of the room rent has to be paid from your pocket. Hence, it is recommended to select a plan that has a high room rent limit.

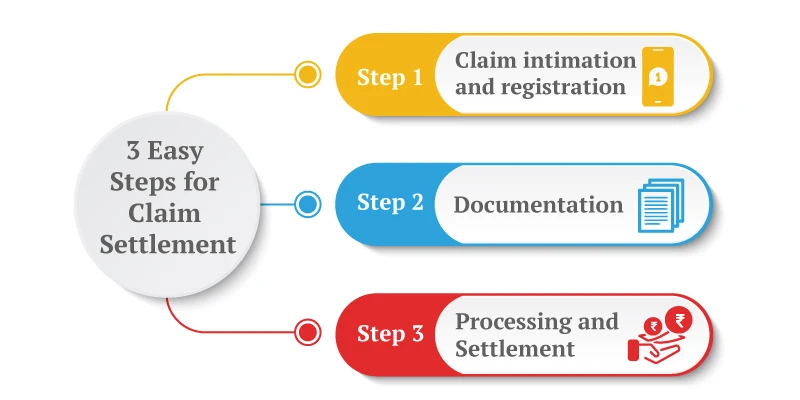

Select a company that has a high claim settlement ratio. The settlement ratio is the percentage of settled claims over the received claims by the health insurance company. Choosing a company that has a high claim settlement ratio will keep you in safe hands.

For example, if a health insurance company has a 90% claim settlement ratio, it means that the company has settled 90 claims of every 100 claims received. That is a prime factor to be considered while choosing a health insurance company for your family. Canara HSBC Life Insurance has a Claim Settlement Ratio of 99.43%^ for FY 2024-25. We have an easy and simple claim settlement process.

From factoring in the settlement ratio to looking at the number of network hospitals, you now know how to pick the right insurance plan. By understanding and utilizing the above mentioned ten tips, you can choose the best health insurance plan for your family and loved ones without any difficulty.

An OTP has been sent to your mobile number

Sorry! No records Found

Thank You for submitting the response, will get back with you.

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.