Written by : Knowledge Centre Team

2025-12-02

1096 Views

11 minutes read

Share

Life insurance plans act as financial support for your loved ones in your absence. By including it in your financial planning, you build a corpus and provide life cover to your family. Life insurance policies help save tax and act as a long-term investment.

Key Takeaways

|

Imagine this: you spend your life providing for a family. Your family is dependent on you for everything. Have you ever wondered what would happen to them once you are no longer there?

Life is unpredictable, and the pandemic has been a lesson. More and more people have started to invest in life insurance policies for their families, as human value has increased. However, those with existing life insurance policies have the edge over others.

Let us see why investing in a life insurance policy is a smart choice.

An OTP has been sent to your mobile number

Sorry ! No records Found

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

The COVID-19 pandemic has been a powerful wake-up call, highlighting just how unpredictable life can be. It has changed the way people view financial security, making it clear that preparing for the unexpected is no longer optional. One of the most important steps in this preparation is investing in a life insurance policy. In the face of such uncertainty, more and more individuals are now choosing to secure life insurance to protect their families’ financial future and ensure peace of mind during unforeseen events.

Here are 5 reasons why life insurance is important in 2026:

Smart Financial Planning : Life insurance policies are an integral part of smart financial planning. It allows you to achieve your long-term and short-term financial goals. A life insurance policy cushions you in case of emergencies, particularly post-retirement.

To claim the 80C deduction, the premium must not exceed.

Maturity proceeds or death benefits received from a life insurance policy are tax-free under Section 10(10D), provided:

There are three types of life insurance plans available in India, and each has its unique features. These are tailored to suit the unique needs of people and have different premiums.

Term life insurance: Term insurance is the most popular form of life insurance in India. Term life insurance has low premiums, which makes it a popular choice with middle-class families. However, term life insurance has a specific tenure, such as 10 years, 20 years, and 30 years.

Canara HSBC Life Insurance has a wide variety of life insurance plans that you can choose from as per your financial goals and requirements. Choose the best life insurance plan to provide a safe and secure financial future for your loved ones.

iSelect Smart360 Term Plan: This versatile plan can cover your spouse and has a limited premium payment option. Moreover, you get an increasing sum at an affordable price. Canara HSBC Life Insurance also gives you multiple payment options.

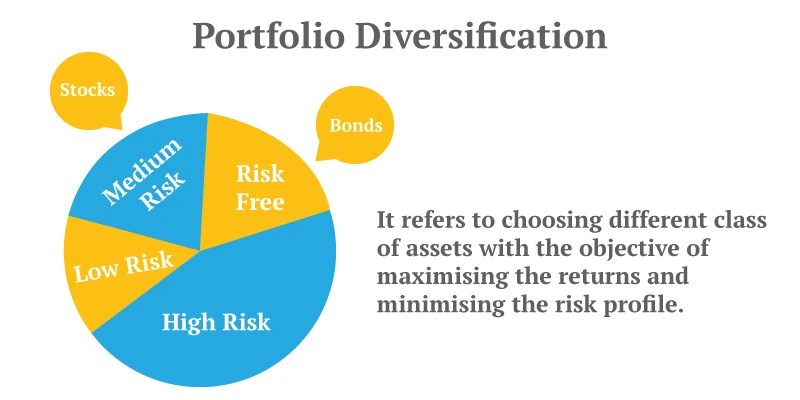

Life insurance is a necessity in today’s world of uncertainty. Whether it’s the rising cost of living, unforeseen health emergencies, or the growing importance of long-term financial planning, a life insurance policy acts as a powerful tool to safeguard your loved ones' future. As highlighted, it goes far beyond just a death benefit. It helps build a retirement corpus, reduces your tax burden, diversifies your investment portfolio, and provides essential financial support to your dependents.

With a variety of policy options available, such as term plans, ULIPs, endowment plans, and retirement solutions, you can choose the one that best aligns with your financial goals and risk appetite.

The earlier you start, the better positioned you are to enjoy lower premiums, greater returns, and enhanced financial stability. Secure your future, protect your dreams, and take the first step toward responsible financial planning, because your loved ones deserve nothing less.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.