Written by : Knowledge Centre Team

2026-01-10

1097 Views

6 minutes read

Share

Inflation in India is measured using two standard indicators known as the Wholesale Price Index (WPI) and Consumer Price Index (CPI).

You buy a 500G packet of filter coffee powder for ₹400. In another 10 years, the same packet of coffee powder may cost ₹700. This implies the cost has grown by almost 6%. In simple terms, this % growth in the cost of products is called Inflation. The same ₹400 that can fetch you a 500G packet of coffee today will be sufficient to buy only 285G of coffee after 10 years.

In a nutshell, the buying power of your money goes down with time. To ensure your hard-earned money does not erode in value over time, the money must grow faster than the rate of inflation. The question is how inflation impacts your retirement plan. Let us delve deeper to understand.

Key Takeaways

|

An OTP has been sent to your mobile number

Sorry ! No records Found

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

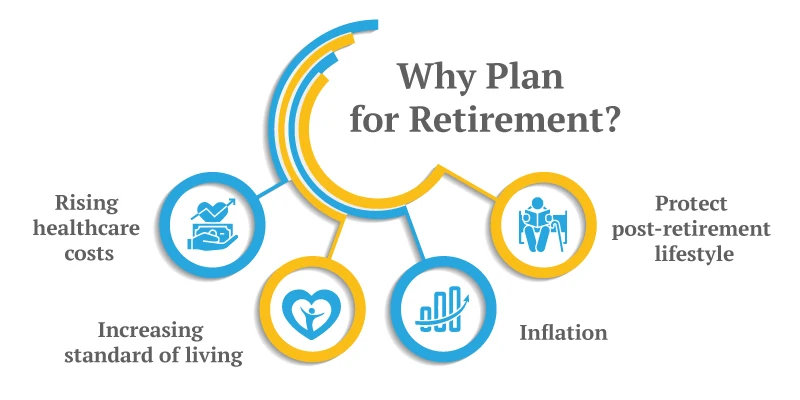

Considering only the average rate of inflation when planning for retirement can be misleading. You need to focus on the specific expenses that will remain relevant to you in later years. For instance, if healthcare costs rise by 10% annually, this can severely impact your finances during old age.

Your health insurance, if you have one, may not be sufficient, and your savings could be exhausted sooner than expected. Healthcare costs are also steadily increasing and are now above the average rate of inflation. As a result, healthcare accounts for a major portion of senior citizens’ living expenses.

This is why you must be mindful of these factors when you invest in funds and plan for your retirement corpus. If you invest in funds that give you an average of 7% returns when the cost of food is growing at 9%, it is evident that your savings will not help you lead the lifestyle that you are leading now.

Some insights into how inflation can impact your retirement plans are given below so that you can start planning early:

Keeping these factors in view, it would be wiser to invest in asset classes that will help you generate wealth, assure your family of reliable financial support in case of exigencies, and allow you to lead a stress-free retired life. Investment-linked insurance plans have proven to be comprehensive in providing an all-around financial backup because of their innate flexible design.

Canara HSBC Life Insurance offers various savings and investment plans that you can use to build your retirement corpus. The best thing about these savings plans is that they take inflation into consideration. Most of the plans are flexible and they allow you to increase the sum assured, keeping in account the growing needs of an individual.

Inflation can look like a slow-moving threat, but with time, it can significantly reduce the value of your money. Ignoring its impact can create a severe gap between your expected and actual financial needs. Hence, understanding and incorporating inflation into your retirement planning is not optional; it is necessary.

It’s never too soon to start your retirement planning. The sooner you begin investing in inflation-beating instruments, the more prepared you will be for a comfortable retirement.

Canara HSBC Life Insurance offers a range of retirement plans and annuity products tailored to meet the needs of every retirement stage. Explore your options and choose a trusted plan that works for your future goals!

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.