Written by : Knowledge Centre Team

2026-01-10

1087 Views

7 minutes read

Share

Retirement is often seen as the time to relax, explore long-lost hobbies, and enjoy the freedom from daily routines. This phase goes beyond just saving a portion of your salary. It is about shaping a future where you can live with a mindset free from any financial constraints. Many people overlook the fact that retirement also comes with certain risks.

These may not be obvious today, but they can affect your lifestyle later. In this blog, we help you understand the four most common risks retirees face. More importantly, we share ways you can prepare for them and protect your golden years.

Key Takeaways

|

To live an ideal post-retirement life is what you work for. You just want to relax and travel the world. You could also start to pursue a hobby you left long ago. Most importantly, you should live a stress-free life post-retirement. But what is life without risks and uncertainty? You could encounter various risks post your retirement as well. There are certain risks that you can face post-retirement. These tend to threaten your financial soundness and hinder your retirement plan to live stress-free after retirement.

Here are the 4 most common risks you can face after you retire:

Underestimating longevity.

Risk of unexpected medical expenses, i.e., critical illness, accidents.

Systematic changes, urban development, etc.

Any other unexpected costs.

An OTP has been sent to your mobile number

Sorry ! No records Found

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

Many people believe their retirement funds will last because they have planned for the next 15 or 20 years. However, with growing medical advancements and better lifestyles, it is becoming more common to live well into the late 80s or even past 90. This means your retirement might span more than three decades. If your finances are not aligned with that possibility, you may run out of money when you need it the most.

If you or your spouse suffers from a serious disease requiring extensive medical care, such as cancer or heart problems, then it can be classified as a critical illness. These illnesses not only affect your health but also impact your finances. Treatment for such conditions often involves expensive hospital stays, surgeries, and long-term medications.

For retirees who may already have a fixed income, these sudden costs can quickly eat into savings meant for daily needs. To protect yourself, it is wise to consider a health insurance plan that includes critical illness coverage.

This kind of support can reduce the burden on your family and help you focus on recovery, without the fear of medical expenses draining your retirement fund.

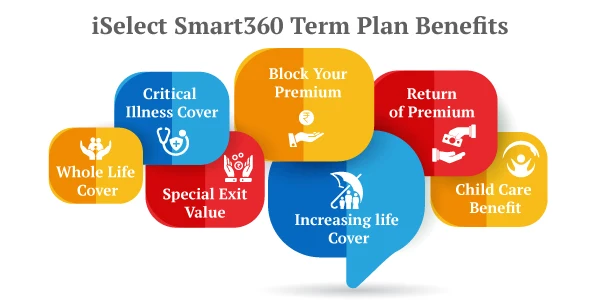

Many life insurance products, such as term insurance, provide you with an option to enhance your protection through riders. Riders improve the scope of your policy. You should buy a term plan that offers critical illness benefits.

iSelect Smart360 Term Plan by Canara HSBC Life Insurance offers the option to continue the cover till the age of 99. The plan carries critical cover as a default benefit. Thus, you can maintain the critical health cover throughout your life.

If this option is chosen, then you are entitled to receive a lump sum amount if you get diagnosed with a critical illness. This can help you go a long way in meeting the heavy expenses associated with the disease.

Systematic changes are the changes that affect the broader environment and are usually far beyond your control. These changes usually take place gradually, but a sudden occurrence is also likely at times.

Let us look at some of the common risks that can be caused by systematic changes:

Though these risks are out of your control, you can try to mitigate them or reduce their effect to some extent. Here’s how:

However secure you are, both physically and financially, after retirement, the truth is that you never really know what the future holds. Unforeseen events, such as a sudden accident, can bring large medical bills that may shake your financial stability in an instant.

For example, if an unfortunate accident results in severe injuries to your spouse, it can deeply impact the balance of your existing corpus. What you have saved over the years could start depleting faster than expected.

The costs of hospital stays, ongoing medication, medical equipment, and even hiring a full-time caretaker can easily catch you off guard. This is why it becomes essential to prepare in advance. Being financially ready for such unexpected situations is key to ensuring peace of mind and protecting your loved ones.

Insurance policies can help meet unexpected costs. But a healthcare plan will be useful till the age of 70. If this occurs when you are way past 70, you will have no option but to bear these expenses with your own money. These costs will not only take a toll on you mentally, but financially as well

This can be done by creating an emergency fund. Set aside a certain amount from your retirement corpus every month. This will act as your emergency fund. This will help you if you are in times of an unexpected house repair or an accident, etc.

Now you have an idea about how these risks can affect you post your retirement. Though you cannot change the future, the least you could do is to prepare for it. A well-thought-out life insurance policy and planning well in advance will go a long way to make sure that you fight these risks and lead a peaceful life after you retire.

You have planned to live for 80 years, but what if you surpass that age? Will your corpus be enough?

Here are a few suggestions that will answer these questions and help you live peacefully with a retirement plan:

Delaying a life insurance plan is not just about paying a higher life insurance premium in the future. It can also mean reduced coverage, fewer benefits, and leaving your family financially vulnerable. The smartest choice is to act when you are young and healthy, so you secure a low premium and strong protection for years to come.

With policies like iSelect Guaranteed Future Plus by Canara HSBC Life Insurance, you can lock in assured benefits and create a safety net that grows with you. Every year you wait costs more, so take the step today and protect your tomorrow without unnecessary expense.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.