Written by : Knowledge Center Team

2025-08-05

1916 Views

10 minutes read

Share

When 'retirement years' come to mind, we usually imagine a happy and secure life. You spent years working to accomplish your different financial goals and responsibilities. In the second inning of your life, you dream of living a comfortable life with your children, grandchildren and doing what you always wanted to do.

Financial worries should be the last thing that comes to your mind when you think of retirement years, especially if you have already invested in the best retirement plans.

Key Takeaways

|

The future life expectancy projections show that with every passing year, the life expectancy will increase. If you plan your retirement with 70 years of life expectancy, the number may be higher when you are near that age (it depends on your current age). An important question to ponder is, what if you outlive the years you have planned for? If you spend all your life saving, you will not like to work at that age. The solution to this problem is a life insurance annuity plan.

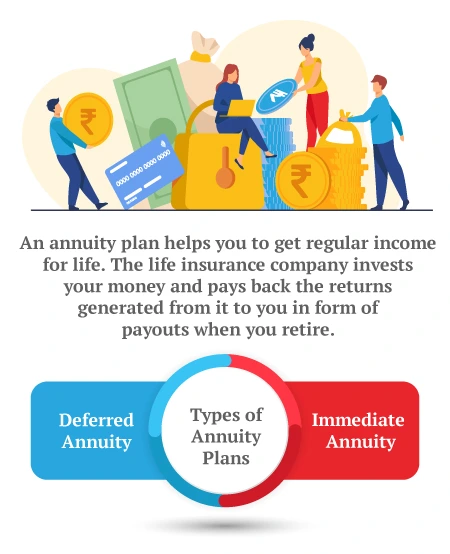

The annuity plan helps you get regular income for life (until your death) in return for a lump sum investment you make today. You can plan for your retirement in different ways, but to handle the above scenario, you may consider having an annuity plan. It will ensure you will always have a continuous source of regular income for life.

For example, the Pension4Life plan by Canara HSBC Life Insurance offers a guaranteed lifetime pension which will continue until your demise. You can also get a joint life policy, which will continue to provide a pension to your dependent spouse after your demise.

An OTP has been sent to your mobile number

Sorry ! No records Found

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

An annuity is a long-term investment plan that protects you from the risk of outliving your income. Below are three phases of the annuity plan:

The growth is not taxable. So, even if you choose the safety of capital over the growth opportunity, the investment growth will probably beat inflation by a small margin.

What happens to your payment after your death depends on the option you have chosen while buying the annuity plan.

When you decide to buy an annuity plan, you have several options to choose from. Each option is different with respect to how your annuity will work after you die. Let us look at the different options. Although you can have up to six different options for an annuity, there are two major classifications of annuities:

In this option, you receive the annuity throughout life, and when you die, all future annuity payouts cease to exist. In other words, the policy terminates.

You receive the annuity throughout life, and when you die, the purchase price (the price at which you bought the plan) is paid to your nominee. Immediate Life Annuity with Return of Balance Purchase Price.

The annuity continues till your natural demise. After your death, the balance is paid to your nominee. The balance is calculated by subtracting the price of the plan and the total of annuity instalments paid till your death. For example, if you bought the annuity plan by making a lump sum payment of ₹10 lakh and received ten payments of ₹25,000 each before your death. The nominee will receive a balance of ₹7.5 lakh as the death benefit. If the balance of the purchase price is negative, the nominee does not get any amount.

Upon your death or if any critical Illnesses are discovered or Accidental Total & Permanent Disability (ATPD) happens, the annuity payment will stop, and the purchase price will be paid to your nominee.

This is for a joint account, and the annuity continues till one of you is alive. If you die, your partner continues to receive the original annuity amount throughout her/his life. Upon the death of your partner, the purchase price is paid to your nominee.

In case of your death, the nominee will receive the higher of below:

The purchase price plus guaranteed bonus minus the annuity received till the date of your death.

105% of the purchase price.

Pension4Life by Canara HSBC Life Insurance is a great way to live a stress-free life post-retirement. It is not just beneficial for you but also your partner. You should consider an annuity plan while doing your financial planning for a better and secure future.

How close your dreams get to reality depends on your investment decisions now. One way to achieve it is through Pension or Annuity Plans like Pension4Life by Canara HSBC Life Insurance.

Annuity plans help you enjoy a worry-free life after retirement by giving you regular income. They protect you from outliving your savings and support your partner, too. Plans like Pension4Life by Canara HSBC Life Insurance give you lifetime income and financial security for your family. Choose an annuity plan while planning your retirement to stay stress-free and independent.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.