Written by : Knowledge Centre Team

2026-02-14

1296 Views

7 minutes read

Share

Getting old means one has to get retirement from his job. Retirement is an important phase no one can ignore; many people have retirement dreams. So, it's important to start saving now if a person wants to fulfil his dreams and live happily ever after. The first step is how much a person should save to reach a retirement goal; many people get stuck at this question.

According to the thumb rule of savings, one needs to save 15% of one's pre-retirement income if taken to assume that a person has started saving at 25 to 67 years.

15% may seem a lot of your income, but if a person has a savings account with the employer, it counts as a person's annual savings. Is 15% enough? That solely depends on choices one makes before retiring and most importantly, when he starts saving. Any other source of income like pension should also be considered.

The earlier you start, the better it is. Early savings means a person's investment has time to grow through all the market's up and downs.

It may seem futile to save when young, and when retirement is far away, but when young a person has time to start saving, the investments also have time to grow and every penny saved equals every penny earned.

The thumb rule that is suggested requires a person to work till the age of 67 because that is the age after which people are eligible for social security benefits. But if a person wants to retire early, he needs to save more.

Learn more about saving and investment plans.

1% may seem very less, but after 30 years of retiring, he will see the benefits. For example, if he is 20 and increases 1% of his savings, his total savings are increased by 3%.

A fall and an increase in the market can affect the investment a person has. If he has invested too much, it can shift him towards risks, too less invested in stocks won't benefit him. So, one needs to be sure that he has a mix of investment. A regular check is needed on his investment to ensure he has the right amount of stocks, bonds, to meet his goals.

It is important to keep regular checks on investment if a person doesn't have time to opt for a managed account. If a person has a managed account then, professional managers do the job. A person can pick the level of risk he is willing to take.

Among the various priorities a person has like a house, children, parents, he should make retirement his priority. Be sure to save at least 15% of the income every year.

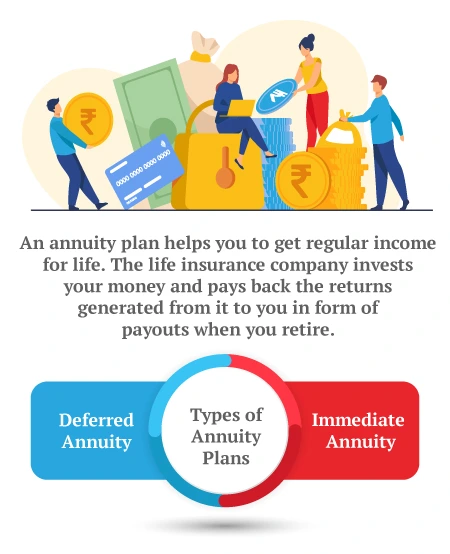

To take care of your post-retirement expenses, you can put your money into different saving plans and schemes. These plans come to provide a person with a normal salary after retirement. Considering the regular inflation investing in a retirement plan has become necessary. The best pension plan will support the old aged when all other income wells dry.

These life insurance plans ensure a better future after a person retires. A person can opt for any one of these monthly income plans for senior citizens to avail assured benefits. Prepare for the wellness of your golden years.

An OTP has been sent to your mobile number

Sorry ! No records Found

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.