Written by : Knowledge Centre Team

2026-02-05

3908 Views

8 minutes read

Share

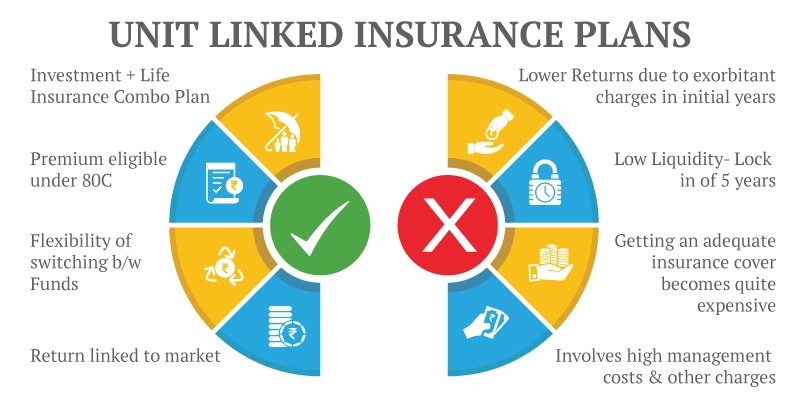

Unit Linked Insurance Plans are some of the most flexible investment options available as long-term investments. However, Unit Linked Insurance Plans are known for their equity fund investments and market-linked returns. Are they really a risky investment?

An asset class is a culmination of similar types of assets, securities, and other instruments which behave in a certain way. Thus, all the securities that are in the same asset class are most likely to react to the market in the same way.

There are different types of asset classes available in which you can invest in. Following are some of the types of asset classes:

Different asset classes have different factors relating to volatility, taxes, duration, etc. ULIP Plans offer three options for investment in three of these asset classes – equity, debt and cash or liquid funds.

If you are thinking of making an investment, you are most likely two consider two things.

These two things are the basis of the performance of all types of investments. If these are favourable to you then the investment will also be favourable.

The general consensus is that there is a positive relationship between risk and the return of any investment. The higher the potential returns of your investment, the higher is the risk as well. This is also known as the risk-return trade-off.

That is why safer investments having little risk such as Government Bonds give you average to low returns, while highly speculative investments can give you very attractive returns.

Unit Linked Insurance Plans apart from providing you with life cover, also give you the opportunity to invest. ULIPs offer three asset classes for investments – equity, debt and liquid assets in a diversified portfolio format.

So, you can come across the following four types of funds to invest in a ULIP Plan:

These are further divided into Large Cap, Small Cap, Multi-Cap, as per the insurance provider.

It is a good choice in the long run as it keeps your funds ticking and is relatively safe as well. These are also known as hybrid funds.

In liquid funds, your amount is invested in Money Market instruments and have carry low risk.

You can allocate your premiums to the ULIP Plan in any ratio in these funds. You can even allocate 100% of the premium to only one fund. And, as per your fund choice, your investment risk in ULIPs can range from high (100% equity) to very low (100% liquid fund).

So, as per your fund choice, your ULIP investment can become a low-risk investment:

| ASSET CLASS/FUND TYPE | RISK INVOLVED |

|---|---|

| 1. EQUITY | High |

| 2. DEBT | Low |

| 3. HYBRID | Medium |

| 4. LIQUID | Very Low |

Investment risk and return only belong to the investor in any formal investment. When you invest in a ULIP Plans as well, the risk from market volatility and resulting growth both belong to you. The insurer can only deduct a nominal fee for the management activities in the fund.

Managing risk with ULIPs can ensure better growth and stable returns in the long run. So, if you are investing in ULIP Plans for the long term and want to grow your money safely, use one of the risk management options in the plan.

Promise4Growth Plus from Canara HSBC Life offers you 4 different strategies to manage risk:

Now let us understand their working briefly.

Your money gets shifted from the funds you have invested into the liquid funds.

This happens at the beginning of each year starting from the 4th year before the maturity.

Also, there are other features of ULIP that further reduce the risk factor these plans involve.

The above strategies show that ULIP Plans are a great way to grow your wealth. Not only this, with the features it offers, you can also minimize the risk involved with your investment.

An OTP has been sent to your mobile number

Sorry ! No records Found

Thank You for submitting the response, will get back with you.

Thank You for submitting the response, will get back with you.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

Canara HSBC Life Insurance offers online ULIP plans that blend life insurance protection with investment growth, helping you build wealth while securing your family's future.