Written by : Knowledge Centre Team

2026-02-10

1110 Views

7 minutes read

Share

Retirement is often viewed as the reward for years of hard work, and pension plans are designed to provide financial security during those golden years. A pension plan supports your life after retirement, providing a regular income and peace of mind. However, while many people think about how to build a retirement corpus, few consider an equally important question.

What happens to a pension plan if the policyholder passes away? The answer depends entirely on the type of plan and the choices made at the time of buying it. This becomes even more critical if you wish to ensure financial security for your spouse or children. Let’s understand this better further in the blog.

Key Takeaways

|

Reflect on how far you have come and the dreams you still hold dear. You wanted to work at a top IT firm by 22, bought your first vehicle at 25, and soon plan to marry the love of your life. You both hope to raise happy children, build a holiday home by the beach, and maybe even start a business together someday. Travel, family, and freedom sit high on your priority list. And at the end of it all, who wouldn’t want a peaceful retirement with no financial stress?

However, real life seldom follows a perfect script. There may be unexpected events along the way that demand financial resilience. From a carefree lifestyle at 22 to home loans and school fees later on, your needs grow with every phase. So does your income, and so do your goals. But have you stopped to think about your second innings? Have you ensured your dreams will remain safe even if life takes a turn?

Every life stage brings a shift in spending patterns. The money you spent on movies and food in your early twenties soon gets replaced by vacation planning, wedding costs, EMIs for your dream home, and school fees. While some of these are planned, others may catch you off guard. This is where the value of proper financial planning shines the most.

No matter how carefully you design your future, setbacks can occur. However, the strength of your plan lies in how well it absorbs shocks. A well-chosen pension plan is more than just a retirement tool. It becomes a dependable income source and, when chosen wisely, a financial legacy for your loved ones. Even after the policyholder’s untimely demise, the plan can continue to support those who matter the most. Therefore, understanding what happens to a pension plan after the policyholder’s demise is not just important. It is essential.

An OTP has been sent to your mobile number

Sorry ! No records Found

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

The policyholder continues to get annuities till the end of life, after which the purchased/invested amount will be given to the nominee. In case you have opted for a Joint Life Annuity, your spouse would continue receiving annuity even after you until his/her demise. The purchased/invested amount would then be handed over to the nominee.

Retirement is a phase that should be enjoyed, not endured. Early planning, regular investments, and appropriate choice of pension plans can help you live your second innings with dignity, fun, and excitement.

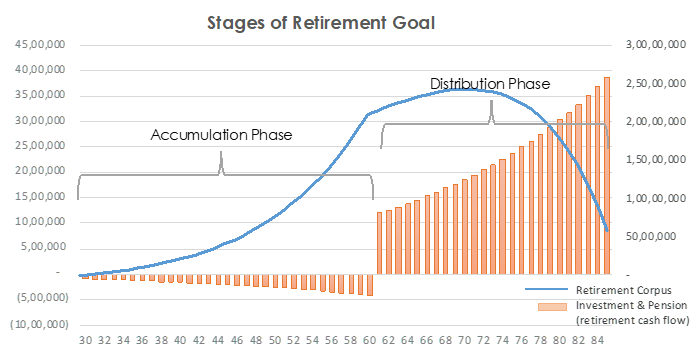

Building a corpus fund for your second innings cannot happen overnight. The earlier you start, the better it is. You will reap the full benefits of the Power of Compounding if you start well before you need it. Wealth creation requires patience, focus, and consistency over the long term.

A typical Wealth Management process moves in this order:

Figure: Wealth Creation > Wealth Preservation > Wealth Distribution

For example, the Promise4Growth Plus ULIP plan by Canara HSBC Life Insurance systematically switches funds to ensure steady returns. The safety switch gets activated so that your corpus growth remains safe from the market downtrends.

Learn how to check if your retirement corpus is enough.

The regular income stream that you receive post-retirement is called the Annuity. The Pension4Life plan by Canara HSBC Life Insurance offers both annuity options.

If you have recently retired and would like to invest a substantial corpus to earn regular income streams, the immediate annuity option is well-suited for you. If you have a few years left to pull down curtains on your full-time work, opt for a deferred annuity because you can invest over the years to build a corpus.

Understanding what happens to pension plans after the policyholder’s unfortunate passing is not just thoughtful but necessary for long-term financial security. The right pension plan helps ensure your family continues to receive support even when you are no longer around. Whether it is through a joint annuity or return of purchase price to your nominee, your plan can become a pillar of strength for your loved ones.

At Canara HSBC Life Insurance, we offer pension plans that combine lifetime income with legacy protection. This, in turn, allows you to retire with peace of mind. When your financial plan includes a dependable pension strategy, your second innings becomes more than just comfortable. It becomes secure, predictable, and aligned with your life goals, even during your absence.

Learn to protect your family with the right pension plan decisions.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.