Written by : Knowledge Centre Team

2025-02-28

1795 Views

8 minutes read

Share

Any ownership that creates positive economic value and can be converted into money is called an asset. Any commodity that grows in value has generally termed an asset (the only exception being a personal transport vehicle that is considered a depreciating asset).

You invest some money in gold today at Rs. 5000 per gram and sell it off after 3 years for Rs. 7000 per gram. You make a net profit of Rs. 2000 per gram. Gold can be classified as an asset because you derive positive (profit of Rs. 2000) economic value and can convert this (by selling) value into money.

Similarly, a property such as a flat can give a dual returns-one in the form of rent and another in the form of surplus at the time of sale. If you purchase a flat for Rs. 30 lakhs and sell it for Rs. 55 lakhs, you clearly stand to gain Rs. 25 lakhs.

Amongst financial assets, you may choose to invest in Public Provident Funds (PPFs), Bank Term Deposits, or Life Insurance Policies, depending on your risk appetite.

Asset allocation is the dominant factor driving return on investment and any investment made should clearly align with your short and long-term financial goals. Some assets such as equities give superior returns over the long term but carry significant risk because the returns are subject to volatility in the market.

Click here to use - Investment Calculator

Assets that give lower but reasonably guaranteed returns are low in risk. Asset selection or allocation is a highly personalized decision and depends on your personal circumstances, aspirations and risk appetite. One size fits all approach does not work here. You must maximize future value depending on your individual tolerance level. Here are a couple of scenarios:

You may not like to take aggressive risks because you do not have the safety net to fall back on. If you think you have way too many commitments planned for the future, you may like to invest in safer instruments that do not involve too much exposure to equity markets. Guaranteed Savings Plans offered by Canara HSBC Life Insurance could be a good option to look at. These plans are good for guaranteed pay-outs at defined milestones besides giving better returns than standard bank deposits.

You are young and have minimal financial commitments at the moment. You want to focus on wealth creation that can help you build a large corpus for your future. You are also aggressively saving for retirement. Wealth creation requires adequate exposure to equities early on in your career. As you approach mid 50’s you can move into wealth preservation mode by putting your wealth in safer instruments.

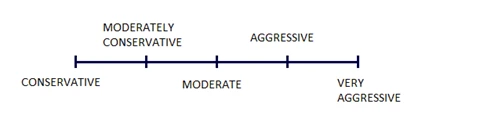

The above two are the extreme scenarios of risk appetite. There are a couple of other possible scenarios that lie between these two ends of the spectrum. Moderately conservative/moderate/aggressive are variants with different degrees of exposure to equity and debt. Try to assess what kind of risk appetite do you have. Basis your risk appetite, refer to the table below to allocate your funds between equity and debt.

| RISK APPETITE | ALLOCATION | ||

|---|---|---|---|

| EQUITY | DEBT | ||

| Conservative | 0-5% | 95-100% | |

| Moderately Conservative | 5-20% | 80-95% | |

| Moderate | 25-30% | 70-75% | |

| Aggressive | 30-40% | 60-70% | |

| Very Aggressive | 40-50% | 50-60% | |

While it makes sense to maintain an asset allocation you feel comfortable sticking to over a long period. However, you may question if you have enough time or expertise to manage such a portfolio. Here are a few savings and investment options that will do it all for you:

NPS is a popular retirement savings scheme for Indian citizens. Although NPS is famous for retirement savings, it also allows non-retirement investments which are more open-ended.

Both these accounts offer a custom portfolio investment under Active Choice and Auto Choice options. Active Choice lets you decide the asset allocation between equity, corporate debt, government bonds and alternative assets. The auto choice option will manage your portfolio under set allocations automatically as per your age.

Also Read - Best Saving Plan in India

ULIP plans also offer a mix of assets with different risk profiles for you to invest in. You can choose to manage your portfolio manually in ULIPs or choose one of the automatic strategies. The automated strategies can help you manage the risk in your portfolio for the long term.

Also, you have three unique advantages of investing in ULIPs:

Investments have to be done basis individual risk appetite and goals. Always keep in mind the extent to which you can take risks and allocate funds to appropriate financial instruments. If you want to maximise your returns from an investment you need to give it sufficient time.

This is only possible if, first, you can, and second, you feel confident in your choice. Both possibilities arise only if your overall portfolio is well within your risk appetite.

An OTP has been sent to your mobile number

Sorry ! No records Found

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.