Written by : Knowledge Centre Team

2026-01-08

1385 Views

7 minutes read

Share

Your financial life can be divided into three unique phases: accumulation, preservation, and distribution. The journey of your investments also follows the same pattern. While you are professionally employed, you rely on an external source of income. During this phase, you invest your savings to meet specific financial goals later in life.

One such goal is to build a substantial retirement corpus that enables you to maintain your life without needing to work. After you have achieved this goal, you can retire from active duty and spend your time at your convenience.

However, you still need to invest your money so that you can receive a regular income to cover your expenses. This can be achieved through life insurance and annuity plans.

Key Takeaways

|

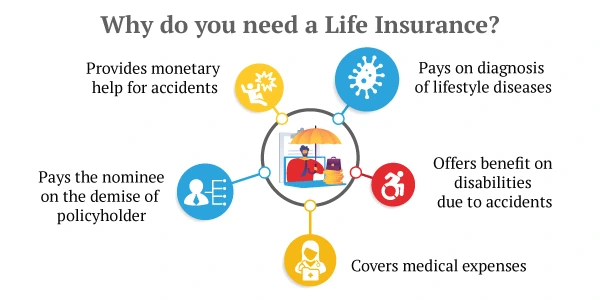

A life insurance policy is a legal financial instrument. The general picture you can have about life insurance is that you can secure your dependents’ future financially with a life insurance policy. The policy will provide a large lump sum of money to the dependents in the event of your early death.

You will need to pay a small amount annually to ensure coverage for your family. This amount is the premium of your life insurance policy.

However, life cover is not the only benefit of a life insurance plan. You can also invest your savings for a long-term goal into these plans. Life insurance is considered one of the safest long-term investments after government bonds and securities. Apart from this, it is also generally free from taxes.

Thus, life insurance plans not only offer coverage for your family in the event of your untimely death but also serve as a reliable way for you to preserve and grow your wealth over a long time.

If you're looking for comprehensive protection at affordable premiums, consider exploring term plans by Canara HSBC Life Insurance, designed to secure your family's future with flexible cover options.

An OTP has been sent to your mobile number

Sorry ! No records Found

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

Annuity refers to an arrangement (especially financial) that ensures a regular payment of a sum to you from an investment. Annuity plans are special instruments that enable you to turn your lump sum money into a regular income stream.

You can invest in these plans either in a lump sum or as a recurring deposit. However, regardless of your investment mode, annuity plans begin providing regular income after maturity out of the saved amount.

Annuities are generally looked upon as an investment to safeguard your regular income post-retirement. Their primary goal is to provide you with a long-term and steady income stream after you retire.

Though both life insurance and annuity have some similarities and are long-term investments, they are not the same. While you buy life insurance to provide a safety net for your family in case of your untimely demise, annuity plans make sure that you don’t outlive the investments you have made.

Here’s the difference between life insurance and annuity:

Annuities have two phases: investment and distribution. You can start an investment as soon as possible, ideally during your earning years, to allow your money to grow over time. During this phase, it’s advisable to explore options that offer higher growth potential based on your risk appetite.

In the distribution period, the focus shifts to preserving your accumulated corpus. Thus, you invest only in the safest options. At this stage, it is wise to choose safer investment avenues that provide regular income with minimal risk.

For example, if you have received a large lump sum amount from a provident fund, etc., you can invest in these plans. The correct age to start this phase of annuity is when you decide to give up your external source of income, i.e., your employment.

While both life insurance and annuity plans are long-term financial tools, they serve very different purposes. Life insurance provides security for your family in case of an untimely loss, whereas annuities offer steady income during your retirement years. Understanding how and when to use each can help you build a balanced financial plan that supports your goals through every stage of life.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.