Written by : knowledge Centre Team

2025-09-12

1089 Views

8 minutes read

Share

People have been investing in various financial instruments and finding several ways to build their wealth. One of the easiest ways to grow your money is to invest it in options which offer compounding returns.

Compounding interest is the interest where accrued interest on invested capital is regularly reinvested. Thus, after some time your previous interest also starts to earn interest, and this is what is called compounding. In other words, your capital continues to grow with time. So, the longer you stay invested the higher interest you can earn.

Here’s an example, you invest Rs 1000 with a compound interest of 5%. After a certain period, the money you earn will be 5% of Rs 1,000 which is Rs 50, and the balance of Rs 1050. Now instead of earning Rs 50 more the next time, you earn Rs 52.50. As you get some interest on previously earned Rs 50. Bigger investments create more profit in longer terms.

Compounding is when your previously earned interest starts to earn more interest. Basically, by stacking up the interests, you earn extra money. If you invest money in a compounding return option like Fixed Deposits, your capital will earn interest every quarter.

For example, if you make an FD of Rs 50,000 for 4 Years with a quarterly compounding interest rate of 5% p.a. Means the accrued interest will be reinvested four times a year. After three months you earn 1.25% of Rs 50,000 which is Rs 625.

| Duration | Invested Amount | Interest Accrued |

|---|---|---|

| 0 | 50,000 | 625 |

| Q1 | 50,625 | 632.81 |

| Q2 | 51,258 | 640.72 |

| Q3 | 51,899 | 648.73 |

| 648.73 | 52,547 |

After the first three months, you will earn an interest of Rs 625. For the next quarter, this 625 is ploughed back into your capital and the next interest is Rs 632.8.

If you invested only for a year, at the end of the year your total FD value will be Rs 52,547 instead of Rs 52,500 as it would be at a simple rate of return. If you stay invested for 5 years in this FD, your total value will be Rs 64,102. Compare this with Rs 62,500 you would earn at the simple rate of return of 5% p.a.

The gap between the simple rate of return and compounding return increases with time. In other words, the longer you stay in the compounding investment, the higher your rate of growth is. This phenomenon is known as the ‘power of compounding’.

You need to know more than just how compound interest works. You need to know the formula to calculate your earnings from your investment. The formula to calculate compound interest is –

FV = P(1+r/n)^(n*t)

In which,

P = Principal Amount

r = Annual Interest Rate

n = Number of times a year when interest rate compounds

t = Total amount of time

FV = Future value after ‘t’ amount of time

Finance is a great factor in our lives. Now and then we buy stuff and when we can’t afford it, we take loans. Loans are great ways to buy things when you don’t have enough money temporarily. However, this borrowed money shouldn't be taken lightly.

EMIs are compounding interest in reverse. When you don’t pay your EMIs on time, the interesting part of your EMIs also earns interest. Thus, causing a cascading effect and increasing your interest the more you delay the payment.

If you aren’t punctual about the payment of EMIs then you might end up repaying an extra amount than negotiated. So, make sure to pay your EMIs within the due date.

The majority of the long-term investments in India offer compounding returns. Few of the most prominent of these investments are as follows:

Mutual funds have been a popular investment choice due to their flexibility in accepting investments. You can start with small amounts, even an amount as small as Rs 500. You can invest in a mix of fixed-income securities and equity stocks through mutual funds.

The growth is compounded quarterly in most mutual funds with long-term investment objectives. Mutual funds like ELSS also allow tax deductions on invested money.

Mutual fund returns are linked to the market. Thus, you should invest in mutual funds as per your risk appetite.

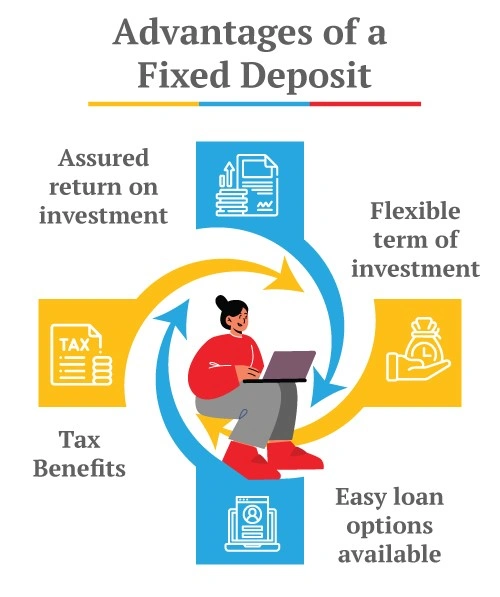

One of the best features of FD is that it acts as savings and earnings at the same time. You can invest in an FD for a certain amount of time and don’t have to worry about it. In other markets, rates and fluctuations disturb your earnings. FDs are Fixed and definite for the investment tenure you choose.

Public Provident Fund is one of the best investment options to grow your money beyond inflation and taxes. The long-term nature of the investment makes it great for compounding your wealth. Here are the salient features of this investment:

After retirement, NPS can be of great help. National Pension Scheme gives equal growth opportunities to both employed and self-employed workforce in India. Salient features of NPS are as follows:

Savings plans from life insurance companies like iSelect Guaranteed Future from Canara HSBC Life Insurance offer long-term, guaranteed compounded growth much like PPF. However, with a significant difference:

ULIPs are some of the most versatile life insurance plans with significant wealth-building potential. The tax-saving quality of the investment makes it one of the best portfolio investments available, along with the following features:

Save and draw tax-free pension with plans like Promise4Growth Plus ULIP from Canara HSBC Life Insurance:

Life cover ensures your family has a minimum guaranteed life cover

World-renowned scientist Einstein himself has called compounding the 8th wonder of the world. Compounding returns are the mainstay of wealth creation.

Compound interest is a great tool for investors and the easiest way to financial freedom. Market-linked investments which offer compounding can greatly enhance your wealth over time. You should ensure adequate long-term investments if you want to benefit from the power of compounding.

An OTP has been sent to your mobile number

Sorry ! No records Found

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.